Aug 4, 2022

U.S. stocks little changed as traders parse earnings

, Bloomberg News

If the bond yield stays soft the Fed is not really in control of inflation: Michele Schneider

VIDEO SIGN OUT

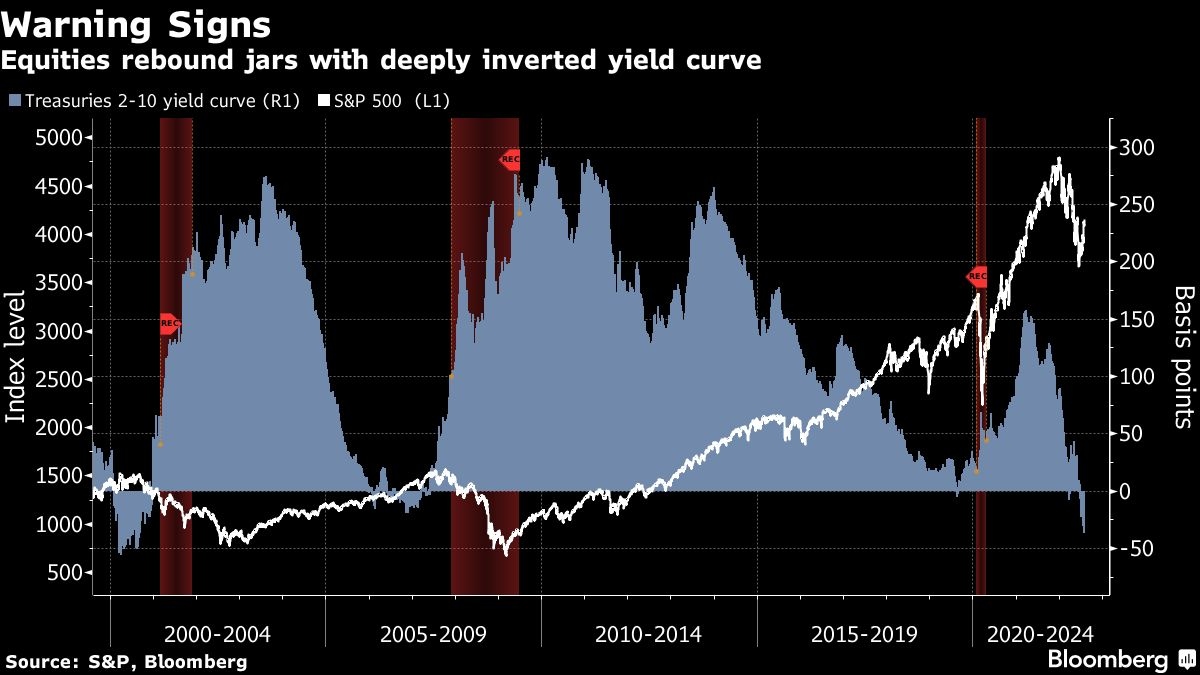

US stocks wavered on Thursday as traders parsed various corporate earnings against a backdrop of aggressive interest-rate hikes by global central banks. The US yield curve remained inverted as recession fears persisted.

The S&P 500 ended the session little changed after fluctuating throughout the session. The Nasdaq 100 closed up higher for the second straight day after swinging between modest gains and losses.

While the tech-heavy index was buoyed by Amazon.com Inc. and Advanced Micro Devices Inc. later in the session, it was also dragged down by Fortinet Inc. after the firm trimmed its service-revenue forecast. Eli Lilly & Co., which dropped after missing Wall Street expectations for second-quarter revenue, weighed on the S&P 500 Index. Thin liquidity in the summer also tends to amplify market moves.

Treasury yields wobbled throughout the session, with the 10-year rate around 2.66 per cent after pushing past 2.80 per cent on Wednesday.

A flurry of economic data that released this week assuaged fears of a downturn while hinting at stabilizing growth. But the bond market, especially the persistently inverted Treasury yield curve, is flashing warnings on the economy amid a global wave of monetary tightening. All eyes will be on the US jobs report on Friday for further clues about the Federal Reserve’s path of rate hikes.

“There’s an intense tug-of-war happening in the economy and markets,” said Dan Suzuki, deputy chief investment officer at Richard Bernstein Advisors. “On one side, you have a narrative that reasonable growth is going to support continued inflation pressure and keep the Fed hiking. The other narrative is that slowing growth is going to ease inflation and allow the Fed to stop hiking.”

On Thursday, Cleveland Fed President Loretta Mester reiterated the central bank’s promise to bring down inflation by raising interest rates. Her counterparts, this week, have also been backing this hawkish stance, forcing markets to recalibrate after initially expecting a dovish pivot Fed Chair Jerome Powell hinted at last week.

US-China tension also remains among the uncertainties clouding the outlook. China likely fired missiles over Taiwan during military drills on Thursday, Japan said, part of Beijing’s biggest cross-strait exercises in decades after US House Speaker Nancy Pelosi visited the self-ruled island.

West Texas Intermediate stayed below US$90 a barrel, a level last seen in the weeks leading up to Russia’s invasion of Ukraine. Gold advanced and Bitcoin fell.

What to watch this week:

- US employment report for July, Friday

Some of the main moves in markets:

Stocks

- The S&P 500 was little changed as of 4 p.m. New York time

- The Nasdaq 100 rose 0.4 per cent

- The Dow Jones Industrial Average fell 0.3 per cent

- The MSCI World index rose 0.9 per cent

Currencies

- The Bloomberg Dollar Spot Index fell 0.4 per cent

- The euro rose 0.8 per cent to US$1.0246

- The British pound rose 0.2 per cent to US$1.2170

- The Japanese yen rose 0.7 per cent to 132.88 per dollar

Bonds

- The yield on 10-year Treasuries declined five basis points to 2.66 per cent

- Germany’s 10-year yield declined seven basis points to 0.80 per cent

- Britain’s 10-year yield declined two basis points to 1.89 per cent

Commodities

- West Texas Intermediate crude fell 2.6 per cent to US$88.33 a barrel

- Gold futures rose 1.9 per cent to US$1,810.30 an ounce