Aug 7, 2019

World economy edges closer to a recession as trade fears spread

, Bloomberg News

Trade war could cause full easing cycle

VIDEO SIGN OUT

The escalating trade war between the U.S. and China is nudging the world economy toward its first recession in a decade with investors demanding politicians and central bankers act fast to change course.

In the U.S. alone, the recession risk is “much higher than it needs to be and much higher than it was two months ago,” Lawrence Summers, a former U.S. Treasury secretary and a White House economic adviser during the last downturn, told Bloomberg Television. “You can often play with fire and not have anything untoward happen, but if you do it too much you eventually get burned.”

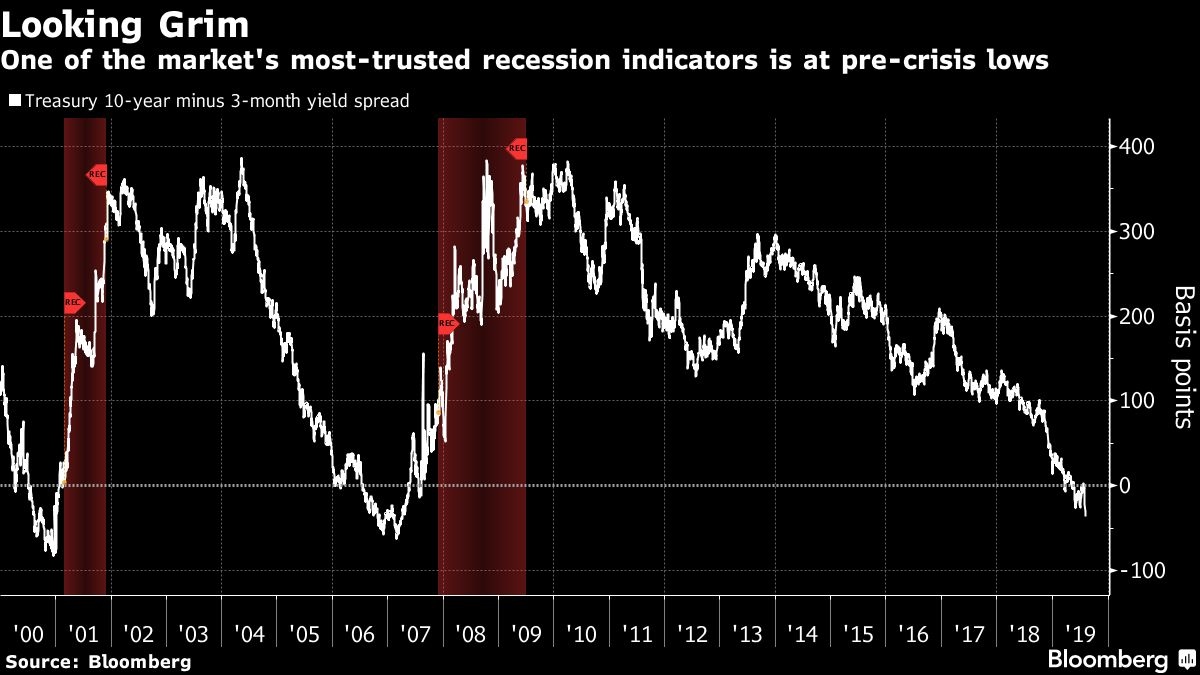

Summers, who teaches at Harvard University, still sees a less than 50/50 chance that the U.S. enters a recession in the next 12 months. Investors are much more bearish: A closely watched segment of the yield curve, the difference between 10-year and three-month notes, inverted the most since 2007, indicating bets on protracted weakness.

New Zealand’s central bank on Wednesday stunned investors by dropping its benchmark rate by 50 basis points, double the expected reduction and sending the kiwi tumbling. Thailand also surprised, cutting by 25 basis points. India’s central bank lowered its rate by an unconventional 35 basis points.

While tight labor markets globally and the recent shift by central banks should provide a cushion, economists are starting to war game for how a recession could happen. Their fears are mainly centered on trade.

Under one scenario, U.S. President Donald Trump would carry through with his latest threat to impose 10% tariffs on a further $300 billion of Chinese goods, drawing a retaliation from President Xi Jinping. While the direct cost of those tariffs is likely to be small, it is the uncertainty created by a further escalation of the trade war that could weigh on investment, hiring and ultimately consumption.

Morgan Stanley economists predict that if the U.S. puts 25% tariffs on all Chinese imports for four to six months and the country hits back, a global economic contraction is likely within three quarters. The tensions also extend beyond the U.S and China to include Japan and South Korea as well as Britain’s future relationship with the European Union.

Global Fallout

The worry is without a trade truce soon, markets will extend their recent slide and uncertainty-plagued companies would pull back further on investment, extending the pain of manufacturers to the services sector. Then, an otherwise tight job market would start to crack and consumers would retrench.

While central banks would likely cut interest rates and perhaps resume quantitative easing, that may no longer be enough to revive animal spirits this time and governments might not be fast enough to loosen fiscal policy.

“With no end in sight, there are significant downside risks to our forecasts for U.S. and global growth,” Bank of America Corp. economists warned clients this week. “If the trade war escalates -- this could include a more explicit currency war -- uncertainty would be considerably higher and financial conditions much tighter.”

What Bloomberg’s Economists Say

“Asset purchases -- if the ECB and others take that path -- will be less effective this time than they were in the past. Conventional policy space is limited. Unconventional policy is of limited effectiveness. Best hope it’s not needed.”--Tom Orlik, chief economist

Much depends on consumer and corporate confidence.

JPMorgan Chase & Co.’s global manufacturing purchasing managers index already shows contraction. June data on industrial production in Germany, Europe’s biggest economy, showed the biggest annual slump in a decade. The European Central Bank is poised to unleash a renewed round of stimulus as soon as September, potentially including a rate cut further into negative territory, to fight a deepening slowdown.

In the U.S., manufacturing growth has slowed for four straight months and Citigroup Inc. equity strategists have cut their earnings forecast for S&P 500 companies.

Then there are consumers. Those in China and the U.S. have continued to spend, perhaps encouraged to by tight labor markets. But JPMorgan economists reckon the pace of global hiring in the second half of this year will slow to its softest since 2012-13. One early warning sign: Car sales in China are reeling from a historic slump.

Barely finished cleaning up from their last recessions, central banks are swinging back toward rescue mode. Having cut rates a week ago for the first time since 2008, the Federal Reserve is on course to do so again next month and investors price in further action by year-end. That’s despite Chairman Jerome Powell’s signal that he’s undertaking more of a mid-cycle adjustment than a pronounced easing cycle.

But this time around central bankers may not be powerful enough given rates are already low and further action may not offset the fallout from the trade troubles. Investors surveyed recently by Bank of America Corp. identified monetary policy impotency as their biggest concern.

“We are using interest rates to fix problems that they cannot solve,” said Patrick Bennett, head of macro strategy for Asia at Canadian Imperial Bank of Commerce in Hong Kong.

An added complication is the U.S. Treasury’s decision this week to label China a currency manipulator after China allowed the yuan to weaken past 7 against the dollar for the first time since 2008.

“We have gone from some degree of uncertainty to bucket loads of uncertainty yet again,” said Fraser Howie, who has two decades of experience in China’s financial markets and co-wrote the 2010 book “Red Capitalism.”

--With assistance from Craig Stirling.