Oct 30, 2017

Larry Berman: What's going on with the Canadian dollar?

By Larry Berman

The Canadian dollar has been on a roller coaster all year.

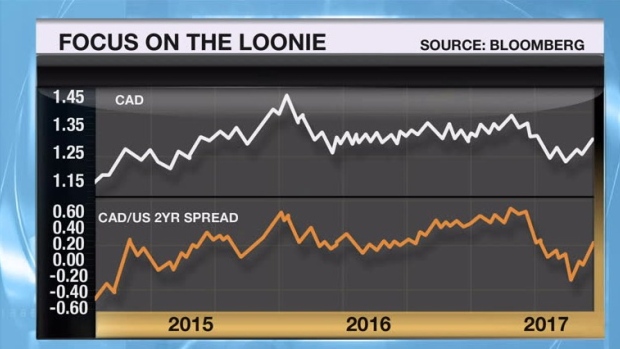

Early in the year, the message from the Bank of Canada was that the economy was not at full potential and continued to require extremely low interest rates. Coupled with this, the U.S. Federal Reserve has been focused on raising rates and now reducing the size of their balance sheet. This combination pushed two-year interest rate differentials (green line) between Canada and the U.S. to multi-year lows in September. The last time it was at a positive for Canada was before the central bank surprised us with a rate cut in January 2015 in response to falling oil prices.

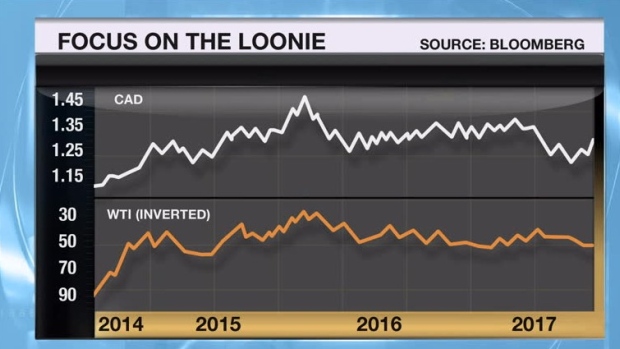

Historically, the Canadian rates have been higher than U.S. rates to help support the value of the “weaker” Canadian dollar. Since oil prices started to become more of a factor in the mid 2000s, that dynamic changed for a while. Remember when the Canadian dollar spiked 10 cents higher than the U.S. dollar in 2007, when WTI hit US$100 for the first time?

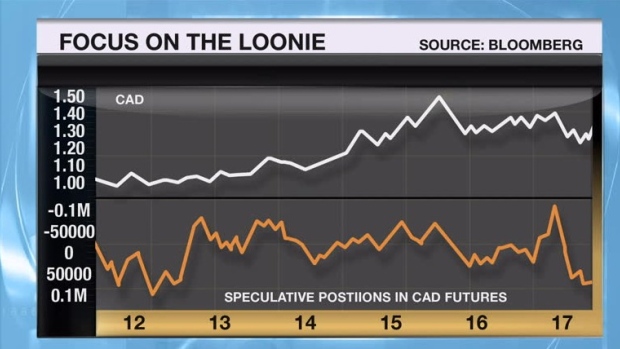

A few quarters of surprising and unexpected GDP growth and the Bank of Canada removed the emergency rate hikes they put on in 2015 when oil prices collapsed. That prompted speculators that were heavily betting on Canadian dollar weakness to continue to reverse positions. That pushed the Canadian dollar to about 83 cents (1.2023) capping a 4-month rally of almost 10 per cent. Those same group of investors are now speculating that the loonie is going to get stronger. It looks like they are wrong again and are the source of potentially more selling especially if NAFTA breaks apart.

WTI has been stronger recently, but it’s influence on the loonie has been none existent in recent weeks.

So what are these variables telling us about where the Canadian dollar will go in the coming months. It looks like the dollar is poised for a bit more weakness. The market expects the Fed to raise rates in December and the Bank of Canada will likely match a rate hike in January.

NAFTA is back on the front burner towards the end of Q1, and based on the U.S. mid-term elections next year, we think Trump will likely break the agreement. Expectations are for that to be worth about two to four cents. Some of that risk is already priced in, but we will not know how much until maybe mid 2018 when second round negotiations likely breakdown.

If you want to learn how to make better investment decisions and how to build portfolios that fit your investor type, come out to the current Berman’s Call tour (investor’s guide to thriving). You will learn about some of the behavioural biases that might be hurting your investment returns and learn how a bit more about how to properly diversify your portfolios, which most individual investors do not do very well. Learn how to identify what type of investor you are and some techniques to improve how to manage your asset allocation so you can preserve and grow your portfolio. The events are free and we ask for a voluntary charitable donation to either Sick Kids Hospital or Baycrest Brain Health research for Alzheimer’s. Visit www.etfcm.com or Bermanscall.com to register.

Follow Larry Online:

Twitter: @LarryBermanETF

LinkedIn Group: ETF Capital Management

Facebook: ETF Capital Management

Web: www.etfcm.com