Dec 12, 2023

Markets today: Traders betting Fed peak is here curb pivot wagers

, Bloomberg News

BNN Bloomberg's mid-morning market update: Dec. 12, 2023

VIDEO SIGN OUT

Wall Street saw small moves in the run-up to the Federal Reserve decision, with underwhelming inflation data reinforcing speculation policymakers will be in no rush to claim victory just yet.

While markets continued to bet officials will be on hold Wednesday, the latest figures bring into question the aggressive pricing of a dovish pivot. Traders have slightly trimmed their wagers on rate cuts in 2024, with the first one still projected to happen in May. The data also spurred speculation that Jerome Powell will try to throw cold water on the Fed-easing buoyancy.

Following the last Fed decision, Powell reminded investors that inflation progress will “come in lumps and be bumpy.” The fact that Tuesday’s consumer price index was roughly in line with estimates — and ticked up a bit — underscored the choppy nature of getting prices back to the 2 per cent target — especially in the service sector, which the Fed has zoned in on as the last mile in its inflation fight.

“Today’s CPI report is a little bit of a ‘mood dampener’,” said Seema Shah at Principal Asset Management. “This isn’t enough inflation deceleration to reassert or justify the market’s policy-easing expectations, particularly at a time when the labor market is still so solid. Powell should push back at the recent market narrative.”

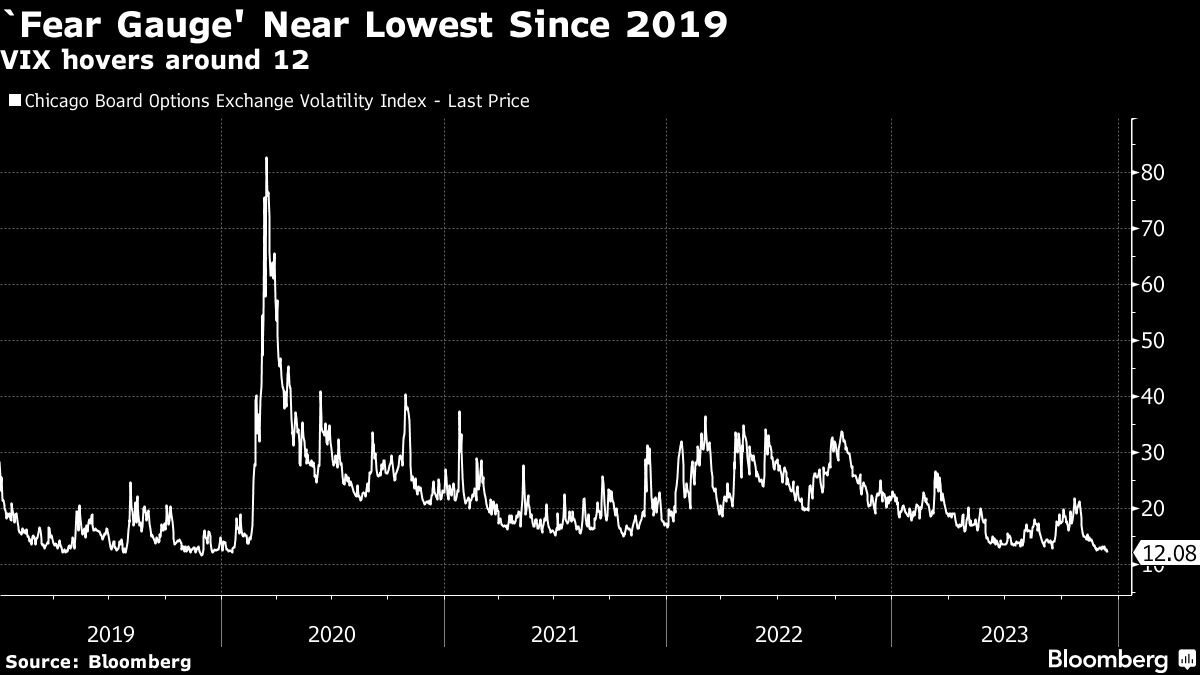

After whipsawing in the immediate aftermath of the report, two-year yields steadied above 4.7 per cent. Long-term Treasuries swung to a small gain after solid demand in a US$21 billion sale of 30-year bonds. The S&P 500 eked out a mild advance to the highest since January 2022. Wall Street’s “fear gauge” — the VIX — slid toward a four-year low.

To Krishna Guha, vice chairman at Evercore, the CPI data will chime with policymakers’ sense that the disinflation process will continue to advance gradually — with the potential for noise along the way.

“Powell will have to ‘walk a fine line’ by recognizing the ground gained towards the normalization of the economy while pushing back on the idea of early rate cuts,” according to TD Securities strategists Oscar Munoz and Gennadiy Goldberg. “We expect the chairman to lean against the Committee’s likely dovish guidance, with guarded hawkishness in the post-meeting presser.”

Barring a meaningful deterioration of the economy and labor market, the Fed won’t be easing policy until they’re certain inflation is on a clear and sustainable path toward the 2 per cent objective, the TD strategists noted. “Today’s report is unlikely to provide that certainty just yet.”

Signs of disinflation helped drive the U.S. bond market last month to its biggest gain since the mid-1980s, with yields tumbling sharply on speculation the Fed will cut its benchmark rate by over a full percentage point in 2024.

“Knocking inflation down from last year’s highs is one thing, getting it to the Fed’s 2 per cent target is another,” said Chris Larkin at E*Trade from Morgan Stanley. “Today’s number aside, though, the trends still point to a slowing economy and cooling inflation. That means lower rates are still on the 2024 horizon — just not as near as some people may be hoping.”

U.S. Treasury Secretary Janet Yellen said Tuesday she doesn’t believe the “last mile” in returning inflation to the Fed’s 2 per cent goal will be especially difficult.

While price pressures have largely retreated from multi-decade highs, a still-strong labor market continues to power consumer spending and the broader economy. Data last week showed that the U.S. labor market unexpectedly strengthened in November with pickups in employment and wages. The unemployment rate fell to 3.7 per cent and workforce participation edged up. Monthly wage growth rose more than forecast.

“The wage sensitive core services components that have been a focus for the Fed continue to move sideways, reaffirming our view that despite the significant progress on inflation, the labor market still needs to cool for the Fed to ultimately be successful in returning inflation to 2 per cent,” said Tiffany Wilding, managing director and economist at Pacific Investment Management Co.

With the Fed widely expected to keep its target rate range steady for the third straight meeting at 5.25 per cent to 5.5 per cent, traders will carefully scrutinize any signals from Powell on the path for policy and the update to the central bank’s quarterly forecasts.

“The trick now is make sure the policy which broke the back of inflation does not boomerang and stall the economy into recession. The Fed now has a very narrow path to prevent the latter from occurring,” said Jamie Cox, managing partner for Harris Financial Group.

How the Fed frames its outlook for rate policy ending next year and 2025 via its “dot-plot” could inject some uncertainty into a market that has run ahead of the central bank’s current forecast.

“Market participants wait to see if Fed Chair Powell’s comments and the revised Summary of Economic Projections spread holiday cheer tomorrow or embolden the Grinch,” said Jose Torres, senior economist at Interactive Brokers.

An SEP that is consistent with expectations for five rate cuts in 2024 will likely drive stocks to a “Santa Claus rally”, he noted, adding that “projections for only two to three cuts could cause equities to join the Grinch in finishing the year on a dour note.”

Corporate Highlights:

- Netflix Inc. is ready to tell the world how many people watch its shows. On Tuesday, the company released global midyear viewer data for every title on its service, the first of what Netflix said will be regular reports.

- Walgreens Boots Alliance Inc. is reviving discussions on a potential exit from its UK drugstore chain Boots, people with knowledge of the matter said, nearly 18 months after a sale process was scrapped.

- Boeing Co. delivered 46 of its 737 family jets in November, its largest such tally in five months, leaving the manufacturer just 24 aircraft short of its revised annual target.

- A second U.S. union is accusing Starbucks Corp. of refusing to fairly negotiate, undermining the company’s recent efforts to prove it’s the one trying to get contracts completed.

- Google’s legal defeat at the hands of Fortnite maker Epic Games Inc. threatens to roil an app store duopoly with Apple Inc. that generates close to $200 billion a year and dictates how billions of consumers use mobile devices.

- Oracle Corp. reported slowing quarterly sales growth in its cloud computing business, fueling investor fears that the software maker’s expansion efforts have yet to gain ground in the competitive market.

- Numerous components in RTX Corp.’s marquee commercial jet engine are at risk of premature failure and must be replaced as part of the company’s costly recall tied to parts made with tainted metal powder, according to U.S. aviation safety regulators.

- Macy’s Inc. was cut to sell at Citigroup Inc. on skepticism that a buyout offer from Arkhouse Management and Brigade Capital Management will actually materialize.

- Walt Disney Co. and Reliance Industries Ltd., led by Asia’s richest tycoon Mukesh Ambani, are expected to sign a non-binding pact as early as Monday to merge their media operations in India in a cash-and-stock deal, according to people familiar with the matter.

Key events this week:

- Eurozone industrial production, Wednesday

- U.S. PPI, Wednesday

- Federal Reserve policy meeting and news conference with Chair Jerome Powell, Wednesday

- European Central Bank policy meeting followed by news conference with ECB President Christine Lagarde, Thursday

- Bank of England policy meeting, Thursday

- Swiss National Bank policy meeting, Thursday

- U.S. initial jobless claims, retail sales, business inventories, Thursday

- China 1-yr MLF rate and volume, property prices, retail sales, industrial production, jobless rate, Friday

- Eurozone S&P Global Manufacturing PMI, S&P Global Services PMI, Friday

- U.S. industrial production, Empire manufacturing, cross-border investment, Friday

Some of the main moves in markets:

Stocks

- The S&P 500 rose 0.5 per cent as of 4 p.m. New York time

- The Nasdaq 100 rose 0.8 per cent

- The Dow Jones Industrial Average rose 0.5 per cent

- The MSCI World index rose 0.4 per cent

Currencies

- The Bloomberg Dollar Spot Index fell 0.2 per cent

- The euro rose 0.3 per cent to $1.0797

- The British pound rose 0.1 per cent to $1.2568

- The Japanese yen rose 0.4 per cent to 145.53 per dollar

Cryptocurrencies

- Bitcoin was little changed at $41,197.75

- Ether fell 1.5 per cent to $2,183.85

Bonds

- The yield on 10-year Treasuries declined three basis points to 4.20 per cent

- Germany’s 10-year yield declined four basis points to 2.23 per cent

- Britain’s 10-year yield declined 11 basis points to 3.97 per cent

Commodities

- West Texas Intermediate crude fell 3.7 per cent to $68.71 a barrel

- Spot gold fell 0.1 per cent to $1,979.28 an ounce