Nov 2, 2022

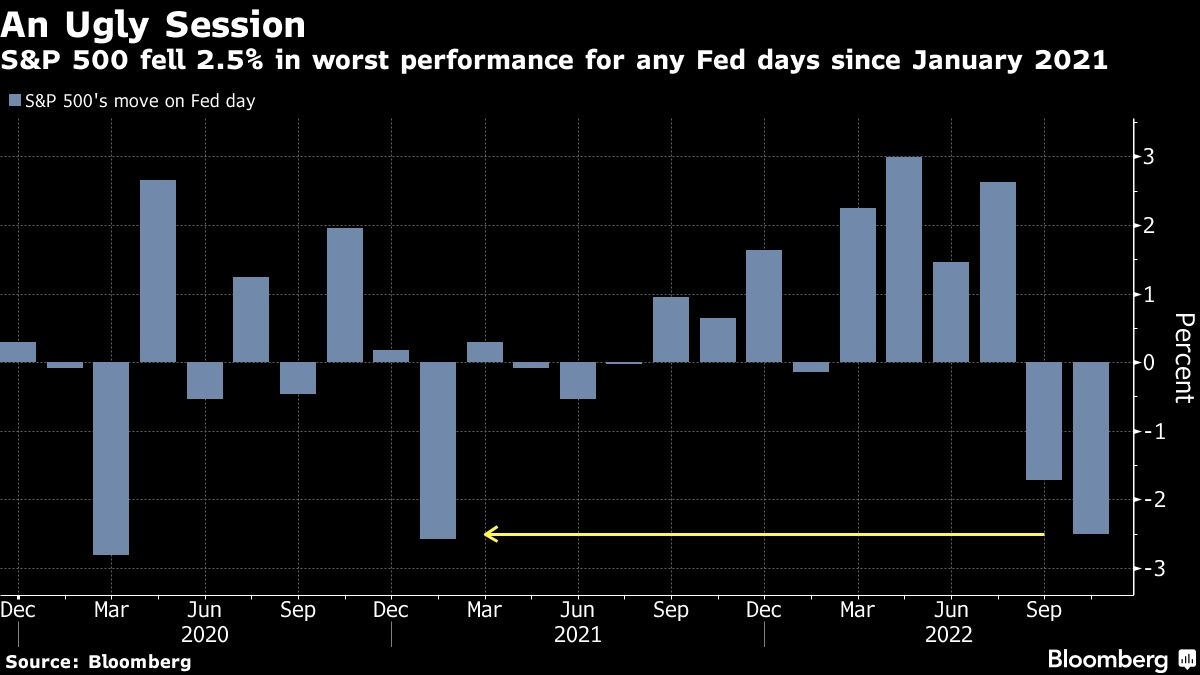

S&P 500 suffers worst 'Fed day' since January 2021

, Bloomberg News

BNN Bloomberg's closing bell update: November 2, 2022

VIDEO SIGN OUT

Stocks sold off as Jerome Powell continued to sound unequivocally hawkish as the Federal Reserve pushed ahead with its most-aggressive tightening campaign since the 1980s to thwart inflation.

The S&P 500 suffered its worst rout on a Fed decision day since January 2021. Stocks came decidedly lower after Powell said the Fed still has “some ways to go” in its policy cycle, adding that it’s premature to think about a pause as rates could peak at higher levels than previously thought. The move wiped out an earlier rally driven by his remarks that a slower pace of hikes could come as soon as December.

“It’s as if investors came to a haunted house and got candy, but once they unwrapped it, saw it was soggy broccoli,” said Max Gokhman, chief investment officer at AlphaTrAI.

Megacap tech bore the brunt of the selling, with giants like Apple Inc. and Tesla Inc. tumbling more than 3.5 per cent. In late trading, Qualcomm Inc., the biggest maker of smartphone processors, slumped on a weak forecast. Two-year U.S. yields -- which are more sensitive to imminent Fed moves -- reversed course and pushed higher. The dollar gained.

“When Powell made his comments regarding nothing pivot-related, or no shot of that, I think that was the ‘dagger’ for the market,” said Alon Rosin, head of institutional equity derivatives at Oppenheimer & Co.

The Federal Open Market Committee said that “ongoing increases” will still likely be needed to bring rates to a level that are “sufficiently restrictive to return inflation to 2 per cent over time,” in fresh language added to their statement. Officials unanimously decided to lift the target for the benchmark rate by another 75 basis points to a range of 3.75 per cent to 4 per cent, its highest level since 2008.

Comments:

- Ronald Temple, head of U.S. equity at Lazard Asset Management:

- “This is not an environment in which the Fed will pivot or signal a pivot. To do so would be malpractice, and the Fed knows that. In December, the Fed will have two more inflation reports and two more jobs reports. Then, perhaps, the FOMC can signal a deceleration in tightening, but not before.”

- Ian Lyngen and Ben Jeffery, strategists at BMO Capital Markets:

- “One thing is obvious from the Fed’s tone; ‘Santa Pause’ ain’t coming to town.”

- Edward Moya, senior market analyst at Oanda:

- “Stocks might struggle here as the risk of the Fed taking rates above 5.00 per cent are clearly still on the table.”

- Sam Stovall, chief investment strategist at CFRA:

- “Of course data will largely determine the policy path going forward. Our best guess is that the Fed continues to take the more hawkish path.”

- Quincy Krosby, chief global strategist at LPL Financial:

- “Factoring in the bond market’s assessment, markets are becoming increasingly convinced that the path towards the terminal rate will include a recession.”

- Christopher Harvey, equity analyst at Wells Fargo Securities:

- “The major message during the press conference was that rates needed to go (and stay) higher for longer than many expected.”

Data Wednesday showed hiring at U.S. companies rose in October by more than forecast, underscoring resilient labor demand despite the Fed’s efforts to cool the economy. A strong job market has fueled fast wage growth, contributing to rapid inflation and putting pressure on the Fed to aggressively tighten monetary policy.

The Treasury halted the longest string of cutbacks to its quarterly sales of longer-term debt in about eight years, showcasing the end of a period of historic reduction in the fiscal deficit.

In corporate news, Boeing Co.’s chief said the planemaker could generate US$10 billion in cash annually by mid-decade, once it turns around its operations after years of setbacks and miscues. China has ordered a seven-day lockdown of the area around Foxconn Technology Group’s main plant in Zhengzhou, a move that will severely curtail shipments in and out of the world’s largest iPhone factory.

Key events this week:

- Bank of England rate decision, Thursday

- U.S. factory orders, durable goods, trade, initial jobless claims, ISM services index, Thursday

- ECB President Christine Lagarde speaks, Thursday

- U.S. nonfarm payrolls, unemployment, Friday

Some of the main moves in markets:

Stocks

- The S&P 500 fell 2.5 per cent as of 4 p.m. New York time

- The Nasdaq 100 fell 3.4 per cent

- The Dow Jones Industrial Average fell 1.6 per cent

- The MSCI World index fell 1.7 per cent

Currencies

- The Bloomberg Dollar Spot Index rose 0.3 per cent

- The euro fell 0.5 per cent to US$0.9830

- The British pound fell 0.8 per cent to US$1.1395

- The Japanese yen rose 0.3 per cent to 147.77 per dollar

Cryptocurrencies

- Bitcoin fell 1.1 per cent to US$20,245.42

- Ether fell 2.5 per cent to US$1,536.43

Bonds

- The yield on 10-year Treasuries advanced four basis points to 4.08 per cent

- Germany’s 10-year yield advanced one basis point to 2.14 per cent

- Britain’s 10-year yield declined seven basis points to 3.40 per cent

Commodities

- West Texas Intermediate crude rose 1 per cent to US$89.23 a barrel

- Gold futures fell 0.6 per cent to US$1,640 an ounce