Oct 30, 2019

Fed prepares to pause after third rate cut

, Bloomberg News

Bank of Canada, Fed decisions loom

VIDEO SIGN OUT

Jerome Powell may be getting ready to pause this year’s monetary easing campaign.

The Federal Reserve chairman and his colleagues are expected to cut interest rates a quarter point on Wednesday for a third straight meeting, to provide insurance against global risks, while signaling that the committee has probably done enough for now. The decision will be announced at 2 p.m. in Washington with Powell facing reporters 30 minutes later.

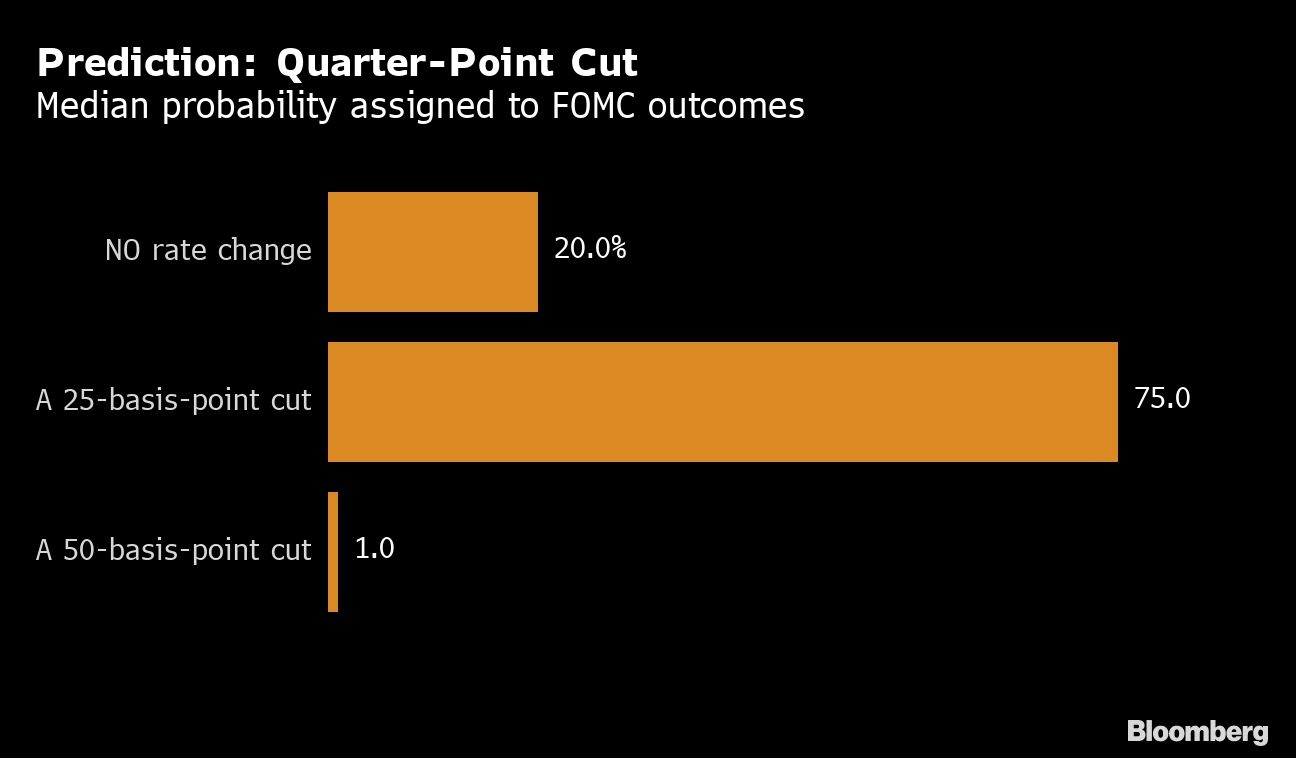

Investors are pricing a 90 per cent likelihood of a cut though economists surveyed by Bloomberg put the odds at 75%, betraying a bit more doubt that reflects divisions on the committee about the need to lower borrowing costs much further. While policy makers all see risks from trade uncertainty and weakness abroad, some view the Fed’s reductions in July and September as already sufficient to offset those headwinds absent additional shocks.

Powell will likely use his press conference to communicate that message of a pause while emphasizing flexibility if the economic outlook shifts significantly.

“What they want to provide is a hawkish cut,’’ said Carl Tannenbaum, chief economist with Northern Trust Co. in Chicago and a former Fed researcher. “Expressing that properly will require some deft expression, which the Fed hasn’t always been able to provide.’’

Powell is following the playbook of a mentor, Alan Greenspan, who cut rates three times in midcycle adjustments in 1995-1996 and in 1998 to counter risks. September forecasts showed the FOMC saw interest rates hitting bottom this year before rising slightly in 2021.

Investors are slightly more dovish and have fully priced in another quarter point cut by mid-2020. The Fed will update its quarterly forecasts in December.

What Bloomberg Economists Say

“Bloomberg Economics expects officials to adopt a “meeting-by-meeting” approach to evaluating the need for additional stimulus, so as to appease hawkish-leaning members of the committee. However, from meeting-to-meeting in a slow growth, low inflation environment, officials will see greater need to provide additional support.”

-- Carl Riccadonna, Yelena Shulyatyeva, Andrew Husby and Eliza Winger

The FOMC is divided between policy makers who favor insurance against risks from a manufacturing slump, the trade war with China, Brexit and slower global growth, versus those who see domestic data largely supporting their outlook for solid growth.

The latter camp includes Kansas City Fed’s Esther George and Boston’s Eric Rosengren, both likely to dissent again if the Fed cuts rates on Wednesday. They have some company: The Fed’s September dot plot of interest rate projections showed five officials didn’t favor the cut delivered at that meeting and another five who saw no need for another cut this year.

That creates the possibility of a surprise, and economists put 20% odds that the FOMC will decide not to cut Wednesday. Any pause would also certainly be opposed by President Donald Trump, who’s pushed publicly for lower rates to rev up the economy.

“This meeting will be very contentious,’’ said Jonathan Wright, economics professor at Johns Hopkins University in Baltimore, who previously worked at the Fed. “The overall data since the last meeting aren’t that negative, and a lot of FOMC participants, mostly nonvoting, will be unconvinced of the wisdom of cutting again.’’

The last time the Fed reduced rates three times while the economy was growing was in 1998. After the third cut, it sent a strong signal it was done, announcing that financial conditions following 75 basis points of easing “can reasonably be expected” to sustain the expansion.

Wednesday’s statement might also suggest “we have done enough,’’ said Stephen Stanley, Amherst Pierpont chief economist. “If they ease and want to send a pause signal, it will be up to Powell to flesh it out.’’

The FOMC may consider tweaking its assessment of current conditions to slightly weaker wording, noting that the job creation has eased and inflation expectations have moderated, said Lindsey Piegza, chief economist with Stifel Nicolaus in Chicago.

One concern Fed officials may have with too strong of a pause signal is that it could flatten the Treasury yield curve, and an inverted yield curve -- where short term rates are higher than long-term ones -- is traditionally viewed as a recession warning that could alarm investors.

“The market is likely to increasingly question the Fed’s resolve to prop up a faltering economy which could translate into lower rates on the longer end, perpetuating the need for further Fed action to stabilize the shape of the yield curve,’’ she said.

The central bank was not seen making much news on its balance sheet following an Oct. 11 announcement it would buy Treasury bills at an initial $60 billion a month pace to lift bank reserves in the system. The Fed has repeatedly called the measure, undertaken after sharp spikes in overnight money market rates, a technical step that did not alter the stance of monetary policy.