Oct 30, 2019

Outlier status leaves Bank of Canada atop the interest rate heap

, Bloomberg News

The Bank of Canada is widely expected to hold interest rates steady for an eighth-straight meeting on Wednesday, probably leaving the country with the highest policy rate among the world’s major economies.

All but two of 30 forecasters in a Bloomberg survey see Governor Stephen Poloz maintaining the benchmark overnight rate at 1.75 per cent at 10 a.m. in Ottawa. Four hours later, in rare back-to-back decisions for Canada and the U.S., the Federal Reserve is expected to reduce borrowing costs for a third time since June.

The end result would be a drop in the midpoint of the Fed funds rate, currently at 1.88 per cent, to below Canadian rates for the first time since 2016. If that happens, the Bank of Canada would have the highest policy rate not only in the Group of Seven but across the industrialized world.

Here are some of the reasons Canadian policy makers are resisting the dovish turn in global monetary policy and adopting a wait-and-see approach.

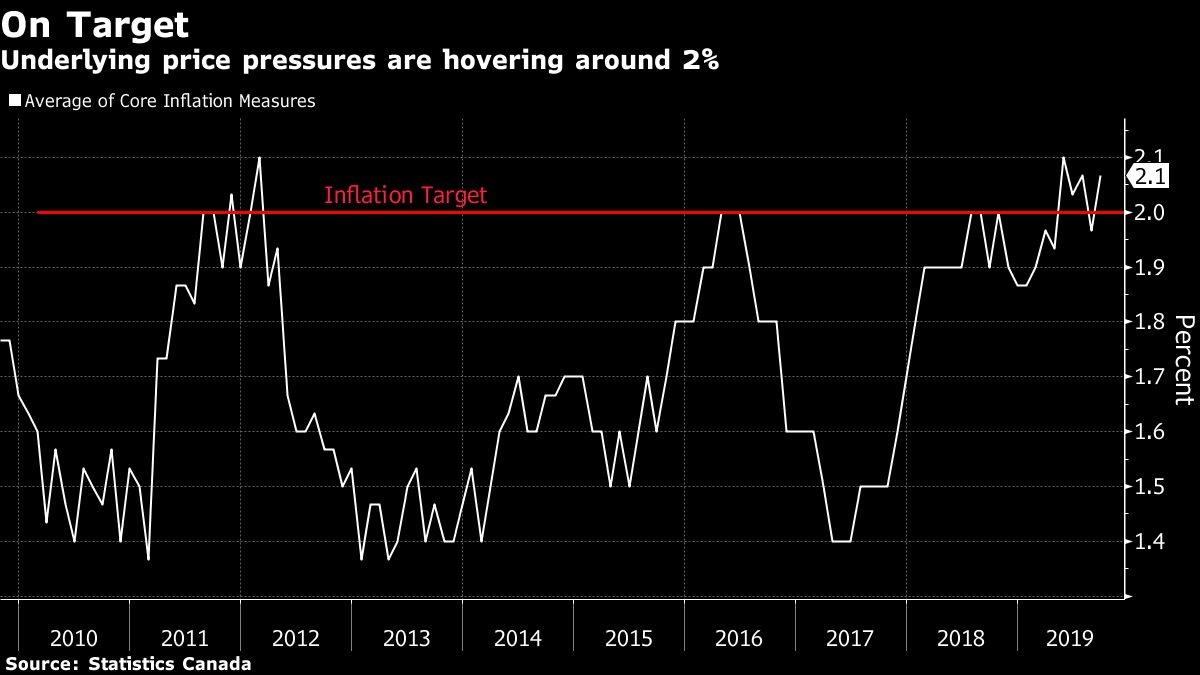

Underlying price pressure -- as measured by core inflation -- has been stable near the Bank of Canada’s two per cent target for well over a year. That’s easily the best the central bank has done in hitting its target over a prolonged period, and reflects an economy running nicely at about its capacity -- neither too hot nor too cold.

This validates Poloz’s decision to hike rates through 2017 and 2018 to levels that, as recently as September, officials described as stimulative.

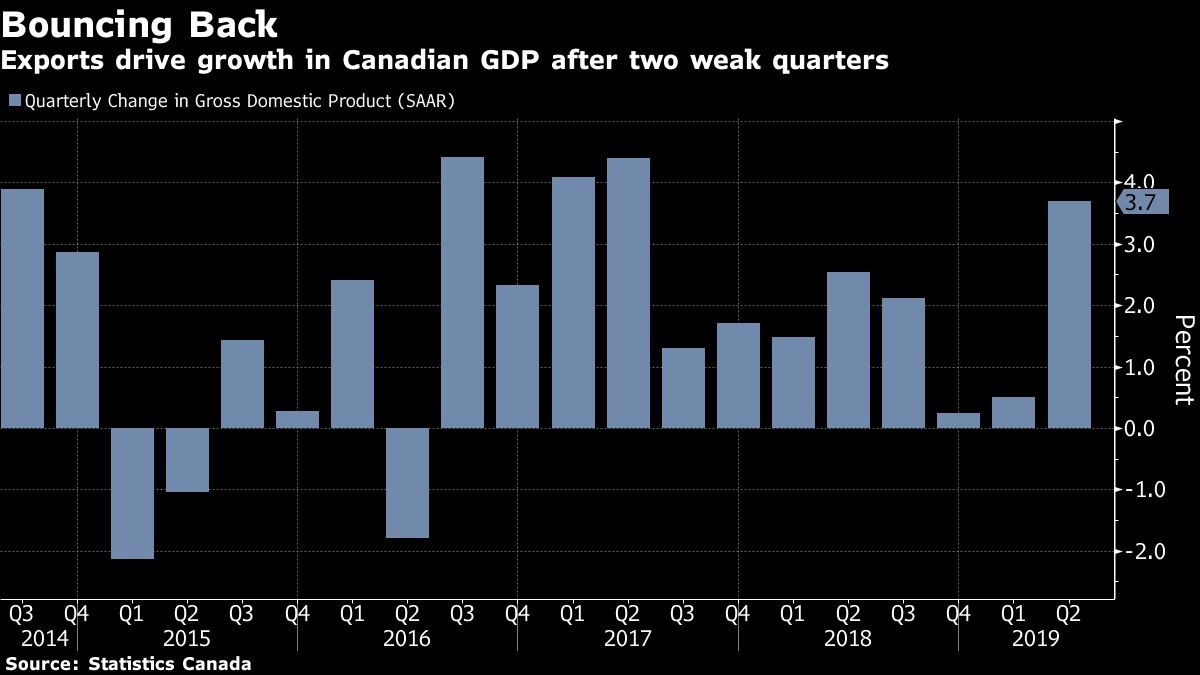

Canada’s economy surprised analysts with a better-than-expected performance in the first half. Annualized growth of just over two per cent reflected a strong rebound in exports that probably won’t continue in the second half, but the anticipated slowdown isn’t likely to be severe enough to push output far below capacity, if it all.

Economists expect growth to slow to 1.5 per cent over the next two years, slightly below potential -- one reason some forecasters are calling for at least one rate cut in the next few quarters.

However, the central bank, which will revise its forecasts Wednesday, has been predicting growth will be slightly above potential over that period, closer to two per cent.

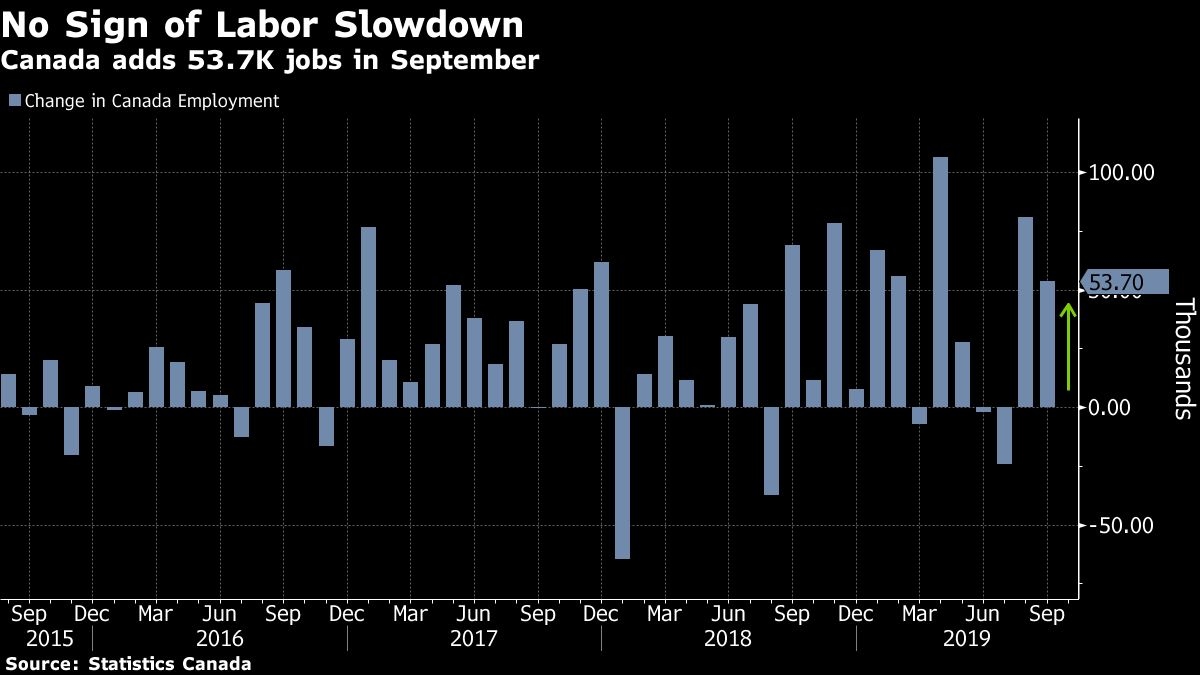

Another reason the central bank can remain on hold is a jobs market that’s on track for one of its best years on record. Canada has added 358,100 jobs since December, the most in the first nine months of a year since 2002. This isn’t just evidence that workers remain in demand, but also creates a virtuous cycle where employment gains fuel income growth that will boost consumption down the line.

In fact, were it not for a sharp increase in the immigrant labor force to meet the demand, the country would almost certainly be running up against capacity constraints that would be fueling even sharper increases in wages than currently seen.

“Conditions have held up well enough domestically that the Bank of Canada doesn’t feel they have fallen behind the curve,” said David Tulk, a Toronto-based portfolio manager at Fidelity Investments. “With there still being a lot of ambiguity on the international front, they can buy as much time as possible to see how all of these inevitably unfold.”

Canada’s housing market, which looked vulnerable earlier this year, has stabilized. For that, Poloz can thank falling bond yields globally, which pushed down mortgage rates in Canada and rekindled demand. Essentially, Canada has already had a dose of stimulus.

It didn’t look good for a while, with home sales hitting a six-year low in February and residential investment tumbling for five straight quarters amid escalating concern about corrections in Toronto and Vancouver.

That all seems to be forgotten, with healthy signs of recovery in both markets, and even stronger gains elsewhere. Housing investment also rebounded during the spring, and isn’t any longer expected to be a drag on growth.

That said, policy makers will be reluctant to see housing turn into a major driver again. That’s because elevated real estate prices are the main culprit in the country’s record household debt ratios, now the highest in the Group of Seven. As Deputy Governor Lawrence Schembri said in the central bank’s last public statement on monetary policy in September, the Bank of Canada is “mindful of the implications for financial vulnerabilities.”

--With assistance from Erik Hertzberg and Shelly Hagan.