Sep 10, 2023

Oil holds at yearly highs as technical levels give traders pause

, Bloomberg News

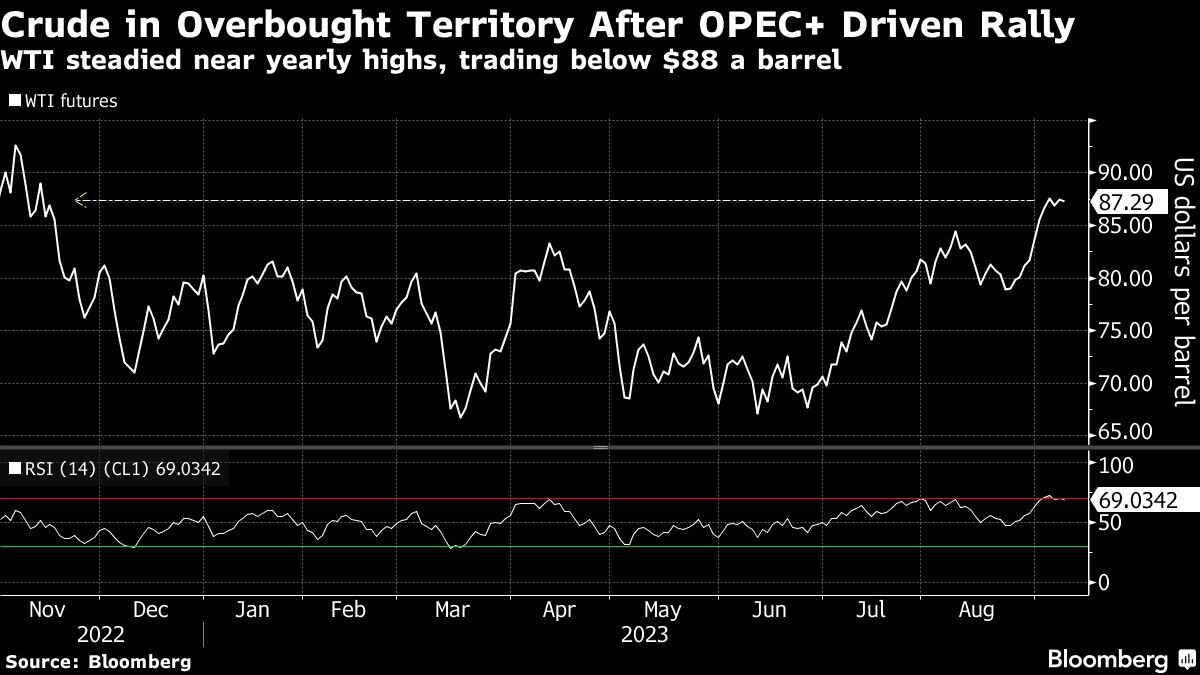

Oil steadied near its highs of the year after rallying about 10 per cent in recent weeks, with technical indicators that suggest its gains may be overdone sapping the benefit of risk-on sentiment in broader markets.

West Texas Intermediate edged lower to settle near US$87 a barrel after a 2.3 per cent advance last week. Oil has surged by almost US$20 a barrel since mid-June on supply curbs from Saudi Arabia and Russia, which have now been extended through the end of the year. Traders are bracing for a potential pullback as technical gauges, including the relative strength index, show futures remain near overbought territory after a renewed surge over the past two and a half weeks.

Diesel futures in Europe also extended their strong run, pushing past US$1,000 a ton for the first time since January. Russia is planning large cuts to its western seaborne exports of the fuel this month.

Signs of bullishness have permeated the oil market complex. Money managers hold the biggest net long position in WTI in 15 months, while they also added to bets for gains in Brent last week. That came as OPEC+ leaders Saudi Arabia and Russia pledged to extend their supply curtailments.

“Producers are keeping it tight in the tug-of-war over energy prices,” Barclays Plc analyst Amarpreet Singh said in a note. “With Saudi Arabia more aggressive than expected with its unilateral cut and continuing strength in demand, we caution against fading the recent run-up.”

Prices:

- WTI for October delivery fell 22 cents to settle at US$87.29 a barrel in New York.

- Brent for November settlement edged lower 1 cent to settle at US$90.64 a barrel.