Aug 27, 2021

Wall Street during the pandemic: The impossible is now commonplace

, Bloomberg News

Wall Street Talent Battle Deepens

VIDEO SIGN OUT

Despite the seemingly endless supply of brainpower and cutting-edge technology that’s put to work in financial markets, at times it feels as if nobody knows anything.

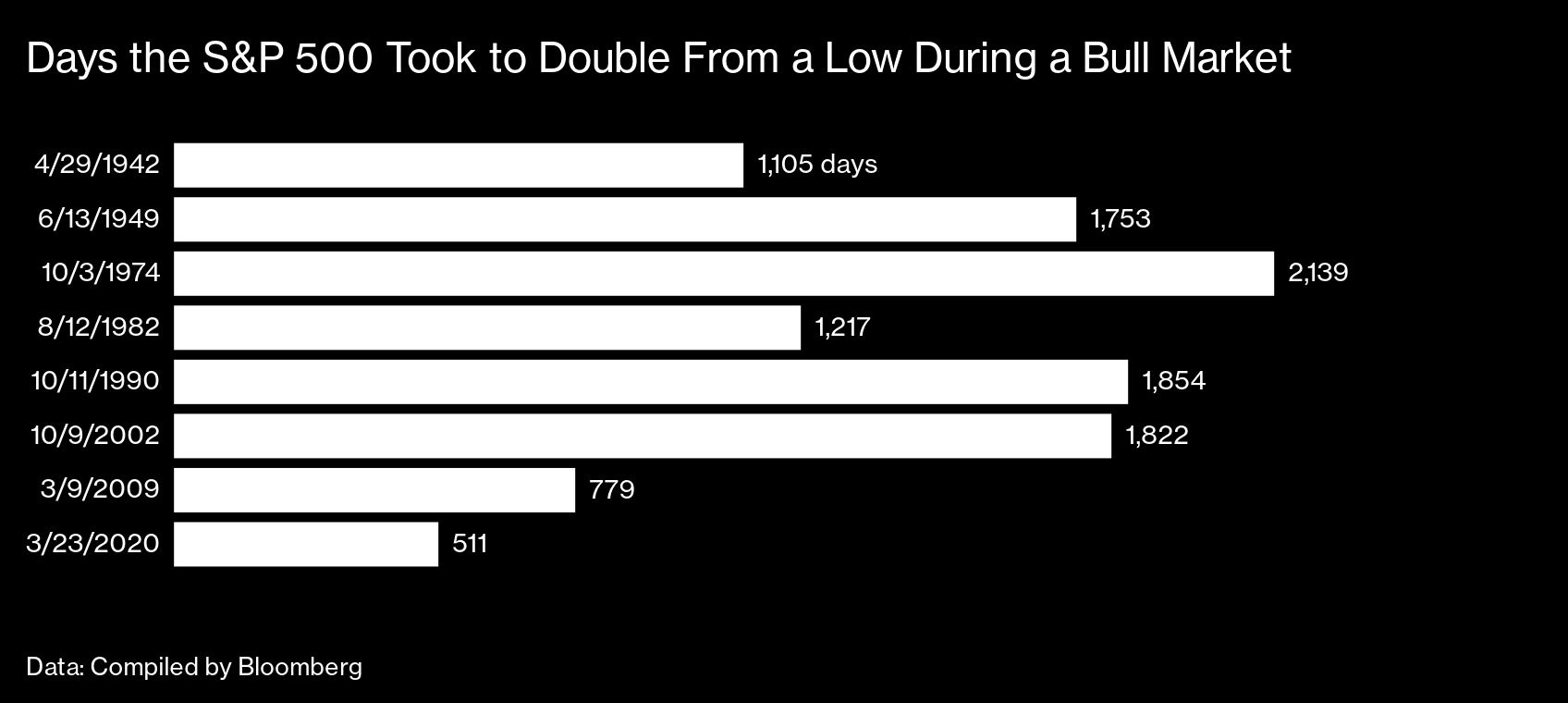

That’s perhaps the hardest-to-digest lesson learned—or at least reinforced—from the past year and a half, during which the U.S. stock market doubled at the fastest pace since 1932: The accrued wisdom of Wall Street can be a swiftly depreciating asset.

“If someone would have told me in March of last year, when COVID was first rearing its ugly head, that 18 months later we would have case counts that are as high—if not higher—than they were on that day, but that the market would have doubled over that 18-month period, I would have laughed at them,” says Steve Chiavarone, a portfolio manager and head of multi-asset solutions at Federated Hermes Inc.

So one of the crucial lessons from this period for Chiavarone is to always have some humility. “Even if you could forecast the virus, you didn’t necessarily get the market right,” he says. “Even if you could forecast an election outcome, you didn’t necessarily get the market right.”

There’s plenty of evidence to show just how far off the mark forecasts have been in the pandemic era. Although it’s common for companies to outperform Wall Street analysts’ published forecasts, earnings across those in the S&P 500 have beaten their estimates by an average of more than 19 per cent in the past five quarters. Prior to the pandemic, they were beating estimates by about 3 per cent. The mismatch meant that when the bear market was at its worst in March 2020, one of the cornerstone concepts of valuing equities—the level of an index relative to its companies’ projected earnings—made U.S. stocks look about one-fifth more expensive than they turned out to be.

Perhaps that helps explain why investors keep pushing stocks higher in the face of collected-wisdom valuation metrics that, in many cases, ostensibly show stocks are as expensive as they’ve ever been. Still, there’s no new-abnormal consensus to which investors can anchor their expectations. Among strategists at Wall Street banks surveyed by Bloomberg, the highest year-end estimate for the S&P 500 is 4,825 and the lowest is 3,800—a spread of almost 27 per cent.

Even industry veterans who worked their way through the dot-com bubble and the global financial crisis have been shocked and humbled by what’s transpired during a pandemic that’s killed almost 4.5 million people worldwide, and counting.

Julian Emanuel, the chief equities and derivatives strategist at brokerage BTIG who has a 30-year Wall Street résumé, says he felt like he’d seen it all when it came to markets prior to the pandemic. Yet now, he’s at a loss. Not just with the fireworks in the stock market, but also with a bond market that seems to be ignoring what the textbooks—and history—say it should be doing.

Emanuel points out that producer prices are increasing at a 13-year high pace and that the U.S. economy is expected to expand at an annual rate of 6.2 per cent—almost triple the growth in the decade before the pandemic. You’d expect bonds to be selling off aggressively in this environment, to produce yields that can keep pace with both inflation and the investment opportunities available in a high-growth environment. “In what world could you possibly have imagined that 10-year yields would be closer to 1.2 per cent?” he says. “The absolutely impossible is literally commonplace now.”

That leads him to another important lesson: The dynamics of the investing public matter as much as the fundamentals of the companies and economies that are the subject of all the analysis.

In past years, the whims of individual investors weren’t considered to be a major influence on the fate of most stocks or the market as a whole. That changed during the pandemic, because of a confluence of events: a price war between brokerages in late 2019 reduced the cost of placing a trade to literally nothing, just in time for lockdowns to create a surplus of time and money for Americans to dabble in the market.

The number of shares traded by customers of the main retail brokerages rose from 700 million a day before the pandemic to 2.9 billion earlier this year, to account for as much as a quarter of the market’s volume, according to Bloomberg Intelligence. Retail options trading more than doubled. Fueled by influential voices on Reddit and other social media, the new hordes of day traders often pumped up the shares of companies that were teetering on bankruptcy and had been left for dead by professional money managers.

The new breed of individual traders is different from anything Emanuel has seen in the past. “The investing public has become a force unto itself,” he says. “If you ignore the investing public, you’re ignoring them at your peril.”

Of course, one of the older forces has been hard at work as well: The Federal Reserve, which has doubled its balance sheet to US$8.3 trillion by buying Treasuries and mortgage securities during the pandemic, helping to prop up bond prices, and, by keeping interest rates low, make stocks seem attractive. For Paul Nolte, portfolio manager at Kingsview Investment Management, a key takeaway is that—like in Europe and Japan— the U.S. central bank will be more of an influence on markets going forward. The delicate approach that the central bank is taking toward reducing its bond purchases shows that “they can’t seriously raise rates because of the amount of debt that we have,” he says.

For Peter Mallouk, a main lesson from the COVID era is to never lose sight of the big picture by focusing too much on the details. “The last year, the story was very simple,” says the chief executive officer of Creative Planning, which has about US$90 billion in assets under management. “We can talk about a million things, but the only thing that matters is COVID—its mortality rate and our ability to handle it. Every other story is really a derivative.”

One of the most important subplots of the pandemic for Mallouk: “Everyone, because of COVID, got checks.” Small-business owners got Paycheck Protection Program loans. Some big corporations got larger bailouts. Individuals received stimulus checks. Those who lost jobs got enhanced unemployment benefits. “And what did you want to do with that? You went and bought stuff,” Mallouk says.

The economy and the market are still working through that very basic story, which to Mallouk explains some of the wilder investing crazes of the COVID era, such as nonfungible tokens, cryptocurrencies, and meme stocks.

The market will sort itself out at some point as all that excess money dwindles, he says: “We’re not there yet. But that’s what’s coming, and that’s the big picture that really drives everything.”