Jan 4, 2023

Apple's stock is losing its shine after an ugly month of December

, Bloomberg News

These three headwinds will put Apple under pressure in the coming months: Thiago Kapulskis

VIDEO SIGN OUT

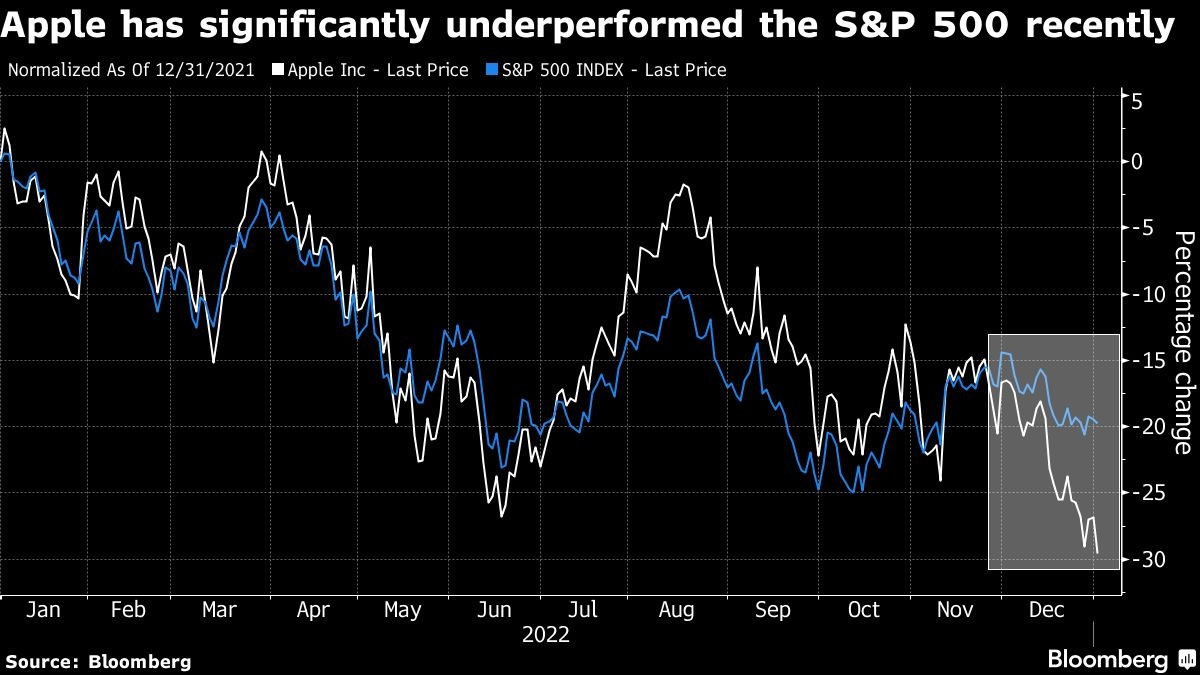

Investors are no longer turning a blind eye to risks facing Apple Inc., an about-face that has taken the iPhone maker's market value below US$2 trillion and threatens more pain for the stock in the months ahead.

Until recently, shares of the world's most valuable company defied much of the gloom that walloped other tech giants in 2022, even as last year represented the worst for the stock since 2008. But now, delays in production of iPhones and concern that demand is weakening as the economy slows are making the stock look more pedestrian by the day. With its valuation still above its average over the past decade, there's plenty of room to fall.

“Apple has been seen as a flight to safety trade and when people kind of throw in the towel that's when they sell Apple,” said Matt Maley, chief market strategist at Miller Tabak + Co. “When we reach a bottom, Apple tends to get washed out and cheap and it's still, if anything, slightly expensive.”

Apple shares are priced at about 20 times profits expected over the next 12 months. While that's down significantly from recent peaks above 30, it's still above the 10-year average of 17 times, according to data compiled by Bloomberg.

The sentiment swing in the stock has been swift. As recently as November, Apple was outperforming the S&P 500, a remarkable feat considering other tech giants like Amazon.com Inc. and Alphabet Inc. had lost more than a third of their values in 2022. Apple's strength was rooted in its massive capital returns to shareholders through buybacks and dividends and the belief that its hard-to-leave ecosystem of loyal customers would insulate the company in a potential recession.

Faith in that argument is cracking, along with investor optimism that the Federal Reserve will soon provide relief from higher interest rates. Apple shares tumbled 12 per cent in December, compared with a drop of 5.9 per cent for the S&P 500 and 9.1 per cent for the Nasdaq 100. It was Apple's biggest monthly drop since May 2019.

The weakness continued Tuesday, after Nikkei reported that Apple told several suppliers to make fewer components for a number of products, given weakening demand. Exane BNP Paribas also downgraded the stock, writing that Apple's growth outlook “seems insufficient to justify a valuation premium to platform peers.”

As a result of Covid-related production snarls in China, Wall Street analysts have been cutting estimates for iPhone sales in Apple's first fiscal quarter, which ended Dec. 31. Last month, JPMorgan Chase & Co. reduced its projection for the second time since early November. Analyst Samik Chatterjee now sees about 70 million units sold, down from a prior estimate of 82 million.

Still, many of the lost sales have likely just been pushed back to the second quarter as supply constraints ease, he said. Indeed, Foxconn Technology Group has brought the world's largest iPhone plant to about 90 per cent of anticipated peak capacity, the official Henan Daily reported this week. And analysts have largely stopped trimming their revenue and earnings estimates now.

Analysts, though, are still catching up to the stock's decline. The average target price for the next 12 months has dropped to about US$173 from US$191 in March. The stock closed Tuesday at US$125.07.