Jun 29, 2022

Central bankers write requiem for low-inflation strategies

, Bloomberg News

We need to keep an eye on what the Fed, oil and food prices do: Strategist

VIDEO SIGN OUT

Risks are mounting that the world is shifting to a regime of higher inflation, forcing central bankers to tear up their playbook of the last 20 years.

That was a key message from Federal Reserve Chair Jerome Powell and his European counterparts on Wednesday as they debated how to tackle persistent price pressures and slower growth.

“I don’t think we are going to go back to that environment of low inflation,” European Central Bank President Christine Lagarde told the ECB’s annual forum in Sintra, Portugal.

“There are forces that have been unleashed as a result of the pandemic, as a result of this massive geopolitical shock we are facing now that are going to change the picture and the landscape within which we operate,” she said during a 90-minute panel discussion moderated by Bloomberg Television’s Francine Lacqua.

Her comments, alongside those of Powell and Bank of England Governor Andrew Bailey, mean a potential upheaval of monetary policy practice. For years, the critical foe facing central bankers was too-low inflation -- pushing them to deploy near-zero interest rates and massive bond purchases to lift their economies during recessions and feeble recoveries.

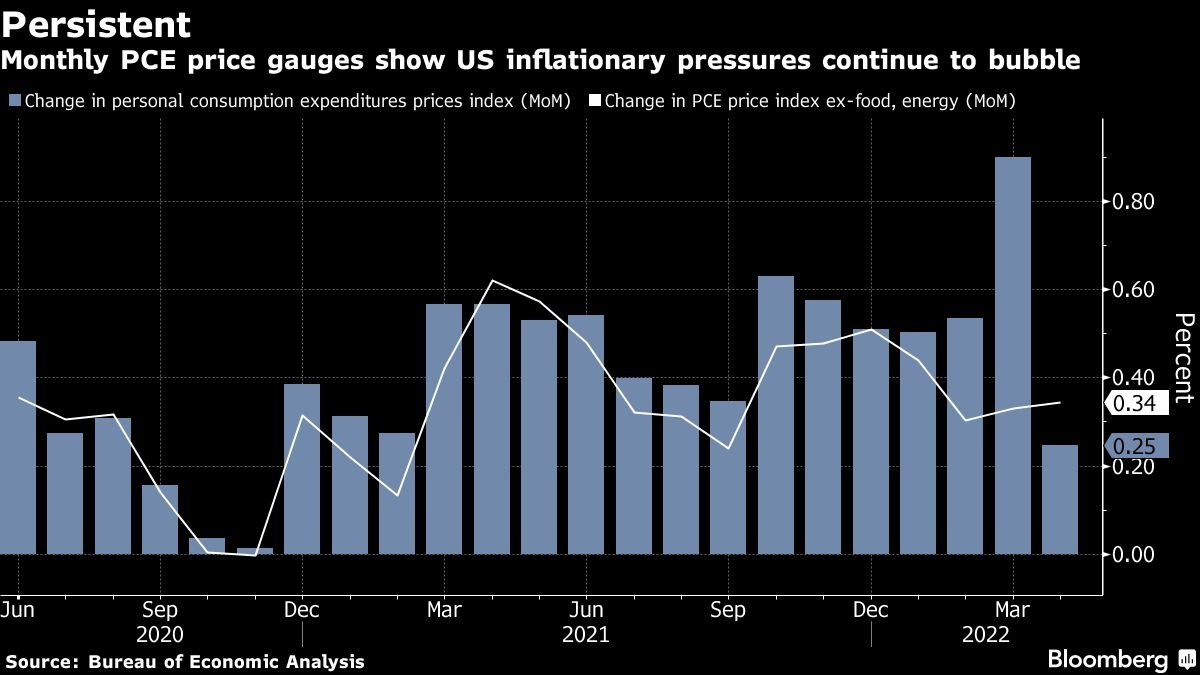

The common enemy now is sizzling price pressures, which have surged to 40-year highs in the US as pandemic-tangled supply chains and Russia’s invasion of Ukraine sink predictions they will prove fleeting, forcing central bankers to hit the brakes: The Fed raised interest rates by 75 basis points this month -- the largest increase since 1994 -- and signaled it could do the same in July.

For Powell and his colleagues, a conclusion that underlying inflation is at risk of drifting higher and becoming unmoored from the Fed’s 2 per cent target could spell an even-more aggressive policy pivot than suggested by their June forecast.

That outlook -- which already shows the most hawkish Fed action since the 1990s, projects rates rising another 175 basis points this year and peaking between 3.75 per cent and 4 per cent in 2023. The following year, however, officials pencil in modest rate cuts as growth moderates and inflation turns back toward target.

Policy makers “are saying there is going to be some pain and we may not get the soft landing we want, but having this high inflation and high inflation expectations is worse,” said Derek Tang, an economist at LH Meyer in Washington. “This is a major shift” and may forestall rate cuts in 2024.

DE-GLOBALIZATION

The Fed chief warned of a “re-division of the world into competing geopolitical and economic camps, and a reversal of globalization” that could result in lower productivity and growth.

The risk of longer-lasting scarcity as the world reorders can already be seen. Inflation rates in the U.S, U.K, and the eurozone are far above their targets and the worry is that they could be persistently so as global trading and production patterns reconfigure.

“It’s how you deal with a series of large supply shocks with no air gap between them, which of course feeds through into expectations,” Bailey said. “Put them all together, they’re not transitory in the traditional sense of the term.”

For decades, advanced economies enjoyed a tailwind from globalization. In the terminology of central banking, inflation expectations were anchored and that allowed central banks to allow labor markets to run hotter. Access to off-shore labor also gutted worker bargaining power, further undercutting inflation but at a social cost as wages stagnated.

“The last ten years were so far the height of the disinflationary forces that we faced,” Powell said. “That world seems to be gone now at least for the time being. We are living with different forces now and have to think about monetary policy in a very different way.”

The Fed in 2020 reorientated its policy approach to tackle the problem of too-low inflation, adopting a strategy that committed to not reacting preemptively to forecasts of higher inflation as the labor market tightened and redefining the full-employment side of its mandate to be broad and inclusive.

Powell acknowledged that the current environment raised questions about whether this approach was still fit for purpose.

“If you want to know the lessons to be learned of the last ten years, look at our framework. Those were all based on a low inflation environment that we had. And now we are in this new world where it is quite different with higher inflation and many supply shocks and strong inflationary forces around the world.”

Central bankers worry that unrelenting price increases could shift households and businesses into a state where expectations are based on more recent inflation experience.

“To the extent that there are a series of shocks, it does become rational for people to pay more and more attention,” Powell said. “The clock is kind of running” on how long the Fed can count on low expectations before they move higher. “We will prevent that from happening.”

In earlier remarks on Wednesday in Sintra, Cleveland Fed President Loretta Mester said officials now face an asymmetric choice, warning that the error of assuming inflation expectations are well anchored when they aren’t is more costly than tightening policy too aggressively to make sure they stay that way.

Jens Weidmann, former President of Germany’s Bundesbank, made a similar argument at a separate event earlier this week in Basel, cautioning against the gradualism that had been a hallmark of central banking until this year.

“The more persistent the shock proves to be, the more the delay in monetary tightening increases the risk that companies, households and workers will start to expect that high inflation is here to stay,” Weidmann said on June 26. “In order to prevent de-anchoring, the persistence of inflation should be overstated rather than understated, and a forceful monetary policy response is advisable precisely when uncertainty about it is particularly high.”

Powell implicitly acknowledged the asymmetric choice -- conceding that officials could err and tip the economy into a recession, but arguing that was the lesser of two evils.

“We are committed to and will succeed in getting inflation down to 2 per cent,” he said. “The process is highly likely to involve some pain. But the worse pain would be from failing to address this high inflation and allowing it to become persistent.”