Oct 11, 2017

Personal Investor: How annuities can make your pension safer

By Dale Jackson

If you are one of the dwindling number of Canadians with a defined benefit pension, congratulations. You probably don’t have to worry about outliving your savings because payments are guaranteed for the rest of your life.

If you’re one of the growing number of Canadians with a defined contribution pension – well, congratulations, too. You’re better off than most Canadians without a workplace pension. However, the amount you save might not be enough to last for the rest of your life.

In a company-sponsored defined contribution plan (DC), regular contributions are put into an investment account with a third party. In many cases the employer will match your contribution. How well a DC pension plan performs depends on how well it is invested and what the markets are willing to give. When you retire, you and your DC pension are on your own.

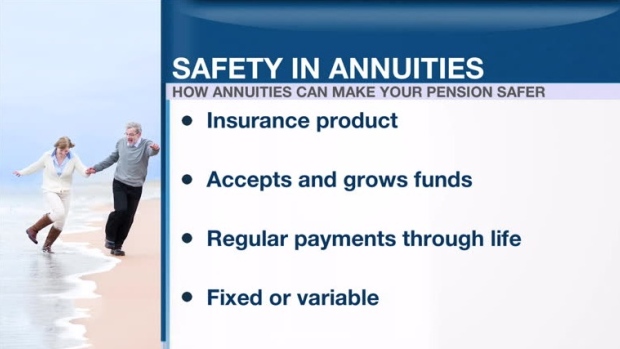

That’s when annuities can potentially give your DC pension the security and reliability of a defined benefit pension. An annuity is an insurance product that the plan holder contributes to over several years. In return, regular payments are guaranteed for a set period of time.

Annuities can be structured in many different ways according to the individual needs of the client. Premiums are set according to projected needs. Payments can be fixed or variable to take advantage of strong markets. They could last for the lifetime of the client or the client’s spouse, depending on how they are structured. An annuity can also act as a life insurance policy that pays out when the client dies.

Many annuities can be a portion of a defined contribution pension, giving the investor a mix of security and the ability to benefit from investments that do well.

Security has a cost, however. In this low interest rate environment annuities tend to provide small returns.

As always, speak with a qualified financial advisor.