Dec 6, 2021

Fed says inflation is higher than expected and that means bad news for bond investors

By Larry Berman

Larry Berman's Market Outlook

VIDEO SIGN OUT

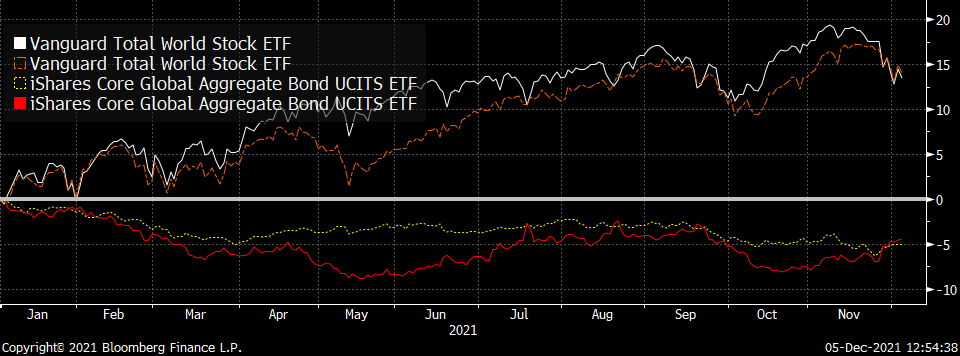

There is no alternative is the narrative that many talking heads will say when it comes to stocks and 2021 was no exception. Stocks globally are crushing returns on fixed income markets globally. Two benchmark ETFs we follow (VT-Vanguard Total World Stock ETF) and (AGGG-iShares Core Global Aggregate Bond ETF) that trades in London in U.S. dollars prove the point. In the chart below, we price these U.S. dollar ETFs in Canadian dollars as well. On a YTD basis, the currency impact is about neutral, but the differences between the white (US$) and orange (C$) equity returns are clear. In the case of global fixed income, we see the currency impact in the differences between the red line (US$) and yellow line (C$) returns.

For traditional bond investors the next few years or longer look bleak. After inflation, bond investors will likely loose money for the foreseeable future. What is an investor to do for the safe money in their portfolios? This week we will see record year-on-year inflation numbers for headline 6.7 per cent and core 4.9 per cent US CPI data last seen in the 1970s and early 1980s.

In the post COVID era, after a year of begging for more inflation, monetizing trillions of dollars, telling us it’s transitory, we hear from newly renominated Fed chairman Powell last week saying, “It’s time to say goodbye to the term ‘transitory’ when it comes to inflation.” They stirred the hibernating inflation beast and now DO NOT have the tools to deal with it given the massive leverage in the market and economy without causing a recession. The reason to think inflation will not stay as elevated as it currently is that the natural rate of economic growth (labour force growth plus productivity) continues to weaken, which opens us up for a period of stagflation. All should understand that the vast majority of global growth in the past decade plus since the great financial crisis has been credit expansion under the developing modern monetary theory shift and easy money policies.

But the outlook for all fixed-income is not as dire as it appears. As it turns out, there are alternatives. There are many alternatives. I launched a private credit fund two years ago that focuses on extracting yield and income with a bit of growth from lending in secured mortgages to residential, commercial and corporate borrows in addition to land development. The fund is only available to private clients of www.QWealth.com partners and is not publicly available and is a fund of funds. Commercial and residential mortgage and asset backed securities as well as public mortgage investment corps are not new asset classes. The private mortgage and lending business is taking off in a big way. The whole area of shadow banking (traditional banking are reducing exposure to many lending areas) is a great asset class that investors need to know more about. The biggest player in this space is the business development corp backed by the government of Canada. Investors can see net yields in the five to 10 per cent range are achievable with significantly less volatility than in public high yield credit markets. Not necessarily less risk, but less volatility. This point is important.

The benchmark for the portfolio of public real estate and infrastructure consists of 40 per cent IVPC – Index of private credit business development corps, 30 per cent MORT- Vaneck mortgage REIT income ETF, 10 per cent GII-S&P Global Infrastructure ETF, 10 per cent PSP-Invesco listed Private Equity ETF, and 10 per cent BBREAPT-Bloomberg Apartment REIT index. In the chart above we show the actual performance of the strategy in red compared to the benchmark in blue and to global fixed-income in grey. Prior to 2019, we are showing the equal weight performance of many of the funds we held in the portfolio two years ago.

There are challenges to the private credit markets for the typical investor. First, liquidity can be restricted. Sometimes the funds suspend redemptions or stop new money from coming in. There was recently a significant fraud in the industry as well. Liquidity can take months or longer to get your money out if you need it. There are other risks too. It’s not a government bond or a high grade large public corporation you are lending money to. But the additional yield and the lack of public market volatility is an attractive feature that will appeal to many investors. Many investors do not know this, but a significant and growing part of your Canada Pension or other pension systems like Ontario Teachers, Caisse de depot et placement du Quebec or private plans are significantly increasing allocations to these alternative credit classes. Here is a website to do some of your own research in the asset class called the Private Debt Investor.

The final week (Dec. 9 at 7 p.m. ET) of our Fall 2021 virtual roadshow will feature a deep dive into the private credit asset class. We think investors need to take a close look at the sector for their fixed income needs. Get your questions ready as the Fall 2021 Investors Guide to Thriving Virtual Roadshow continues. Looking for more yield in your portfolio? You will not want to miss this event.