Oct 30, 2018

Powell's most powerful protector from Trump may be Wall Street

, Bloomberg News

The ultimate guarantor of job security for presidential whipping boy Jerome Powell may lie not in Washington, but on Wall Street.

President Donald Trump could confront a huge blow back from the financial markets -- with stocks, bonds and the dollar all going down -- if he made a serious move to oust the Federal Reserve chairman, market professionals say.

“There would be a very bad reaction in the markets,” said Jim Paulsen, chief investment strategist at Leuthold Weeden Capital Management LLC in Minneapolis. Such a move “would introduce an incredible amount of uncertainty.”

The president has been withering in his criticism in recent weeks of Powell and the Fed for raising interest rates, calling the central bank the biggest threat to the economy. Asked by The Wall Street Journal on Oct. 23 if he would consider removing the Fed chair, Trump replied, “I don’t know.”

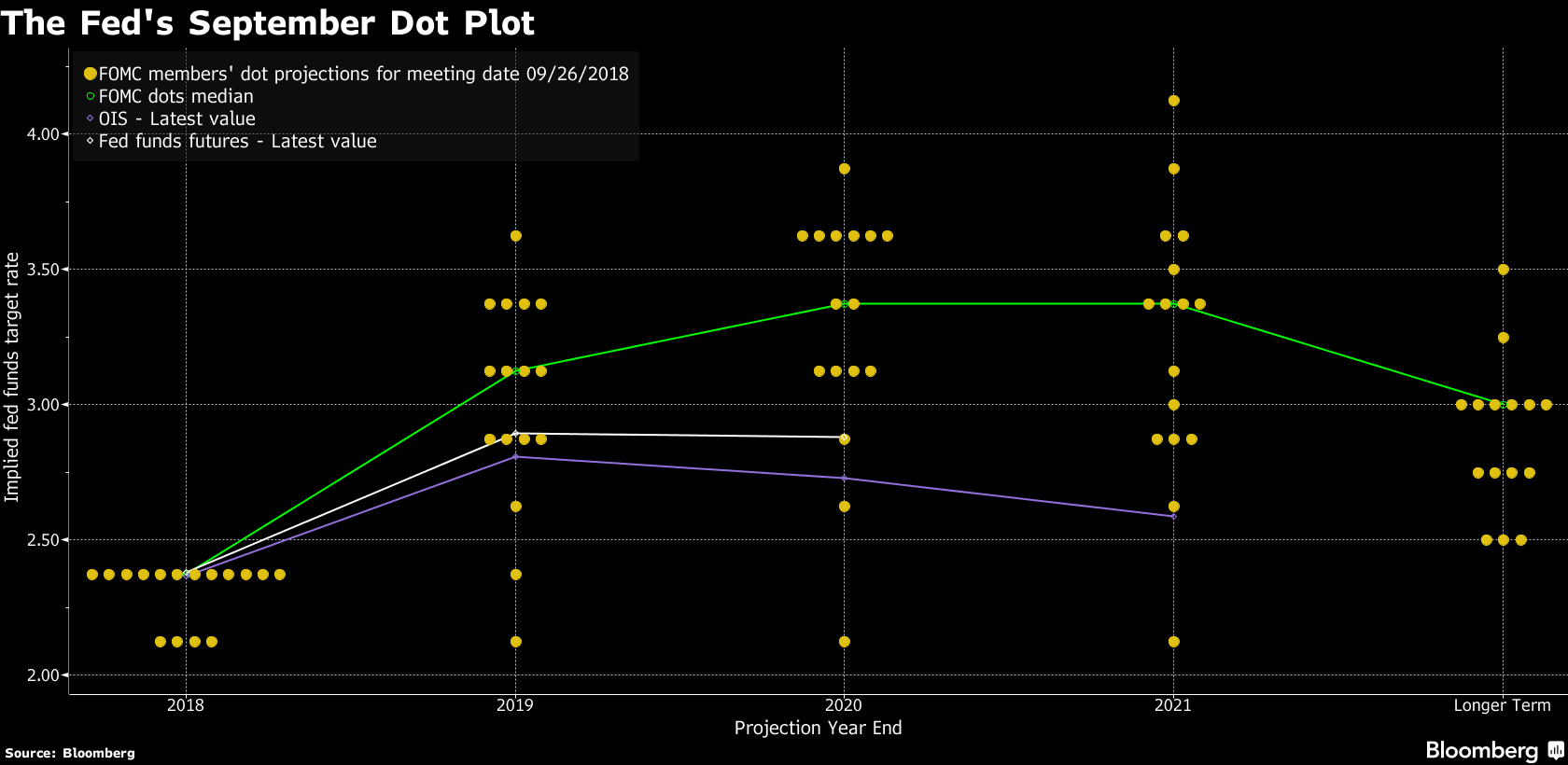

Powell and his team have responded to the attacks by saying they’ll do what they think is best for the economy and not be swayed by politics. And what they think is best for now is to continue gradually raising interest rates.

Under the law, Trump can fire members of the Fed’s board “for cause” -- an amorphous concept that’s generally come to mean inefficiency, neglect of duty, or malfeasance.

But it’s not clear whether that requirement applies to the job of Fed chair, opening up the possibility that Trump could unseat Powell over policy differences as the central bank’s leader, without removing him from the board.

So far, investors have mostly shrugged off the president’s attacks on the Fed and his calls for it to stop raising rates.

“People have gotten used to a certain amount of rhetoric and grandstanding and statements that are meant to influence the masses, without necessarily having any real policy impact,” said Peter Tchir, head of macro strategy at Academy Securities. “So I’d say the market right now dismisses it.”

Presidential pressure on the Fed is not unprecedented. While Trump’s immediate predecessors -- Bill Clinton, George W. Bush and Barack Obama -- did refrain from publicly chastising the central bank, those who came before them were not so reticent.

But an overt effort to unseat Powell as Fed chairman would be something else altogether.

“The unintended consequence of a concerted and believable attempt to remove Chairman Powell from office could be quite consequential for financial markets,” Diane Swonk, chief economist at Grant Thornton LLP in Chicago, said in an email. “We would be in uncharted waters, something markets hate.”

Christopher Dillon, multi asset specialist with T Rowe Price Associates Inc., basically agreed.

“What it would represent is a breakdown in the systematic process that helps guide markets, and once you lose faith in that construction, that’s where we would have concern,” he said.

He sees a risk of inflation and bond yields surging if Trump replaces Powell with a more dovish chairman at the same time the government is heading toward a trillion-dollar budget deficit. That in turn would upend stocks.

“If you can go ahead and get to 4-4.5 per cent from a 10-year Treasury what do I need my equity investment for?” Dillon asked. Ten-year yields were around 3.08 per cent on Monday.

The experience of some emerging markets may be instructive. Turkish President Recep Tayyip Erdogan damaged his country’s economy, creditworthiness and currency with his ham-handed threats against the central bank earlier this year.

The U.S. is no emerging market, of course. Indeed, some analysts think U.S. markets might not do that badly if Trump replaced Powell with a Fed chair opposed to tighter credit.

“Some investors might celebrate that the Fed is not going to take the punch bowl away,” said Jack Ablin, chief investment officer at Cresset Wealth Advisors in Chicago.

The dollar, though, could be hit as foreign investors lose faith in the U.S., he said.

Academy Securities’ Tchir acknowledged that a shift in Fed leadership could be beneficial for the markets, but argued it would be swamped by the uncertainties arising from an assault on the central bank’s independence.

“Even though in theory it would be helpful -- because you’d clearly be taking that step to put someone dovish in -- it would be just such a radical change and deviation from the norm that volatility would have to increase and that would put pressure on assets,” he said.

in New York, U.S., on Friday, Oct. 26, 2018. The slide in U.S. stocks picked up speed, with the S&P 500 Index extending losses from its September record to 10 percent, as disappointing reports from technology bellwethers added to this week's turbulence in financial markets. Photographer: Michael Nagle/Bloomberg, Bloomberg")