Aug 31, 2022

U.S. stocks end a turbulent month on a down note

, Bloomberg News

BNN Bloomberg's closing bell update: August 31, 2022

VIDEO SIGN OUT

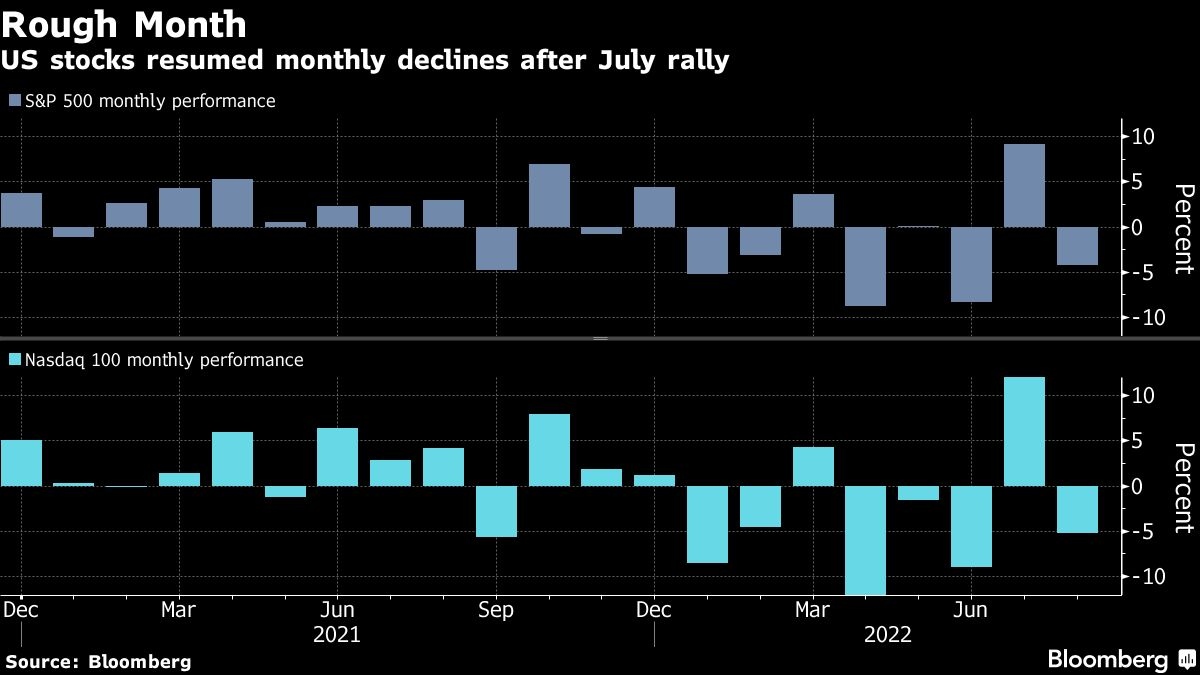

US stocks and bonds ended a turbulent August lower as traders recalibrated rate-hike expectations after central banks across the globe vowed to step up their fights against inflation.

All major US indexes had their worst month since June. Treasuries in August faced their biggest monthly loss since April as the Federal Reserve resolved to stay hawkish. Oil posted a third monthly drop -- the longest losing streak in more than two years -- hampered by the likelihood of slower global growth.

Federal Reserve officials in recent days quashed hopes of a dovish pivot, a view that had helped fuel bets that this year’s bear market is over. Since then, investors have been sifting through sometimes-conflicting economic data for further policy clues. While job openings data on Tuesday underscored tightness in the labor market, revamped ADP data on Wednesday showed US companies increased headcount at a relatively sluggish pace in August. All eyes will be on the job report on Friday for further hints about the central bank’s path.

“Now that the Jackson Hole dust is settling, markets have gained clarity on today’s investment question,” said Florian Ielpo, head of macro research at Lombard Odier Asset Management. “Yesterday’s question was ‘will inflation level down’ when today’s is ‘how big will the needed slowdown be.’ For now, markets are pricing a marked slowdown, not a fully-fledged recession.”

The Fed has ditched its soft-landing goal and is instead aiming for a “growth recession,” which would mean a protracted period of meager growth and rising unemployment.

Euro-area inflation accelerated to another all-time high, strengthening the case for the European Central Bank to consider a jumbo interest-rate hike when it meets next week. ECB Governing Council member Joachim Nagel urged a “strong” reaction. Money markets have now priced in 125 basis points of tightening from the ECB by October, which implies a half-point hike and a three-quarter point increase spread over its next two policy decisions.

Investors are also contending with mounting friction between Beijing and Taipei after Taiwanese soldiers fired shots to ward off civilian drones and evaluating the latest Chinese data, which indicated factory activity shrank for a second month. Power shortages, a property sector crisis and Covid outbreaks all took a toll.

Here are some key events to watch this week:

- ECB Governing Council members due to speak at event Tuesday through Sept. 2

- China Caixin manufacturing PMI, Thursday

- US nonfarm payrolls, Friday

- UK leadership ballot closes Friday. Winner announced Sept. 5

Some of the main moves in markets:

Stocks

- The S&P 500 fell 0.8 per cent as of 4 p.m. New York time

- The Nasdaq 100 fell 0.6 per cent

- The Dow Jones Industrial Average fell 0.9 per cent

- The MSCI World index fell 0.8 per cent

Currencies

- The Bloomberg Dollar Spot Index was little changed

- The euro rose 0.3 per cent to US$1.0049

- The British pound fell 0.3 per cent to US$1.1616

- The Japanese yen was little changed at 138.91 per dollar

Bonds

- The yield on 10-year Treasuries advanced six basis points to 3.16 per cent

- Germany’s 10-year yield advanced three basis points to 1.54 per cent

- Britain’s 10-year yield advanced 10 basis points to 2.80 per cent

Commodities

- West Texas Intermediate crude fell 2.8 per cent to US$89.09 a barrel

- Gold futures fell 0.9 per cent to US$1,721.40 an ounce

in front of the New York Stock Exchange (NYSE) in New York, U.S., on Thursday, Nov. 18, 2021. Photographer: Michael Nagle/Bloomberg, Bloomberg")