Feb 16, 2021

Why the future is bright for nickel exploration

- As the electric vehicle (EV) market continues to grow, renewable energy and minerals associated to it such as copper, nickel and cobalt, are increasing in price

- The current market for EVs has yet to be sizeable as battery improvements continue to develop, however the sector can accelerate worldwide electrification

- British Columbia and Nevada have significant nickel deposits with B.C. being host to multiple operating mines with experienced teams

As recently reported in the Financial Post on January 28, 2021, journalist Peter Tertzakian writes an in-depth article entitled, “Another commodity super cycle is coming – this time driven by renewable energy and EVs.”

The article explains that the transition to a global electrified clean energy economy is going to result in a monumental draw on metals and minerals from the earth's crust. Notably, prices of copper, nickel, cobalt, platinum and rare earth elements are all inflating as electric vehicles and the wider electrification trend starts pulling on constrained resources.

With dozens of electric vehicle manufacturers at various stages of development around the world, EV car sales volumes are predicted to substantially increase. Here, Tesla Inc. is the clear EV market leader with over 500,000 vehicles sold last year alone, and with notification of companies like Volkswagen AG, BMW, and General Motors Co. devoting billions to EV design and manufacturing, the market is expected to accelerate considerably by mid-decade.

Upstart and established car companies are collectively raising billions of dollars to roll out new models. Expectations for EV sales are at all-time highs, and now those expectations are impacting the resource sector, leading to investment analysts speaking openly about a forthcoming “commodity super cycle.”

This is starting to happen, even though current EV sales have not yet achieved a sizable market share of overall car sales, due to the fact that improvements in battery storage technologies have created an acceleration to the overall electrification of the global economy.

Furthermore, the resource world doesn’t move nearly as fast as the technology world, which is why commodity value is now chasing technology value.

And the larger lesson is that the new economy can’t go anywhere without the old. You don’t need a PhD in Economics to realize that the transition to an electrified clean energy economy is going to result in a surge in demand for additional metals and minerals from the earth’s crust.

It is going to result in dramatic metal commodity price increases. In the past few months, rising commodity prices are a wake-up call to that reality.

The increased use of key energy metals like nickel, cobalt and lithium will continue to lead to future demand and commodity price increases which result in good news for energy metal explorers.

Sure, the challenges can be overcome. When commodity prices rise, more resource projects are permitted, financed and built, often in unsavory places.

That is why nickel exploration companies, like Nickel Rock Resources (TSXV: NICL | OTCQB: NIKLF), who both explore for these valuable metals and operate in ethical mining jurisdictions within North America, are highly sought after by multi-national companies focused on energy metals like Glencore PLC (LON: GLEN) and Tesla Inc. (NASDAQ: TSLA).

Nickel Rock is a Canadian based exploration company whose primary listing is on the TSX Venture Exchange. The company maintains a focus on exploration for high value battery metals required for the electric vehicle market.

The company recently announced several acquisitions resulting in a significant property package prospective for awaruite, a naturally occurring nickel-iron alloy important in the manufacture of environmentally efficient batteries for the electric vehicle markets globally.

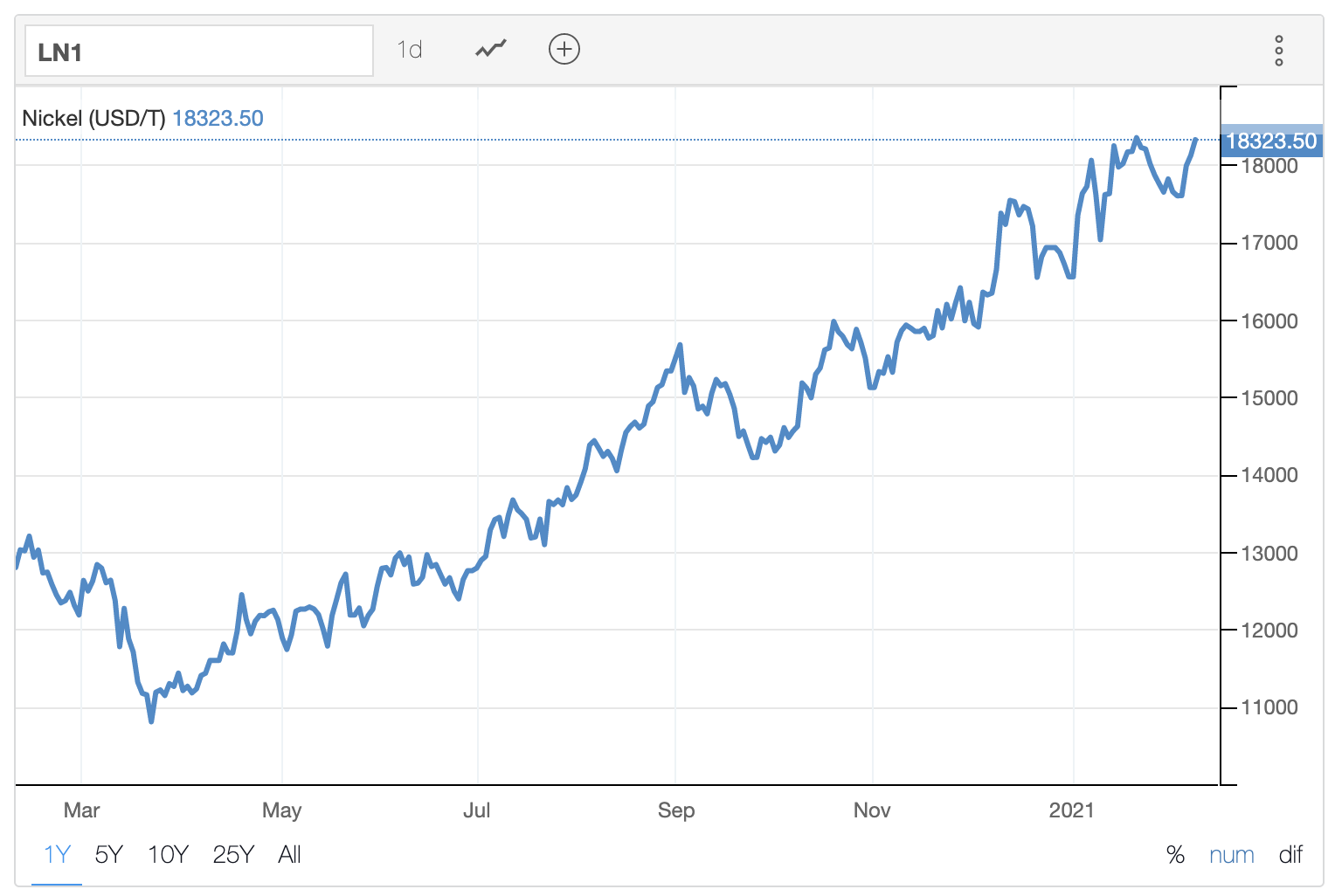

Due to a decline in nickel prices between 2011 and 2015, several nickel mining companies either mothballed their locations or moved exploration and production outside North America.

This resulted in a reduction in the number of nickel stocks to buy in Canada or the U.S. Since 2016, the price of nickel has firmed up significantly, and more recently the commodity price of nickel is approaching its five-year high.

With the significant rise in the nickel price since the beginning of 2016, Nickel Rock is one of the few dual-play nickel/lithium stocks on the TSX or the TSXV.

British Columbia nickel exploration projects

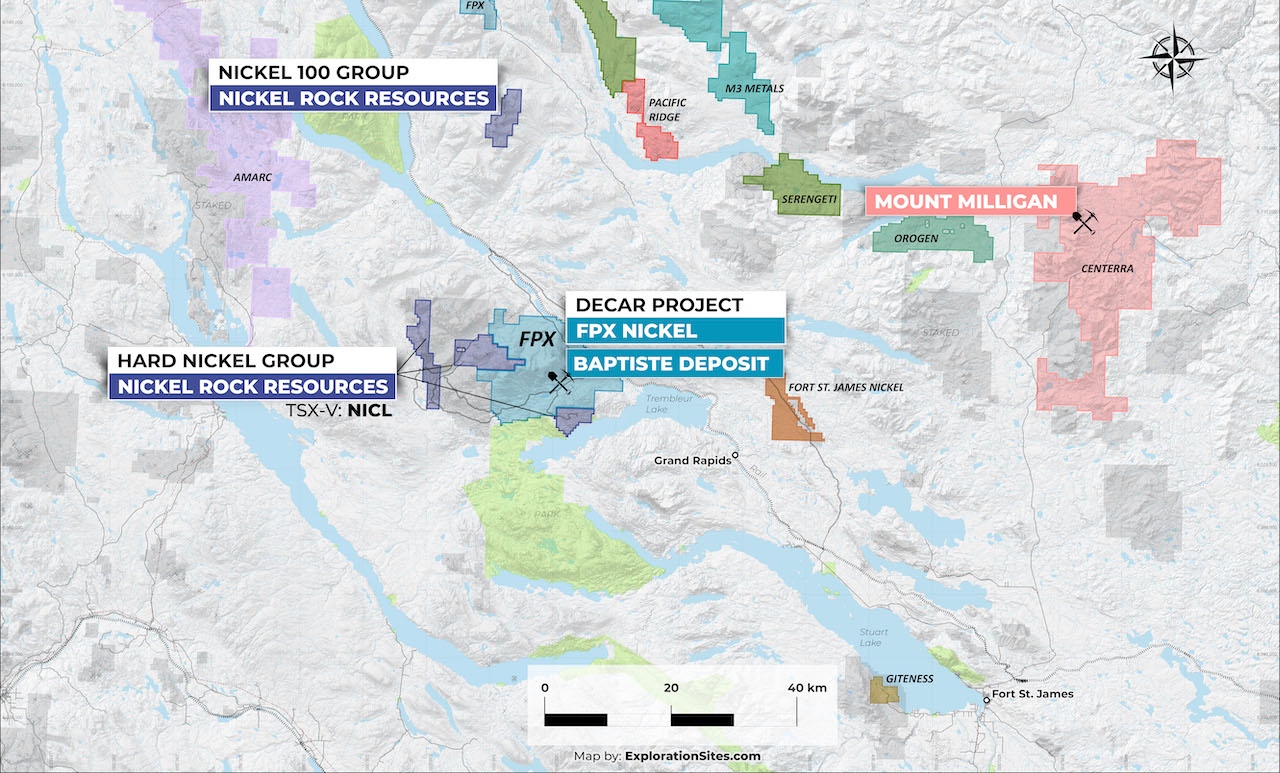

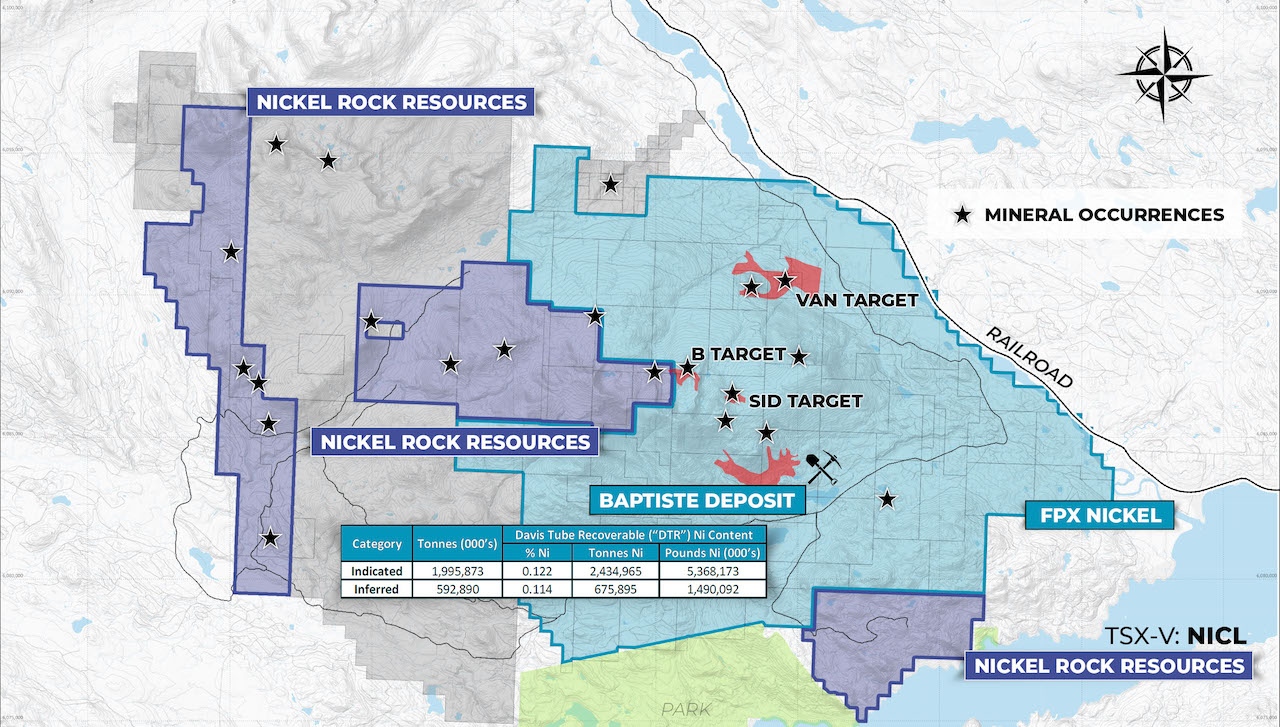

The Nickel Rock mineral claims are partially underlain by rocks like those hosting the Decar project of FPX Nickel (TSXV: FPX) where mineralization includes nickel, cobalt, and chromium.

The Hard Nickel Group consists of five claim blocks in four groups with a total area of 6,125.32 ha in the area surrounding Mount Sidney Williams. These properties both adjoin or are near the Decar Project of FPX Nickel located 100 km northwest of Fort St. James, B.C., in the Omineca Mining Division.

Metallic mineralization occurring in the claim group includes nickel, cobalt, copper, and chromium. Significantly, some nickel mineralization occurs as awaruite.

The earliest publicly available reports of exploration on and around the Hard Nickel Group Property dates from 1974 and were focused on evaluating the potential of the area to host chromite (used in the production of stainless steel) and gold deposits.

Systematic, ground-based exploration work began in 1987 in the Mount Sidney Williams area under the direction of renowned geologist, Ms. Ursula Mowat, recipient of the “Spud Huestis Award” for her discovery of the adjacent Decar Nickel Deposit.

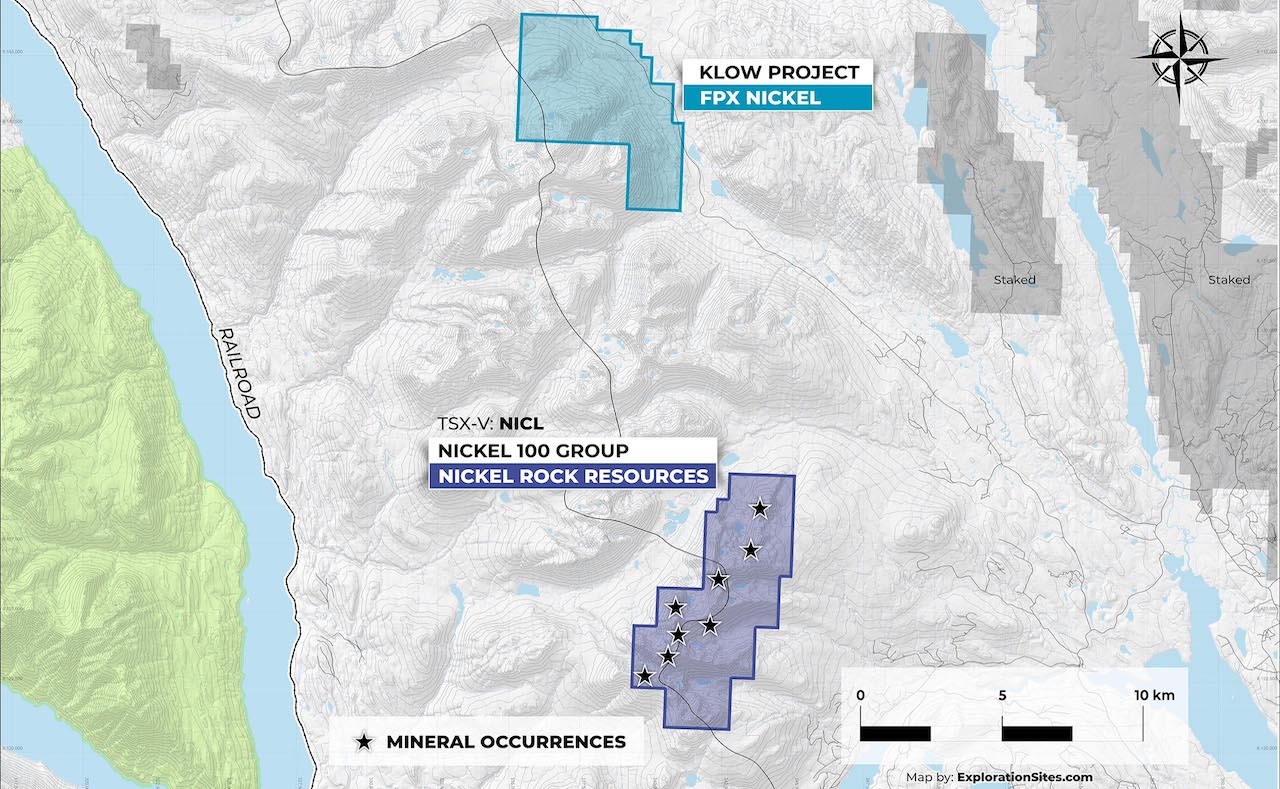

The Nickel 100 Group consists of two contiguous claim blocks covering 3,134.70 ha with many identified mineral occurrences of chromite that have associated nickel along with trace amounts of Platinum group elements (PGEs) and is situated approximately 130 km northwest of Fort St. James in Central British Columbia.

Forestry roads and helicopters provide primary access to the property. A BC Rail Line is located approximately 12 km to the south.

Nickel 100 Group: Nickel-cobalt-chromium mineralization has not been well-explored, but the presence of awaruite has been documented. Geologist, Ursula Mowat completed a preliminary field work program over the area in 2004, and confirmed the presence of elevated nickel, cobalt, chromium, platinum and palladium values in rocks and stream sediments.

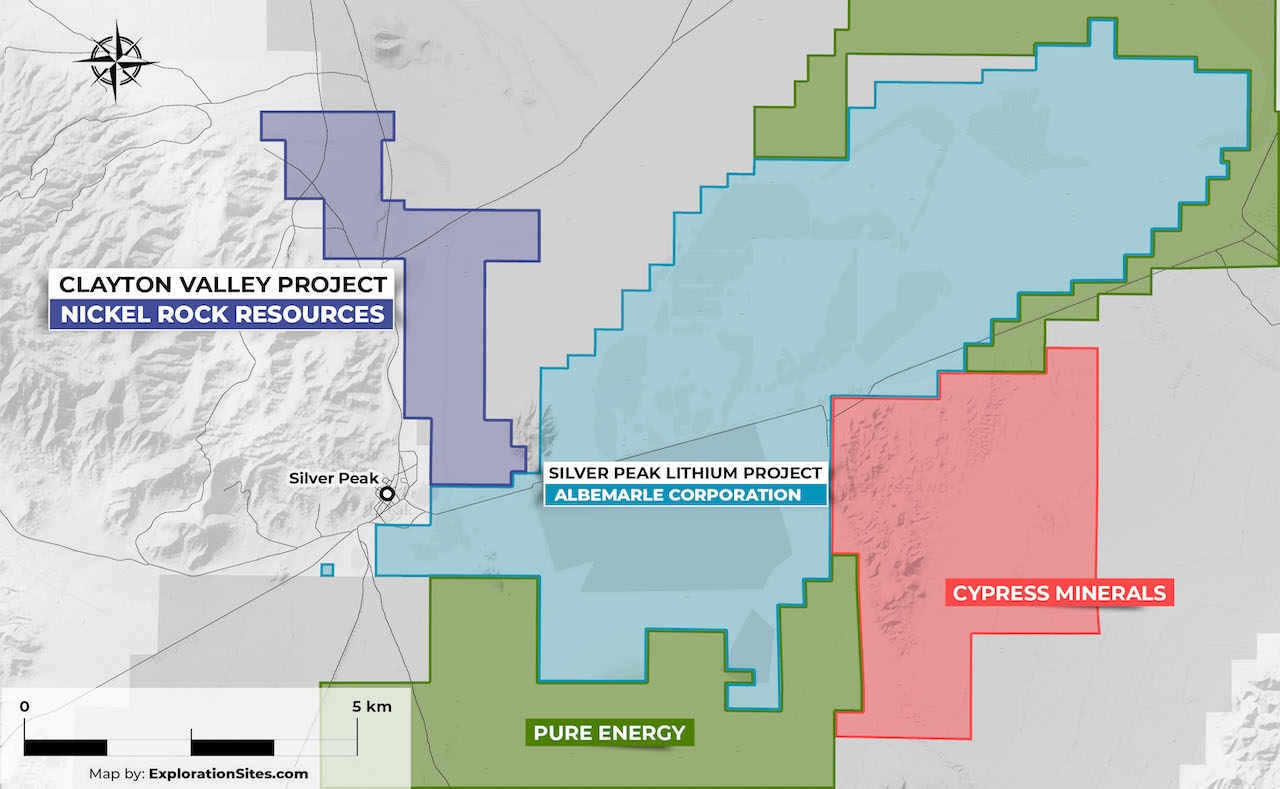

Clayton Valley, Nevada Lithium Project

Nickel Rock is also exploring for commercially important groundwater deposits enriched in dissolved lithium on its Clayton Valley project at Silver Peak, near Tonopah, Nevada.

In Clayton Valley, all producing lithium brine deposits share several first-order characteristics: (1) arid climate; (2) closed basin containing a playa or salar; (3) tectonically driven subsidence; (4) associated igneous or geothermal activity; (5) suitable lithium source-rocks; (6) one or more adequate aquifers; and (7) sufficient time to concentrate a brine.

The company’s Clayton Valley Project is an early-stage lithium brine prospect in Esmeralda County, Nevada. A total of 77 placer claims covering about 640 ha (1,500 acres) were staked over the western side of the Clayton Valley playa.

The property position covers an inferred graben bounded by the Silver Peak range front on the west and Goat Island on the east. The exploration concept is the graben is a sub-basin of the larger Clayton Valley basin and may represent a secondary trap for lithium brines within the greater system.

Located contiguous and adjacent to Nickel Rock Resource’s Clayton Valley Project, the Silver Peak Lithium Brine Mine and Processing Facility has been in production since 1966 using traditional evaporation pond technology and is the only producing lithium brine deposit in North America.

Albemarle Corporation (NYSE: ALB) purchased the mine as part of its acquisition of Rockwood Lithium that closed in early 2015. The United States Geological Survey estimates that over 300 million pounds of lithium carbonate have been produced at this facility since 1966.

Advantages of exploration in British Columbia

There are several advantages of conducting mining operations in British Columbia. The area we are interested in has generated several promising projects and is the subject of significant exploration expenditure in 2021.

In addition, B.C. is host to numerous operating mines, good infrastructure, power plus experienced exploration and supporting services. Nickel Rock’s exploration team believes that its land position is strategically situated near to the Decar nickel deposit and a recent compilation of data from past exploration programs suggests it may host similar type of mineralization.

In 2019, the Mining Journal of London gave British Columbia the title of Least Risky Global Mining Jurisdiction and the B.C. government has made some big infrastructure investments including a CAD$736 million investment in power line transmission to the north and made permanent a popular flow-through tax benefit investment incentives which encourages significant investment in exploration.

The fact that large global mining companies like Newmont Goldcorp (NYSE: NEM) are investing in the Galore Creek Partnership with Teck Resources (TSE: TECK.B), means that there is significant interest in mining investments within British Columbia.

Newcrest Mining Limited (ASX: NCM) has invested USD$806.5 million to buy 70 per cent of the Red Chris Mine from Imperial Metals Corp (TSX: III) inside B,C.’s prolific mining regions.

Nickel Rock’s near-term focus

During the upcoming period 2021-2022, Nickel Rock will direct its mineral exploration efforts on the advancement of its nickel properties in central British Columbia, Canada.

The immediate area has incredible potential for a major nickel resource, as evidenced from the period of November 2009 to November 2015. The company’s neighbour, Cliffs Natural Resources spent approximately USD$22 million to earn its 60 per cent interest in the Decar property.

As such, Nickel Rock believes that this area of the world is the most attractive undeveloped nickel region and that it’s truly a tier-1 asset due to the size of the nearby ore bodies (supporting a top-15 annual nickel producer over a 25+ year mine life) and bottom-quartile operating costs.

The company’s nickel exploration strategy is to continue to demonstrate the technical and economic feasibility of the project, and to commence the permitting process, so that as the nickel price continues to rise, and subsequently the market will begin to value Nickel Rock Resources’ stock more appropriately.

This will give the company a better basis on which to raise funds to advance the project on its own, or to advance the asset with a senior partner.

Awaruite and the potential to make nickel mining carbon neutral

The mineral awaruite is both highly magnetic and very dense, and is therefore amenable to concentration by mechanical processes including magnetic and gravity separation.

This style of deposit is unique and presents considerable metallurgical and processing cost saving advantages. Significantly, the awaruite found in the Trembleur formation occurs in a serpentinized ultramafic rock.

In 2018, G. Dipple at the University of British Columbia began the Geoscience B.C. funded research project entitled, “Carbon Mineralization Potential Assessment for B.C.,” scheduled for completion in early 2021.

In late 2020 a preliminary assessment report was published. One of the key items from the report was “The use of reactive serpentinite tailings from nickel mining as a carbon sink has the potential to make nickel mining carbon neutral or a net carbon sink.”

The presence of serpentinized ultramafic rocks of the Trembleur intrusions has been repeatedly documented in the areas covered by the claims of the Nickel Rock Project, as well as at FPX Nickel Corp.’s Decar Project, according to the report.

Nickel production in Canada and the U.S.

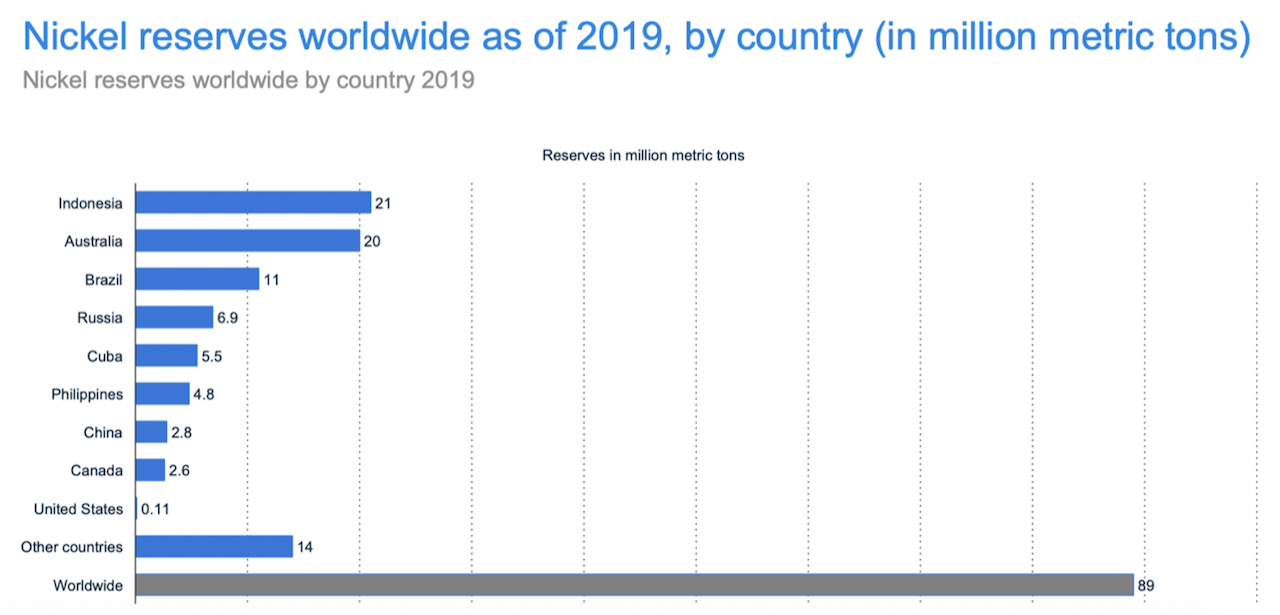

Nickel was first discovered in Canada in 1883 and began being mined the 1890’s. Today the nation is one of the world’s five top nickel producing countries with Indonesia being the largest producer of nickel worldwide.

Recently, Indonesia’s decision to ban the export of nickel has contributed to the rise in global nickel commodity prices. At present, there are approximately four operating nickel mines in Canada, and one operating nickel mine in the U.S.

The nickel mining companies operating these nickel mines include large and mid-sized global diversified groups include Glencore PLC (LSE: GLEN), Vale S.A. (NYSE: VALE) and Lundin Mining (TSE: LUN). Nickel Rock Resources and FPX Nickel are one of the few junior nickel mining companies in Canada.

Nickel and its compounds are essential for the manufacture of countless products that we rely on daily. Reflecting this vast use, Canada’s nickel and nickel-related products are exported to more than 100 countries.

In 2017, Canada produced an estimated 211,925 tonnes of nickel in concentrate from nickel mines located in Newfoundland and Labrador, Quebec, Ontario, and Manitoba.

Canada also produced 163,200 tonnes of refined nickel at four refineries located in Fort Saskatchewan, Alberta; Thompson, Manitoba; Sudbury, Ontario; and Long Harbour, Newfoundland, and Labrador.

According to the Government of Canada, global mine production of nickel in 2017 was estimated at 2.1 million tonnes; Canada ranked fifth, with 10 per cent of global mined production.

Canada’s total nickel production continues to increase year over year, and in 2018 Canada ranked fifth in the world for mine production and for the production of refined nickel. Canada currently produces around 15 per cent of the world’s nickel production and the country’s exports of nickel and nickel-based products were valued at $4.2 billion in 2018.

Most of Canada’s nickel exports go to the U.S. (41 per cent), China/Hong Kong (21 per cent), Belgium (7 per cent), the Netherlands (7 per cent) and the remainder is shipped to 23 other countries worldwide.

Nickel and the Growth of EVs

It can be assumed that Nickel Rock’s assets will continue to grow in value due to the predicted emergence of the electric vehicle market.

For instance, a Tesla Model 3 requires 30 kg of nickel for its on-board battery (80 per cent of the battery metal constituents). Nickel is considered by many to be the single most important component in battery fabrication.

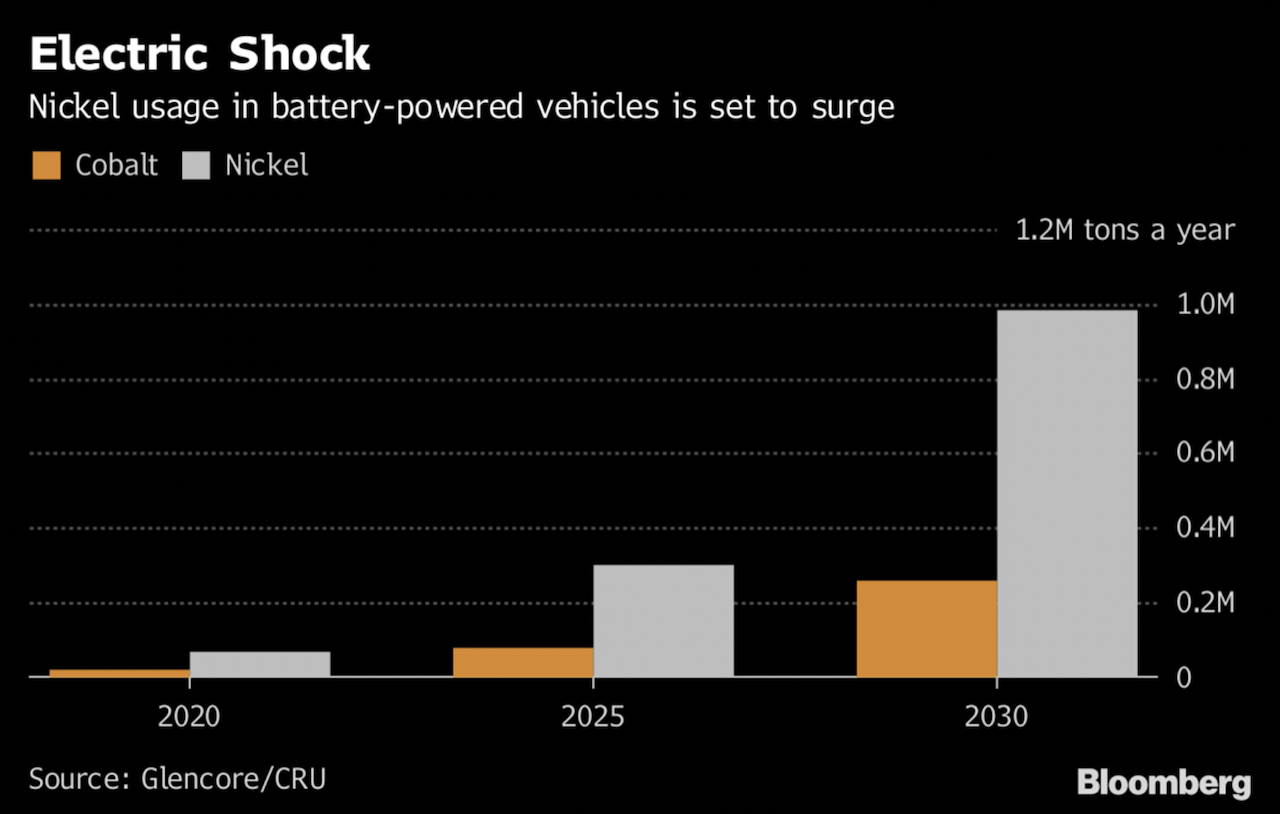

EVs are expected to drive a large part of this increased future metals demand. Globally EVs are projected to grow from a small number today to 140 million vehicles by the year 2035.

China plans to ban the sale and production of gasoline powered cars by the year 2040, as it grapples with ways to improve overall air quality and China is expected to be the largest global market for EVs.

As can be seen, the future for nickel is certainly bright and the company’s management is extremely bullish on the future demand for this metal and the impact a nickel or lithium discovery may have for its shareholders.

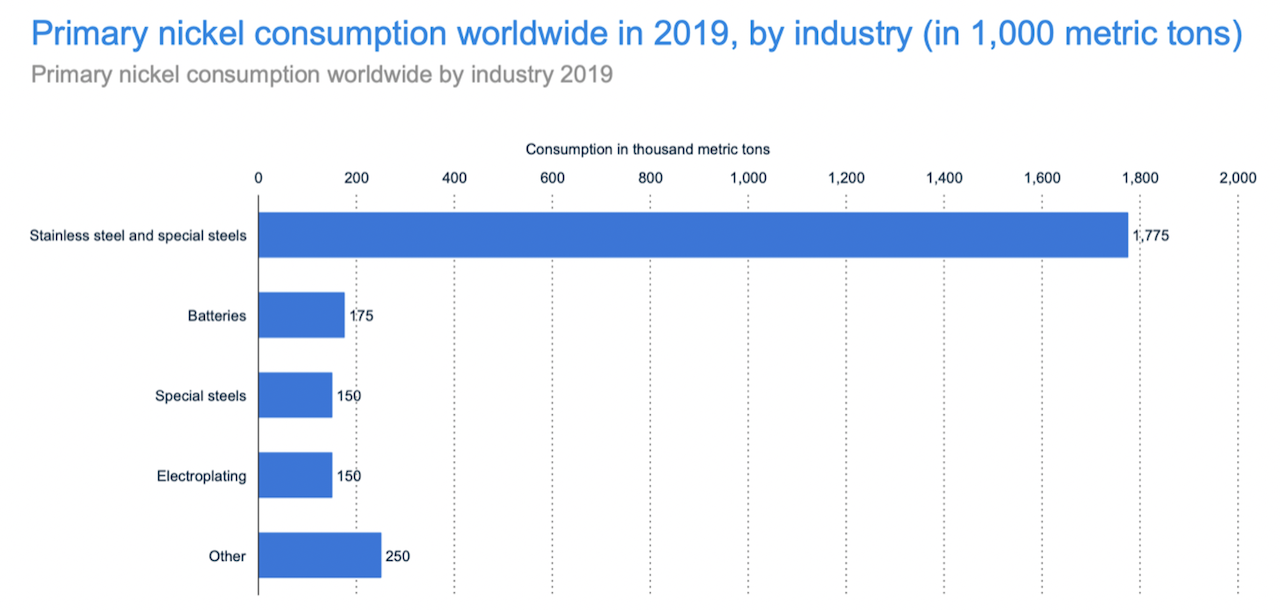

The battery market only consumes three percent (3 per cent) of the world’s available nickel, but that figure is set to grow substantially. Some projections are forecasting that by 2025 there will be more than 140 million EVs on the road, and by 2030 that number could double as the industry is leaning towards batteries with a higher nickel concentration as they tend to last longer.

This makes EVs a more attractive option to consumers and acts as an incentive to make the transition.

Today, the impact of the EV market is small in comparison to stainless steel, but future demands will play a significant role in not only the price of nickel but also in the overall economy, creating jobs and helping the environmental issues we face today.

The fact that awaruite occurs with waste rock potentially having carbon sequestering abilities just adds to the overall positive environmental story which contrasts with most mining operations globally.

As well as the increased demand from the EV manufacturing industry, the demand for clean energy is on the rise in North America. With Canada being a large source of mineral resources and a leading producer of nickel, the country still has several nickel deposits that are relatively untapped and some that are ready to go into production.

"I'd just like to re-emphasize any mining companies out there, please mine more nickel. Wherever you are in the world, please mine more nickel and don't wait for nickel to go back to some high point that you experienced some five years ago or whatever, go for efficiency."

— Elon Musk, CEO, Tesla Inc.

Qualified person notice

Jacques Houle, P.Eng., a qualified person as defined by NI 43 - 101, is responsible for the technical information contained in this release. All scientific and technical information in this article has been prepared under the supervision of Jacques Houle, P. Eng., a consultant, and a qualified person within the meaning of National Instrument 43-101. Readers are cautioned that the information in this article regarding the property of FPX Nickel Corp is not necessarily indicative of the mineralization on the property of interest. The QP has been unable to verify the information in this press release about the Decar property, (such information was publicly disclosed in their PEA dated Sept. 9, 2020) and the QP believes it is reliable.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release. This news release may contain forward‐looking statements which include, but are not limited to, comments that involve future events and conditions, which are subject to various risks and uncertainties. Except for statements of historical facts, comments that address resource potential, upcoming work programs, geological interpretations, receipt and security of mineral property titles, availability of funds, and others are forward‐looking. Forward‐looking statements are not guaranteeing of future performance and actual results may vary materially from those statements. General business conditions are factors that could cause actual results to vary materially from forward‐looking statements.