Nov 14, 2023

Markets today: S&P 500 up 2% as bets 'Fed is done' sink U.S. yields

, Bloomberg News

BNN Bloomberg's mid-morning market update: Nov. 14, 2023

VIDEO SIGN OUT

Stocks climbed while bond yields sank as an unexpected inflation slowdown bolstered bets the Federal Reserve’s aggressive hiking cycle is now over — and the next move will be a cut in mid-2024.

About 95 per cent of the S&P 500 companies rose, with the gauge up nearly 2 per cent. Tesla Inc. led gains in megacaps and Nvidia Corp. rallied for a 10th straight session. Regional banks jumped almost 6 per cent. The Russell 2000 index of small caps added over 5 per cent. Goldman Sachs Group Inc.’s basket of the most-shorted stocks beat the broader market in a sign some traders are preparing to cover bearish wagers. Five-year yields plunged 24 basis points to 4.42 per cent. The dollar fell 1.2 per cent.

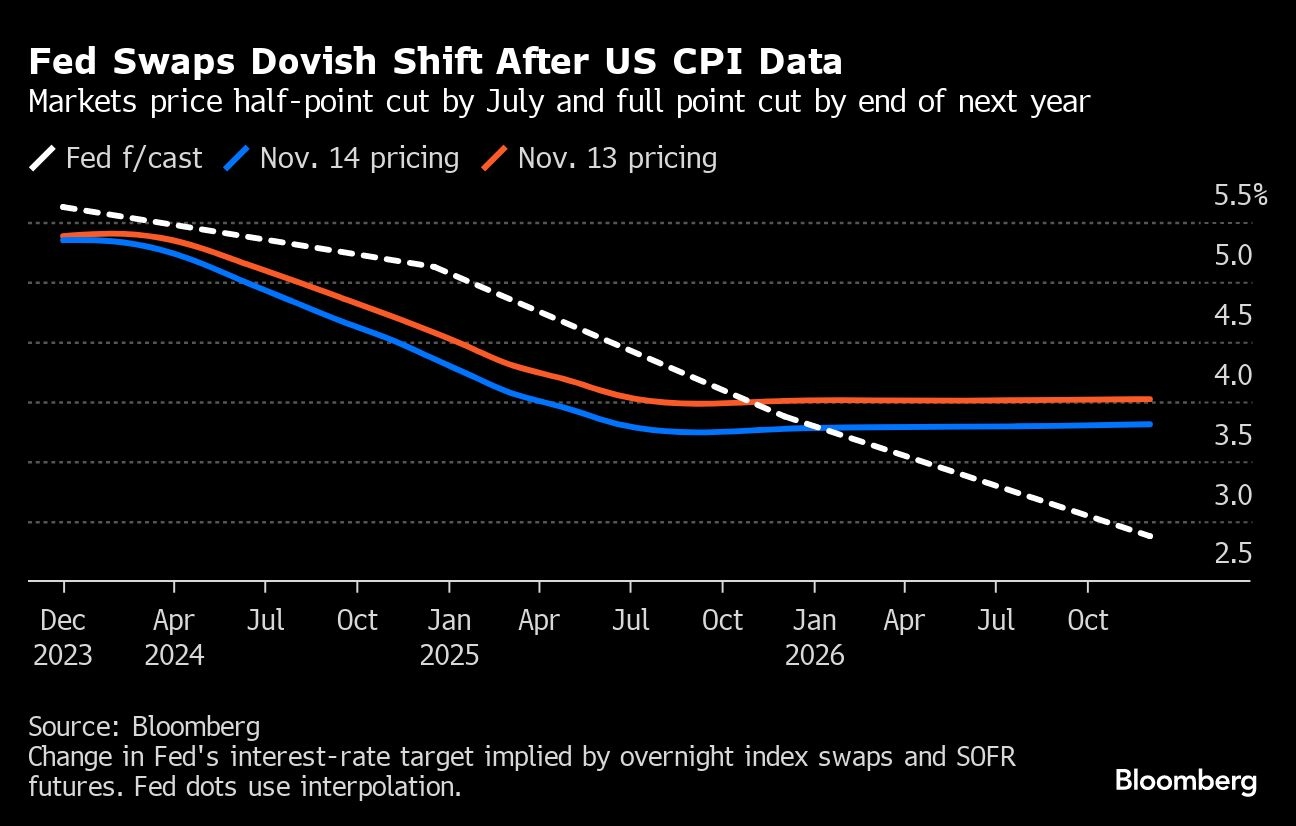

While Wall Street’s rally could risk further easing of financial conditions — and ultimately complicate the Fed’s job — bets on a “pivot” next year have increased. Fed swaps indicate the odds of another hike have fallen to almost zero — with the market pricing in a 50 basis-point rate cut by July.

“The last of investors not convinced the Fed is done are likely ‘throwing in the towel’,” said Bryce Doty at Sit Fixed Income Advisors. “The next Fed action is more likely to be a cut next summer than another rate increase.”

To Chris Larkin at E*Trade from Morgan Stanley, while the cooler-than-expected numbers will likely encourage some investors to start planning for 2024 rate cuts, the Fed will probably continue to fight that narrative.

“They’ve run a long race, and they won’t quit just because the finish line appears to be a little closer,” Larkin noted.

To Chris Zaccarelli at Independent Advisor Alliance, whether or not the economy can stay out of recession remains to be seen, but the market should continue to rally as investors begin to accept the view that higher rates are off the table.

The drop in inflation suggests that recent monetary policy has been doing its job, which makes the prospect of a “soft landing” ever more likely, according to Richard Flynn at Charles Schwab UK. The news reinforces the probability that officials will “hold off” from further rate hikes, he noted.

“With the US economy holding up, the inflation data are ‘soft-landing nirvana’ for the equity markets,” said Neil Dutta, head of economics at Renaissance Macro Research.

An intact disinflationary process means that the Fed can “sit tight for now” — which would lower the risk of an “overly restrictive policy”, according to Lauren Goodwin at New York Life Investments. Still, she cautions investors who are getting “too enthusiastic” as “financial conditions are now easing again, which keeps the Fed on guard and highly data dependent.”

The Fed’s challenge is that the market tries to jump to the “endgame” — risking a larger or sooner easing in financial conditions than the Fed itself would like to see, said Krishna Guha at Evercore ISI. “So expect Fed officials to maintain a very cautious and relatively hawkish tone.”

Citadel founder Ken Griffin said the Fed risks a hit to its reputation if it cuts interest rates too quickly. Cathie Wood, the head of ARK Investment Management, said that deflation is already underway in the US across industries and will force the central bank to kick off a big interest-rate cutting cycle.

Fed officials welcomed the latest data showing receding US inflation, while adding that there’s still a way to go before it reaches the central bank’s 2 per cent target.

“Our base case remains that the Fed will not raise rates further,” said Brian Rose at UBS Global Wealth Management. “However, inflation is still too high and the labor market still too tight for the Fed to declare victory and announce an end to the rate-hiking cycle.”

In Rose’s view, such an announcement is likely to be at least three months away unless the data takes a sudden turn toward the weaker side. Once an announcement is made, markets may quickly focus on the timing of the first rate cut, leading to lower bond yields and a weaker US dollar, he noted.

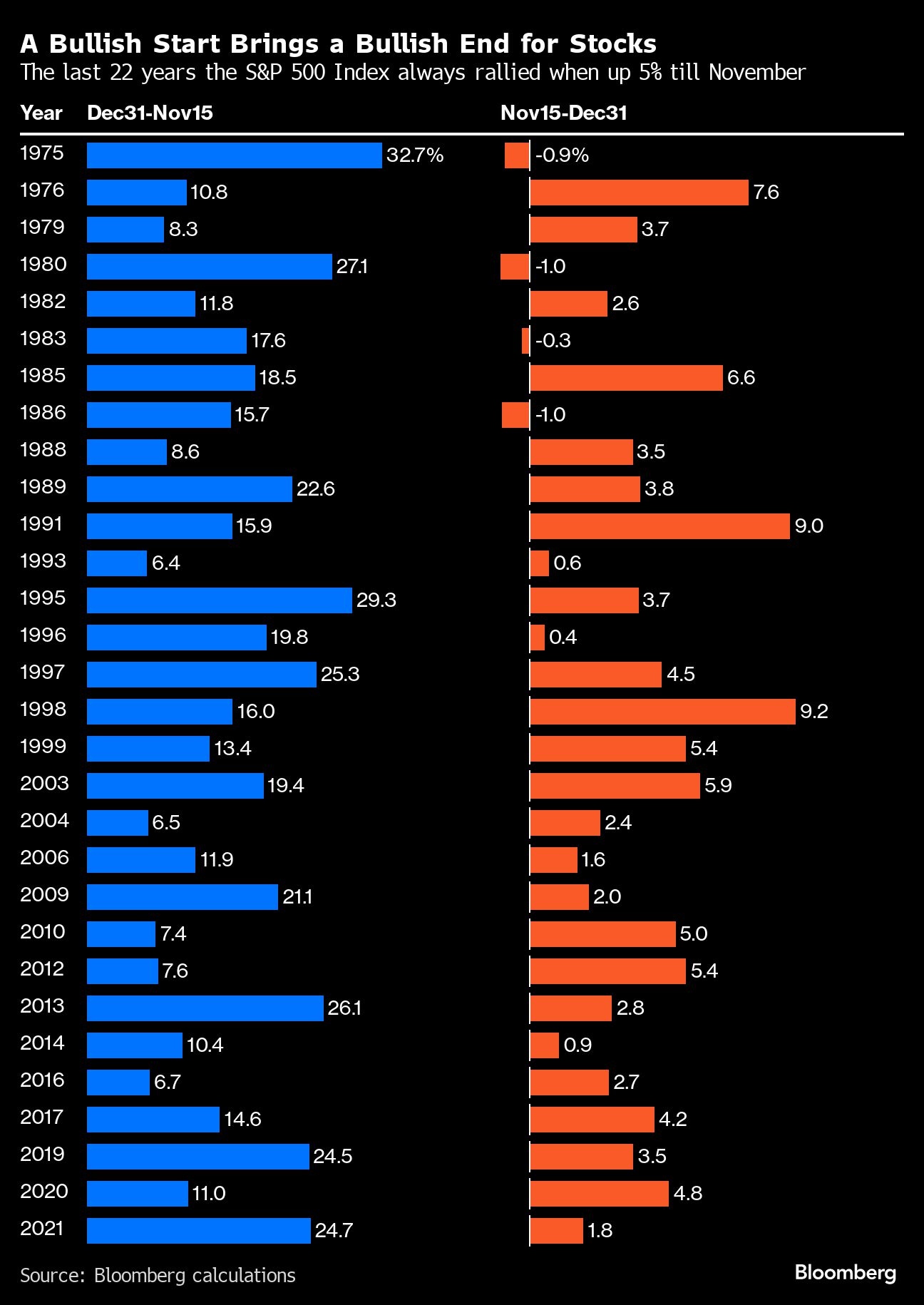

Equities have rallied in November on bets the Fed is done with rate hikes, with the S&P 500 up more than 7 per cent in the span — and heading toward its best month since October 2022.

In the past 22 years, when the S&P 500 was up 5 per cent or more by mid-November, the remainder of that year was positive every single time, according to data compiled by Bloomberg. Go back 50 years, and that setup was positive 26 out of 30 times, with the decline in the four exceptions being 1 per cent or less.

Meantime, investors turned the most bullish on bonds since the global financial crisis amid “big conviction” that rates will move lower in 2024, according to the latest Bank of America Corp. fund manager survey. The poll showed investors were dumping cash to hold the biggest overweight position in bonds since 2009.

Pacific Investment Management Co. — among the many whose expectations for a rally this year were disappointed — is renewing the call for 2024.

Bonds “have rarely been as attractive as they appear today” relative to stocks, Pimco managers Erin Browne, Geraldine Sundstrom and Emmanuel Sharef said in a report predicting “prime time” for the asset class in 2024.

Corporate Highlights:

- Home Depot Inc. narrowed its guidance for a decline in this year’s profit and revenue as home-improvement demand wanes.

- Boeing Co. extended its successful order haul on the second day of the Dubai Air Show, winning a deal from Ethiopian Airlines for more narrow- and widebody aircraft while rival Airbus SE continued to chase an increasingly elusive deal with Emirates.

- Alphabet Inc.’s Google gives Apple Inc. a 36 per cent share of the revenue earned via advertising from searches in the Safari browser to be the default search engine on Macs, iPhones and iPads, chief executive officer Sundar Pichai confirmed.

- Glencore Plc will buy a majority stake in Teck Resources Ltd.’s coal business, ending a months-long saga that transfixed the mining industry and setting the stage for the commodity giant to exit the coal business itself.

- Siemens Energy AG has secured a €15 billion (US$16.2 billion) deal with the German government, its biggest shareholder Siemens AG and a consortium of banks, as the troubled manufacturer weathers massive losses at its wind-turbine unit.

Key events this week:

- China retail sales, industrial production, fixed-asset investment, Wednesday

- Japan GDP, industrial production, Wednesday

- UK CPI, Wednesday

- U.S. retail sales, business inventories, PPI, Empire manufacturing, Wednesday

- Target earnings, Wednesday

- China new home prices, Thursday

- U.S. initial jobless claims, industrial production, Thursday

- Walmart earnings, Thursday

- U.S. President Joe Biden and Chinese President Xi Jinping expected to speak at APEC leaders summit, Thursday

- Cleveland Fed President Loretta Mester, New York Fed President John Williams and Fed vice chair for supervision Michael Barr speak, Thursday

- Bank of England deputy governor Dave Ramsden and ECB President Christine Lagarde speak at event, Thursday

- U.S. housing starts, Friday

- U.S. Congress faces a midnight deadline to pass a federal spending measure, Friday

- ECB President Christine Lagarde speaks, Friday

- Chicago Fed President Austan Goolsbee, Boston Fed President Susan Collins and San Francisco Fed President Mary Daly speak, Friday

Some of the main moves in markets:

Stocks

- The S&P 500 rose 1.9 per cent as of 4 p.m. New York time

- The Nasdaq 100 rose 2.1 per cent

- The Dow Jones Industrial Average rose 1.4 per cent

- The MSCI World index rose 2 per cent

Currencies

- The Bloomberg Dollar Spot Index fell 1.2 per cent

- The euro rose 1.7 per cent to $1.0882

- The British pound rose 1.8 per cent to $1.2501

- The Japanese yen rose 1 per cent to 150.25 per dollar

Cryptocurrencies

- Bitcoin fell 3.3 per cent to $35,274.04

- Ether fell 4.1 per cent to $1,975.61

Bonds

- The yield on 10-year Treasuries declined 20 basis points to 4.44 per cent

- Germany’s 10-year yield declined 11 basis points to 2.60 per cent

- Britain’s 10-year yield declined 16 basis points to 4.15 per cent

Commodities

- West Texas Intermediate crude was little changed

- Spot gold rose 0.9 per cent to $1,963.56 an ounce