Feb 2, 2024

Markets today: U.S. stock bull run powers ahead as U.S. economy roars

, Bloomberg News

Markets with heavy tech focus

VIDEO SIGN OUT

The stock market extended this week’s gains as big tech rallied and a solid jobs report bolstered the outlook for corporate profits.

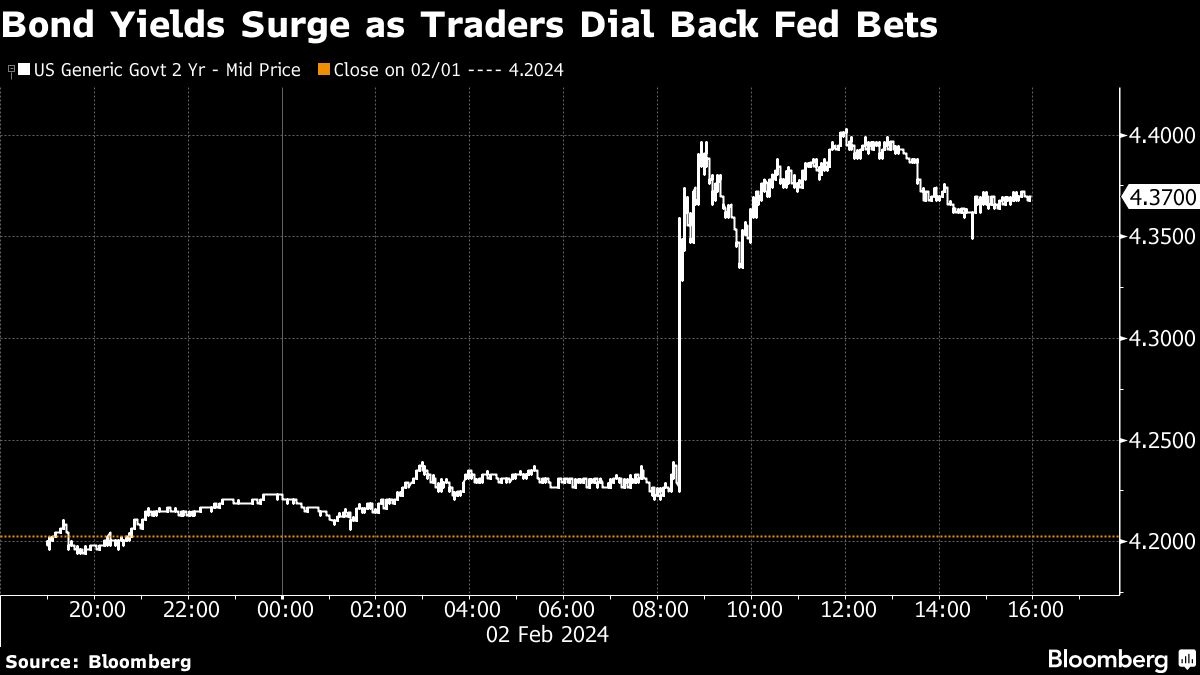

Equities hit all-time highs, with the S&P 500 approaching 5,000 and the Nasdaq 100 up about 2 per cent on bullish outlooks from Meta Platforms Inc. and Amazon.com Inc. Economic optimism outweighed bets the Federal Reserve will be in no rush to cut rates. Treasury two-year yields jumped 17 basis points to 4.37 per cent. The dollar rose to levels last seen before the Fed’s December “pivot.”

“Today’s jobs report calls into question the narrative of a ‘soft landing’,” said David Donabedian at CIBC Private Wealth U.S. “The January jobs report was pretty dramatic, implying there may be ‘no landing.’ The economy is ripping ahead.”

To Neil Dutta at Renaissance Macro Research, strong growth in labor productivity means unit labor costs are under control — which is a good backdrop for company earnings. “It’s hard to get too bearish” with such economic resilience, said Bret Kenwell at eToro. Larry Tentarelli at Blue Chip Daily Trend Report sees the data as “a very bullish sign for the economy” — adding that “we are buyers on any short-term weakness in stocks.”

“Just as many were caught off guard by the recession that never appeared in 2023, there’s always the possibility that another year will go by without a recession,” said Chris Zaccarelli at Independent Advisor Alliance.

Nonfarm payrolls surged 353,000 last month following upward revisions to the prior two months. The unemployment rate held at 3.7 per cent. Hourly wages accelerated from a month earlier, increasing by the most since March 2022. Separate data showed U.S. consumer sentiment increased sharply.

While signs of a strong economy may continue to bode well for Corporate America, the data just reinforce the view that the Fed will delay the start of its rate cuts.

“Well, I think we can officially kiss a March rate cut goodbye, and more than likely a May,” said Alex McGrath at NorthEnd Private Wealth.

Indeed, Treasury yields soared after Friday’s data strengthened the case for the Fed to defer cutting rates until at least the second quarter.

Swap contracts referencing the March Fed meeting date cut the odds of a quarter-point rate cut in half, to about 15 per cent — while the May contract no longer fully priced in a cut, which it had for more than a month.

“A March rate cut now appears increasingly unlikely,” said Jason Pride at Glenmede. “The more likely trajectory is two-three cuts this year beginning around summer.”

Seema Shah at Principal Asset Management says that it wasn’t just a strong January for the labor market. It turns out that previous months were stronger than initially believed.

“The dramatic upside surprise to both jobs and wage growth means that a March rate cut must be off the table now, and a May cut is also now potentially on ice,” she noted.

Following Wednesday’s Fed decision, Powell said that a cut is unlikely to come at the next gathering in March, which some market participants had been betting on. The Fed chief will appear on CBS News’s 60 Minutes this Sunday to discuss inflation risks, expected rate cuts and the banking system, among other topics, the network said.

His direct pushback on the Fed being ready to cut rates in March now looks particularly “well timed,” according to Tiffany Wilding at Pacific Investment Management Co.

To Richard Flynn at Charles Schwab, Friday’s figures may be another factor delaying the Fed’s first rate cut closer to summer, but if the economy maintains its comfortable trajectory, that might not be a bad thing.

“What’s the hurry?” he asks.

The strong market gains remain at nearly unprecedented levels — with shifting expectations on the Fed outlook “unable to crack the momentum,” said Mark Hackett at Nationwide.

“Investors remaining on the sidelines are beginning to capitulate, which when paired with the return of share repurchases following earnings season, should act as a tailwind for markets,” Hackett noted.

Equities powered ahead Friday, led by a rally in megacaps that have led the market surge from the bottom. Meta, which dazzled shareholders with yet another impressive quarterly earnings report soared more than 20 per cent to a record.

For all the hype over artificial intelligence and its potential to bolster profits, Meta and Amazon stood out as winners of the big-tech earnings season for the simple reason that they have cut tens of thousands of jobs, and their core businesses did well over the holidays. That allowed Meta to announce plans for an additional US$50 billion in stock buybacks and its first quarterly dividend, giving investors a reason to stick around.

The rush into technology stocks is resembling the dot-com era, reflecting an assumption that the economy will perform strongly despite tighter monetary policy, according to Bank of America Corp.’s Michael Hartnett.

He notes that 75 per cent of investors expect a soft landing and 20 per cent a no-landing scenario. Yet, while a soft landing should support a broader range of equities, the so-called Magnificent Seven accounted for 45 per cent of the S&P 500’s return in January, reflecting a “leaning toward no landing/bubble,” he said.

In other corporate news, Apple Inc. rebounded from its session lows as investors looked past a deepening slump in its China business. Exxon Mobil Corp. and Chevron Corp. surpassed earnings forecasts as bigger-than-expected oil output from shale fields helped cushion the blow from weakening crude prices. A gauge of regional banks rebounded after a two-day slide.

Some of the main moves in markets:

Stocks

- The S&P 500 rose 1.1 per cent as of 4 p.m. New York time

- The Nasdaq 100 rose 1.7 per cent

- The Dow Jones Industrial Average rose 0.3 per cent

- The MSCI World index rose 0.6 per cent

Currencies

- The Bloomberg Dollar Spot Index rose 0.6 per cent

- The euro fell 0.7 per cent to $1.0793

- The British pound fell 0.8 per cent to $1.2637

- The Japanese yen fell 1.3 per cent to 148.30 per dollar

Cryptocurrencies

- Bitcoin fell 0.3 per cent to $42,945.79

- Ether fell 0.3 per cent to $2,297.85

Bonds

- The yield on 10-year Treasuries advanced 14 basis points to 4.02 per cent

- Germany’s 10-year yield advanced nine basis points to 2.24 per cent

- Britain’s 10-year yield advanced 17 basis points to 3.92 per cent

Commodities

- West Texas Intermediate crude fell 2.3 per cent to $72.14 a barrel

- Spot gold fell 0.9 per cent to $2,036.72 an ounce