Nov 17, 2023

Markets today: 'epic' stock rally fades amid signs of overheating

, Bloomberg News

Buying opportunity in dividend stocks

VIDEO SIGN OUT

U.S. stocks saw small moves after a $2.7 trillion rally in November that was fueled by bets the Federal Reserve will end its hiking cycle to prevent a recession. The dollar erased its 2023 advance.

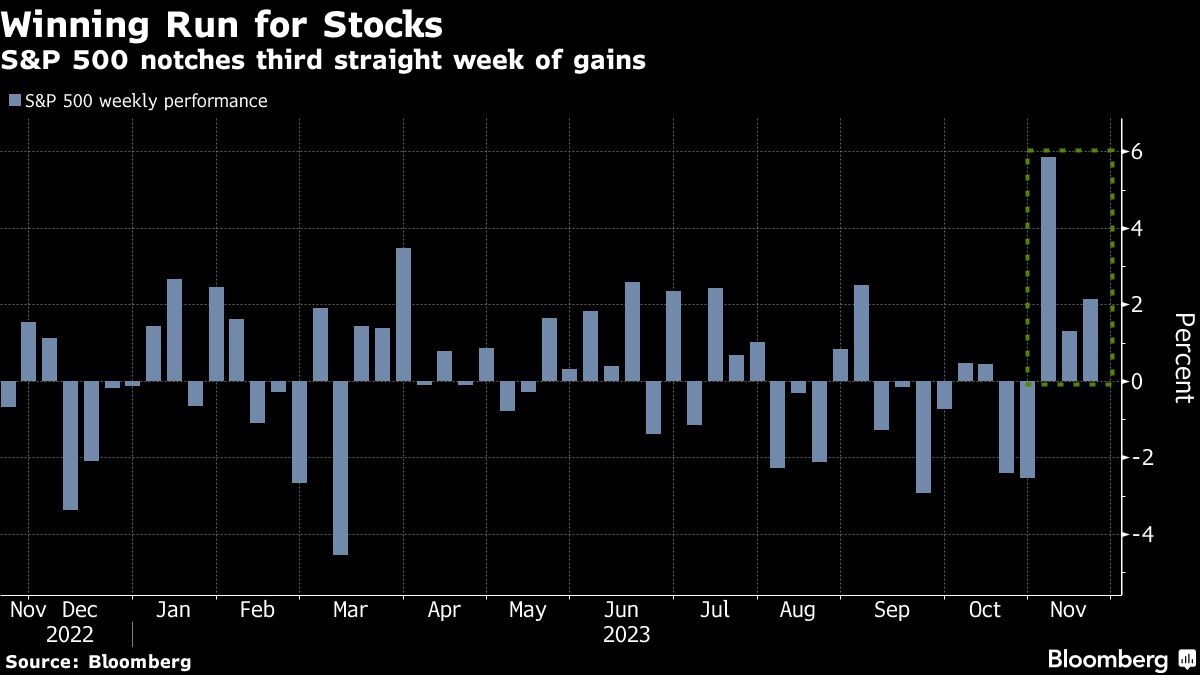

The S&P 500 traded above 4,500, notching its third straight week of gains — the longest run since July. Piles of derivatives contracts tied to stocks and indexes matured — which typically amplifies instability. Applied Materials Inc. sank on a report it faces a U.S. criminal probe for allegedly violating export restrictions to China. Homebuilders rose as new home construction picked up.

Equities have made a rapid about-face to “overbought” from “oversold” levels — spurring calls they were due for a breather. Global stock funds attracted $23.5 billion in the week through Nov. 15, the second-biggest inflows of the year, Bank of America Corp. noted, citing data from EPFR.

After an “epic risk rally,” investors should offload those assets as technical and macroeconomic headwinds are building, according to Michael Hartnett, chief investment strategist at BofA. “Fade it,” he noted.

The dollar saw its worst week in four months amid bets the currency has already peaked, with softer-than-expected economic data reinforcing bets the Fed is done with rate hikes. Ten-year U.S. yields were little changed. Oil climbed, but posted its fourth straight weekly drop on supply pressures.

Following a softer-than-expected inflation report, the Bloomberg U.S. Aggregate index has gained 1.2 per cent this week through Thursday and is up 0.4 per cent for the year. The benchmark, which tracks $25 trillion of investment-grade government and corporate debt, posted a record loss of 13 per cent in 2022 and declined 1.5 per cent the previous year. The index has never slid three straight years.

Franklin Templeton’s Sonal Desai said this week’s bond-market rally has gone too far, too fast. “Markets are priced for beyond the perfect landing,” she told Bloomberg Television. “There do remain risks to inflation and there isn’t enough data to support the rate cuts priced for next year.”

Traders also kept a close eye on the latest Fedspeak. Fed Vice Chair for Supervision Michael Barr reiterated officials are likely at or near the end of their tightening campaign. Yet Fed Bank of San Francisco President Mary Daly said policymakers aren’t certain inflation is on a path to their 2 per cent target.

“While it is unlikely the Fed will raise rates, investors are jumping ahead too quickly embracing rate cuts,” said David Donabedian, chief investment officer of CIBC Private Wealth U.S.. “Some time in 2024, the Fed will start to lower rates. But we are in a waiting game.”

After the recent rally, the S&P 500 has been consolidating in a tight range, with the gauge having “bandwidth” to pull back further over the short run — without breaking the initial support at 4,350-4,400, said Dan Wantrobski at Janney Montgomery Scott.

Meantime, valuations of high-quality stocks — those with high profitability and low leverage — have become significantly more expensive compared to both the overall market and their low-quality counterparts, an analysis by Bloomberg Intelligence found.

The other times in the recent past when quality commanded such high valuation premiums were in 2020 and 2008-2009, both times of turmoil. These periods pushed people to seek safety in high-quality investments, leading to the valuation spikes.

“Quality stocks have historically outperformed in the late stages of the business cycle, including in periods of economic contraction, which should offer portfolio protection if the economy slows more than we expect,” said Solita Marcelli, chief investment officer for the Americas at UBS Global Wealth Management.

As earnings season draws to a close, so does the S&P 500’s profit recession. Earnings are up 4 per cent year-over-year with over 90 per cent of S&P 500 firms having reported results for the third quarter, meaning a three-quarter streak of earnings declines is likely done, data compiled by BI show.

Traders are gearing up for a few more earnings from retailers and tech companies next week.

Best Buy Co., Nordstrom Inc. and Lowe’s Cos. are set to post slumping sales, while Nvidia Corp.’s quarterly results could still exceed sky-high investor expectations thanks to strong demand for generative artificial intelligence.

Corporate Highlights:

- Sam Altman, one of the most prominent figures in the world of artificial intelligence, is leaving OpenAI with the company’s board saying he wasn’t always “candid” and that it had lost confidence in him as a leader.

- Amazon.com Inc. is cutting hundreds of employees in the division responsible for its voice-activated Alexa assistant, according to a memo sent to employees.

- ChargePoint Holdings Inc. announced the sudden resignation of its longtime chief executive officer while posting disappointing quarterly revenue.

- Gap Inc. reported profit that exceeded forecasts and a smaller-than-expected drop in comparable sales.

- Ross Stores Inc., a discount department store chain, reported comparable sales that beat estimates.

- Moody’s Investors Service on Thursday lowered its outlook for Tyson Foods Inc. as it expects the largest U.S. meat producer to keep burning cash in the coming 12 to 18 months.

- Elon Musk’s SpaceX is poised to launch its deep-space Starship rocket system Saturday from South Texas for the second time ever.

Some of the main moves in markets:

Stocks

- The S&P 500 rose 0.1 per cent as of 4 p.m. New York time

- The Nasdaq 100 was little changed

- The Dow Jones Industrial Average was little changed

- The MSCI World index rose 0.3 per cent

Currencies

- The Bloomberg Dollar Spot Index fell 0.4 per cent

- The euro rose 0.5 per cent to $1.0908

- The British pound rose 0.4 per cent to $1.2460

- The Japanese yen rose 0.7 per cent to 149.69 per dollar

Cryptocurrencies

- Bitcoin rose 1.5 per cent to $36,503.45

- Ether fell 0.6 per cent to $1,943.44

Bonds

- The yield on 10-year Treasuries was little changed at 4.44 per cent

- Germany’s 10-year yield was little changed at 2.59 per cent

- Britain’s 10-year yield declined five basis points to 4.10 per cent

Commodities

- West Texas Intermediate crude rose 3.9 per cent to $75.75 a barrel

- Spot gold was little changed