Global Housing Shortages Are Crushing Immigration-Fueled Growth

Households go backwards in 13 developed economies as record immigration runs into a housing crisis.

Latest Videos

The information you requested is not available at this time, please check back again soon.

Households go backwards in 13 developed economies as record immigration runs into a housing crisis.

Australia’s central bank will likely keep its key interest rate at a 12-year high and stick with it for much of the year to restrain inflationary pressures underpinned by a surprisingly tight job market.

Bond traders welcomed their first clear sign of a cooling US labor market, but it’s only a part of what’s needed to fire up the truly sweeping rally they’ve been hoping for all year.

It’s an oft-told anecdote littering social media: Those who invested early in cryptocurrencies have enjoyed life-changing wealth.

Australia’s housing rental value hit a fresh record in April with some cities seeing renewed growth momentum, a troubling sign for the Reserve Bank that’s likely to leave borrowing costs at a 12-year high this week to stave off price pressures.

Dec 10, 2019

, Bloomberg News

In a world reliant on smartphone apps, bank branches may no longer be Main Street mainstays, with red velvet ropes between brass stanchions herding customers to tellers behind wickets.

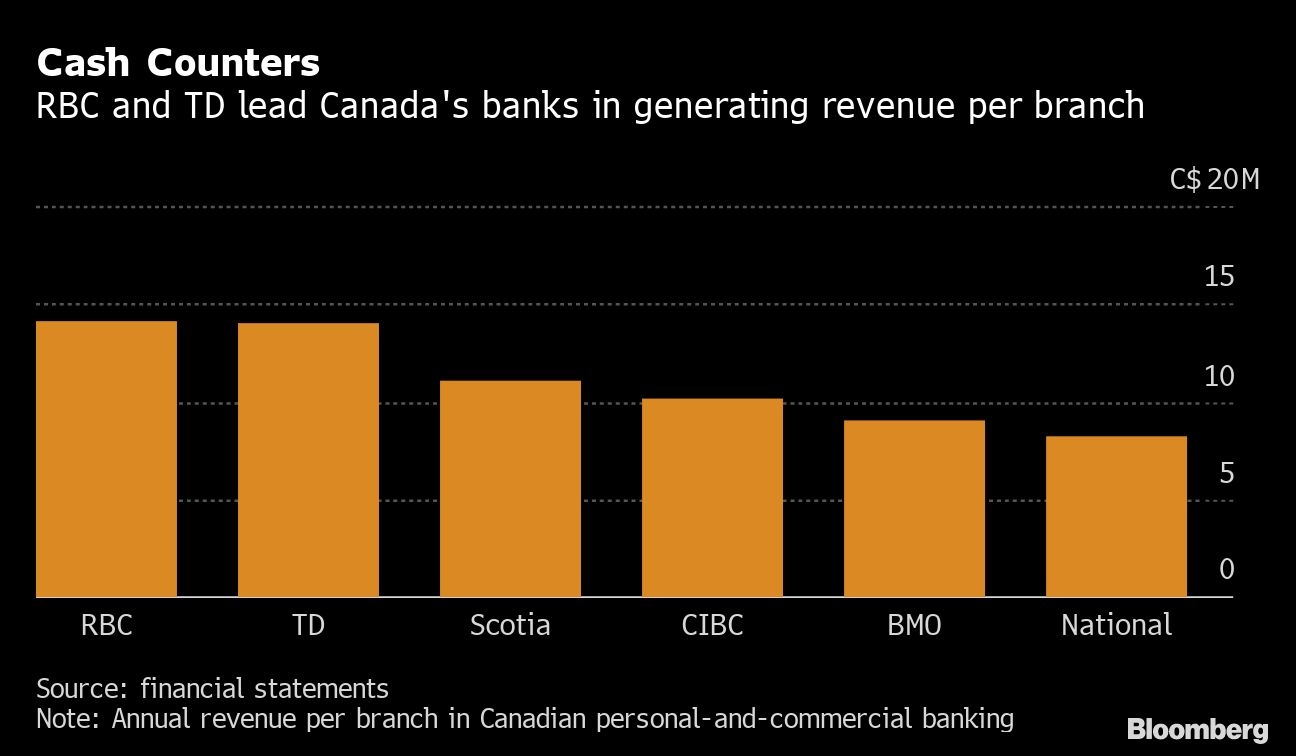

But they’re still an important part of banking and, in Canada, the two largest lenders are beating their smaller rivals at drawing more and more revenue from physical locations. Royal Bank of Canada and Toronto-Dominion Bank earn $14 million a year from each of their domestic branches, distancing themselves from smaller competitors in the process.

Bank branches are evolving as customers increasingly rely on mobile phones, websites and automated teller machines for routine transactions, with the drudgery of standing in line to cash a paycheck or shift money between accounts largely left to a bygone era.

Canada’s banks have reacted accordingly, shrinking branch sizes, adopting the newest technology and turning once counter-bound tellers into roaming advisers armed with tablets to sell high-margin products and mortgages. That’s paying off: All of the big Canadian banks have posted increases in annual revenue per branch in each of the past three years, and sales have soared substantially from a decade ago.

“We’re growing our investment in innovative formats: university campuses, hospitals, newcomer centers, which is helping us grow our client base,” Royal Bank Chief Financial Officer Rod Bolger said in a phone interview. “As we have ramped up our leading digital and mobile applications, customers and clients still like to come to branches for advice.”

Royal Bank is Canada’s leader, with 1,201 branches across the country -- four more than a decade ago, even with the addition of digital-banking options during that period. Annual revenue per branch has soared 70 per cent since 2009. Technology has allowed branch employees to focus on dispensing advice to customers rather than merely handling routine transactions, according to Bolger.

“We continue to free up time for our banking advisers,” he said. “That is helping us to continue to expand our market share, which will then in turn result in higher productivity per branch.”

Rival Toronto-Dominion, meanwhile, has 1,091 branches nationwide, slightly fewer than a decade ago. Like Royal Bank, it has seen a surge in per-branch revenue, with a 66 per cent increase since 2009. The ratio for each of bank was calculated by dividing annual revenue from Canadian personal-and-commercial banking by the number of domestic branches at the end of each fiscal year.

“People have been speculating about the future of branches, but we’ve been very clear in our strategy that branches are important to us -- they’re an important contact point for customers who need human advice and human touch,” Toronto-Dominion CFO Riaz Ahmed said. “We continue to see them as a very important part of our strategy.”

Canadian Imperial Bank of Commerce brings in an average of $10 million in yearly sales, up about 53 per cent from a decade ago, for each of its 1,024 branches.

Customer Conversations

“We continue to improve our advisory capabilities and focus on having conversations with clients to understand their needs and to provide them with products and services that they need,” said CIBC CFO Hratch Panossian. “That has had some positive momentum.”

Canada’s six largest banks operate 5,578 branches domestically, 2.9 per cent fewer than a decade ago. While the decline isn’t as dramatic as was once predicted by those who thought ATMs and mobile banking would spell an end to bricks-and-mortar locations, branches also aren’t keeping pace with population growth.

Canada had 20 branches for every 100,000 adults as of 2018, down from about 25 before the 2008 financial crisis, according to the World Bank. The U.S., in comparison, had about 31 branches per 100,000 adults, down from 35.

Bank of Nova Scotia reduced its domestic network the most, trimming 6.9 per cent of its branches from a decade ago, to 949 today. Those branches generate an average of $11 million in annual revenue, an amount that has climbed steadily in the past six years.

“Scotiabank has been adding adviser roles to branches,” spokesman Clancy Zeifman said in an email. “We have also been investing in technologies and tools to help our employees be more productive, including removing manual processes so they can spend more time focusing on our customers.”

While branches remain important for Bank of Montreal, CFO Tom Flynn said he expects a gradual decline in both the number of branches and average size amid a push toward digital banking. Canada’s fourth-largest lender has 891 domestic locations, which generate about $9 million in annual sales on average, a 55 per cent jump from 2009.

Smaller Branches

“We want to be close to people when they’re doing transactions that are bigger and really important to them,” Flynn said. “At the same time, total branch traffic is down, given the digital migration, and in response to that we have been and will continue to take the average square footage of our branch network down.”

National Bank of Canada has the lowest annual revenue per branch, at $8.2 million for each of its 422 locations, though that’s still 60 per cent higher than a decade ago. The Montreal-based lender, the smallest among Canada’s Big Six banks, may lag behind its larger rivals partly because of its regional focus.

“We are located in the province of Quebec, where people are less in debt -- they borrow less,” Jean Dagenais, senior vice president of finance, said in an interview. With property values lower than in other parts of Canada and mortgages smaller as a result, “the volume of loans per branch is lower than a big bank in the Toronto area.”

Related

wind farm, operated by EDF Energy Renewables Ltd., off the Northumberland coast in Blyth, U.K., on Friday, June 22, 2018. Electricite de France SA Chief Executive Officer Jean-Bernard Levy said it’s too risky to invest in large wind power projects without subsidies because swings in electricity prices would endanger returns for developers and their shareholders. , Bloomberg")