Oct 2, 2017

Joe Mazumdar's Top Picks: October 2, 2017

BNN Bloomberg

Joe Mazumdar, co-editor and analyst at Exploration Insights

FOCUS: Junior mining sector

_______________________________________________________________

MARKET OUTLOOK

Since late 2015, we saw a progression of M&A transactions where mid-tier precious metal producers acquired junior producers, including Silver Standard (now SSR Mining) and Claude Resources, Tahoe Resources and Lakeshore Gold, Kirkland and Newmarket. As the year progressed, we saw more M&A activity directed at developing projects such as Nevsun and Reservoir, Goldcorp and Kaminak, among others. At the time, we came to appreciate the fact that quality deposits, especially in the gold sector, were getting rarer.

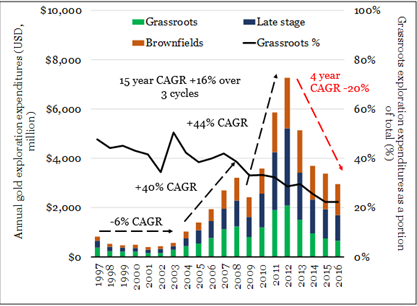

The trends in exploration expenditure suggests 20 per cent per year drops from a peak in 2012 to 2015. Also, we note that the proportion of grassroots exploration has been declining since 2003. Exploration as a proportion of revenue for some major producers has been dropping since 2003 to two to four per cent, roughly the equivalent to what is spent on G&A. With the backdrop of declining reserves, due in part to lower reserve prices, producers need to find higher-quality projects.

As a result, we have observed more strategic investments and joint ventures with exploration companies as a proxy for their exploration budgets. At major conferences, we have also seen an uptick of the attendees from corporate development. Therefore, our focus has been on exploration companies and prospect generators with the following attributes:

- Exploring for gold, copper and zinc

- Large-district scale land packages

- Mining friendly jurisdictions

- Potential for a high margin deposit

- Highly qualified management team with relevant experience (deposit, jurisdiction)

- Well-funded for some important catalysts

These tend to be very high risk and high reward opportunities. The sizeable returns to grassroots exploration companies (14) exploring for gold, copper and zinc in predominantly stable jurisdictions over the past year that have averaged around 260 per cent (up to 680 per cent) over an average of two months are the attraction. We have harvested some of our investments and our closed positions in 2017 have provided us around 180 per cent return on average within a wide range of down 60 per cent to up 700 per cent.

TOP PICKS

MIRASOL RESOURCES (MRZ.V)

We consider Mirasol to be the premier prospect generator as it is currently harvesting several years of project generation in a favorable environment, where major producers are lacking significant project pipelines. The company provides exposure to gold, silver and copper, with assets in Chile and Argentina in varying environments that are guided by an excellent technical team. It is well-funded and has joint ventures with Yamana Gold and OceanaGold.

TINKA RESOURCES (TK.V)

Tinka is led by a quality management team with a number of years of experience exploring for zinc projects in Peru with major companies. We know from our reviews that quality zinc projects are not legion. We think that the potential tonnage (30 million tonnes) at grades of over 7 per cent zinc at the Ayawilca project in Peru should be an attractive target for a potential suitor. Along with more drilling results, the next significant catalyst is the revised resource estimate at Ayawilca due at the end of October to early November.

ALMADEX MINERALS (AMZ.V)

Almadex is a grassroots explorer that was spun out of Almaden Minerals (AMM.TO) last year to focus on copper and precious metal projects in Mexico, where they have ~30 years of experience. Its current focus is on the El Cobre copper project in the state of Veracruz. The project’s location at low elevations and proximity to infrastructure adds to its appeal. Furthermore, the Agnico Eagle private placement to gain exposure to the Caballo Blanco project, only 8-10 kilometres to the northeast of El Cobre, supports the idea that some majors are comfortable with operating in the State of Veracruz. The company has some downside protection with its working capital position and royalty portfolio.

| DISCLOSURE | PERSONAL | FAMILY | PORTFOLIO/FUND |

|---|---|---|---|

| MRZ | Y | N | N |

| TK | Y | N | N |

| AMZ | Y | N | N |

PAST PICKS: MARCH 8, 2017

MIRASOL RESOURCES (MRZ.V)

- Then: $1.87

- Now: $1.63

- Return: -12.83%

- Total return: -12.83%

NIGHTHAWK GOLD (NHK.TO) – Sold

Buy price – $0.46

Sell/reduce price – $0.85

Recent drilling has failed to intersect the same high-grade shoots of gold mineralization that attracted us to the Colomac Gold project initially. The land package at Indin Lake is significant and other exploration targets remain. The company is well-funded for the next two years of exploration but the valuation suggests that the risk to reward ratio is not favorable.

- Then: $0.87

- Now: $0.75

- Return: -13.79%

- Total return: -13.79%

Cordoba Minerals (CDB.V) – Sale pending

Buy price – $0.82

Sell/reduce price – $0.75 (limit price have not hit it yet)

A transaction that involved re-purchasing a portion of the project from a Robert Friedland-led private exploration company, HPX, was not favorable for shareholders. We think, therefore, that we placed a sale at a limit price of $0.75. The company is currently drilling but will have to fund itself to advance the project rather than having HPX carry them to a feasibility study.

- Then: $1.19

- Now: $0.55

- Return: -53.78%

- Total return: -53.78%

TOTAL RETURN AVERAGE: -26.80%

| DISCLOSURE | PERSONAL | FAMILY | PORTFOLIO/FUND |

|---|---|---|---|

| MRZ | Y | N | Y |

| NHK | Y | N | Y |

| CDB | Y | N | Y |

WEBSITE: www.explorationinsights.com