May 6, 2019

Larry Berman: How much risk should your financial plan take on?

By Larry Berman

Larry Berman: How much risk should your financial plan take on?

VIDEO SIGN OUT

FP Canada, formerly the Financial Planning Standards Council, has come out with their new long-term assumptions for financial planners. For most people, having an independent financial plan completed that is free of sales pressures should be essential. For those capable of doing their own forecasting, the FP Canada’s annual assumptions are a good starting place.

For most people, an assumption of how long you’re going to need your money to last (and therefore how much you need to save is important). Sadly, I see a catastrophic financial conclusion for many that do not save enough. My parents were in this situation when they retired. My father was employed in a warehouse and worked very hard every day until he was put on long-term disability around the age of 55 when I was a teenager. My mother could never hold down a job due to her mental health challenges (bipolar schizophrenia). They had no savings at all beyond CPP, OAS and GIS and a very modest work pension (about $700 per month) that mostly do not exist anymore due to the shift to defined contribution plans. What made it worse was that they separated once I left the nest to get married. Late-life divorce can place a huge financial burden on retirement.

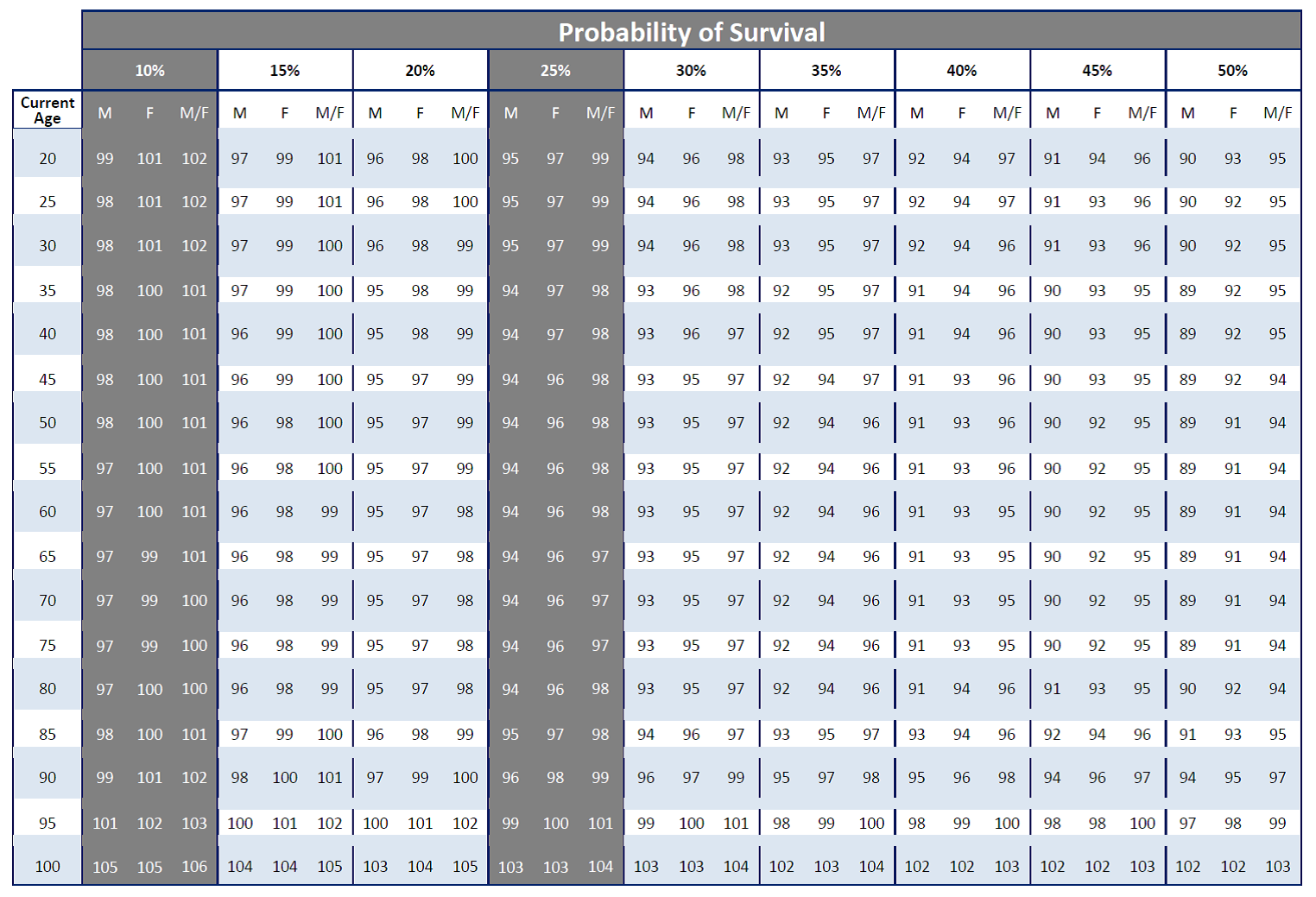

Most should start the exercise of creating a financial plan with some basic assumptions. The first should be how long you will need your money to last. According to recent Statistics Canada data, the average Canadian is almost 41 years old. According to the actuarial tables below, the average married couple has a 50-per-cent chance of one spouse living to 95 years old. In other words, your savings need to last about 30 years in the traditional retirement scenario.

Once you have established how long you are likely going to need your savings, how much you should be saving and the return you will need on your portfolio so that your standard of living does not change in your retirement years, the rest is mostly a mathematical exercise. Financial planners can help you with minimizing taxes (and thereby maximizing your after-tax returns) and planning for your future lifestyle. I’ve said many times that having a regular financial plan update with an experienced planner is one of the best investments you can make. It’s not just about lowering fees. It’s about building a sleep-at-night portfolio to reduce your financial anxiety levels.

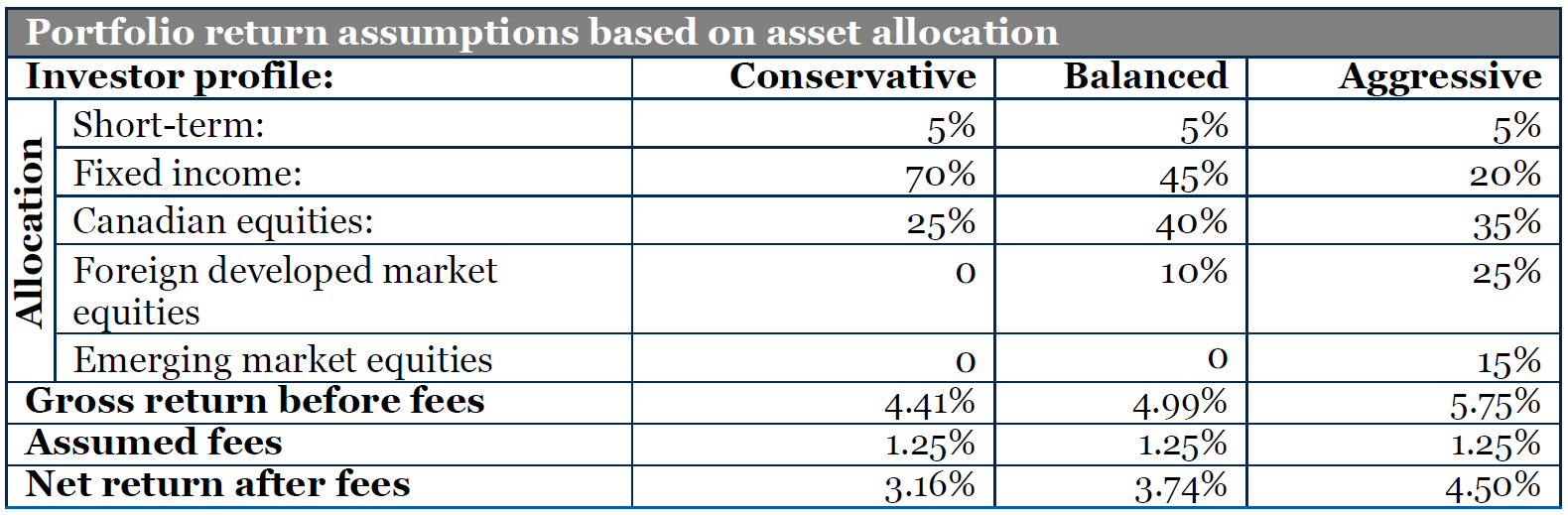

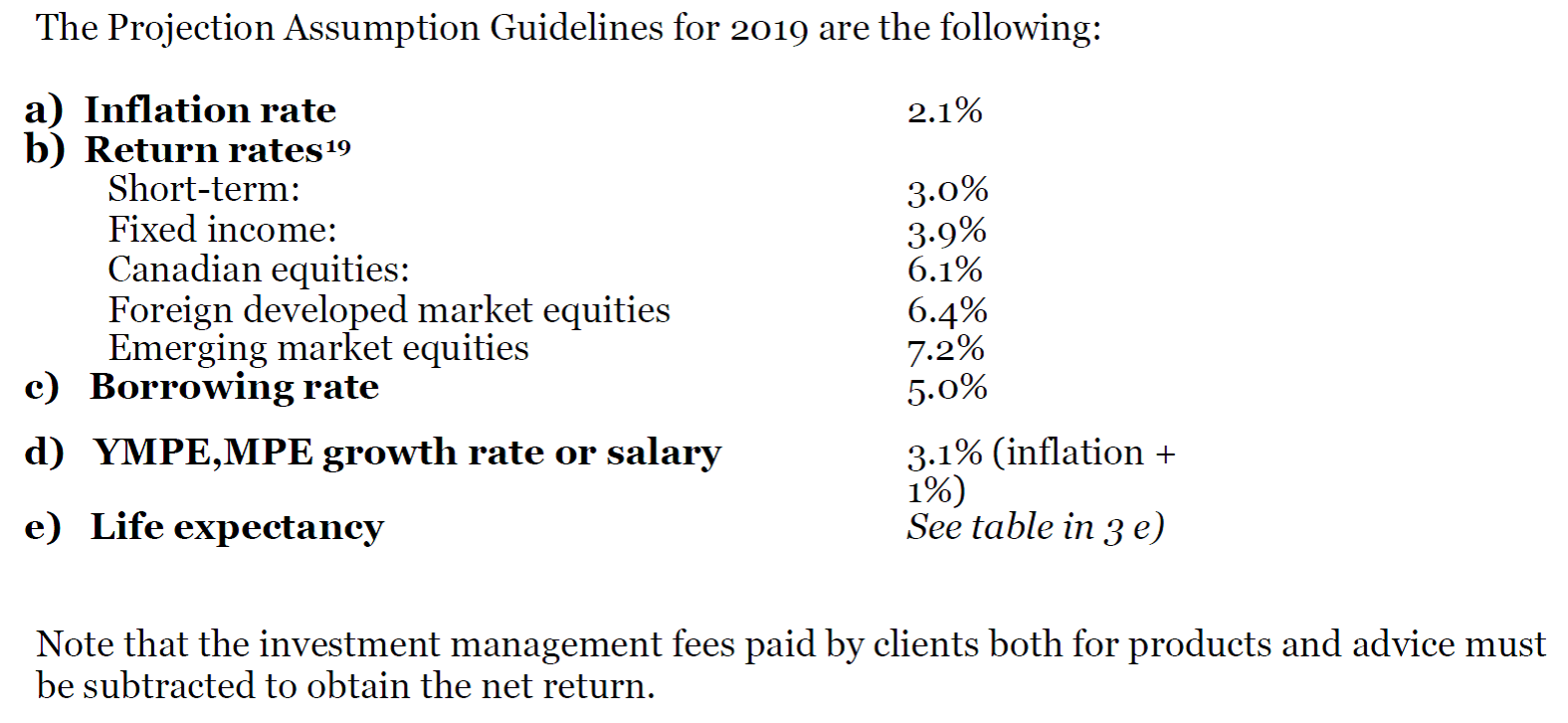

In their report, FP Canada forecast the long-term returns as a guideline for planners to use as assumptions in portfolios. Those numbers have been declining over the past decade due to rising equity markets and falling interest rates. We are much closer to a high point for the cycle and the forecast numbers are low.

How do you calculate the right numbers for you? I do think they are a bit higher than what the average investor will experience over the next decade or so. I wholeheartedly disagree with FP Canada’s guidelines on what should be in a Conservative, Balanced, and Aggressive portfolio in terms of asset mix. Canada will most likely underperform the rest of the world in terms of average returns because we have less technology, consumer and health care stock exposure in our indexes. This most certainly are the biggest growth areas for decades as society ages rapidly.

Assumptions for returns are based on an equal weight of the QPP and CPP assumptions along with a survey of financial services companies and data from StatsCanada. As you can see, even with an aggressive risk allocation, average returns will barely keep up with inflation rates. One way to boost those numbers is to think a bit more globally. There are better potential returns in emerging markets, but these often come with more portfolio volatility.

I cannot stress enough the importance of knowing what your savings rate should be. It will help you know what type of portfolio to invest in and how much risk you should take in your portfolio. It will add to the sleep-at-night factor.

FP Canada has a find a planner tool on their website.

Here is a link for my favourite independent planner, UPotential, which is affiliated with my company www.etfcm.com.

Follow Larry online:

Twitter: @LarryBermanETF

LinkedIn Group: ETF Capital Management

Facebook: ETF Capital Management

Web: www.etfcm.com