Workers rest at a construction site of new buildings on May 26, 2005 in Chengdu of Sichuan Province, China. In the past two months the Chinese government has raised taxes on real estate transactions and enacted other measures designed to discourage speculative dealing in property that it said had pushed real estate prices to unsustainable levels, pricing most local residents out of the market. (Photo by China Photos/Getty Images) Photographer: China Photos/Getty Images AsiaPac, Photographer: China Photos/Getty Images AsiaPac")

Chinese City of Chengdu Relaxes Home-Buying Rule to Revive Sales

Chengdu, a major city in the southwest China, removed home-buying curbs, joining dozens of peers in the country in an attempt to revive real estate demand and boost economic growth.

Latest Videos

The information you requested is not available at this time, please check back again soon.

Chengdu, a major city in the southwest China, removed home-buying curbs, joining dozens of peers in the country in an attempt to revive real estate demand and boost economic growth.

China Vanke Co. made a rare response to Moody’s downgrade last week, citing support from financial institutions and its biggest shareholder.

Billionaires who built their fortunes rolling out wireless networks when debt cost almost nothing are seeing their wealth crimped by higher borrowing costs and caution among money managers on the outlook for the industry.

Above and beyond the obvious damage, wildfires levied a hidden cost on the finance industry: Mortgage lenders and investors lost more than $30 billion between 2020 and 2022, due to both accelerated defaults and prepayments following disastrous blazes.

Crown jewels including resorts and a gas station chain are up for grabs. Saudi Arabia mulls purchases.

Aug 19, 2022

, Bloomberg News

Earnings results from alternative mortgage providers including Home Capital Group Inc. and EQB Inc. show that lenders are turning more cautious on Canada’s rapidly-cooling housing market and the economy.

Home Capital and EQB both missed analysts’ profit estimates as they stockpiled more capital than expected to protect against future loan losses. EQB’s chief executive officer said the firm is tightening lending standards, while Home Capital’s top executive said inflation, softening home prices and a possible recession may cause “stresses to the financial system.”

The comments and the earnings highlight “pockets of concern” arising among lenders, said Jaeme Gloyn, an analyst at National Bank of Canada. Investors will be watching closely to see what top executives at the country’s largest banks say about housing and the economy when they report fiscal third-quarter results this month.

“The provisions for credit losses generally came in a little bit higher than what was expected,” Gloyn said of the mortgage lenders’ results. Some of that is due to loan growth, he said, but it’s also because of changes in the economic models that Canadian lenders use to estimate expected credit losses.

EQ Bank, in a disclosure of the variables it uses to determine expected credit losses, reduced its base-case forecast for Canadian home-price growth over the next 12 months to 4.8 per cent last quarter from 5.6 per cent in the previous quarter. Home Capital was even more cautious, reducing its housing-price outlook to a 7 per cent decline, from a 1 per cent drop.

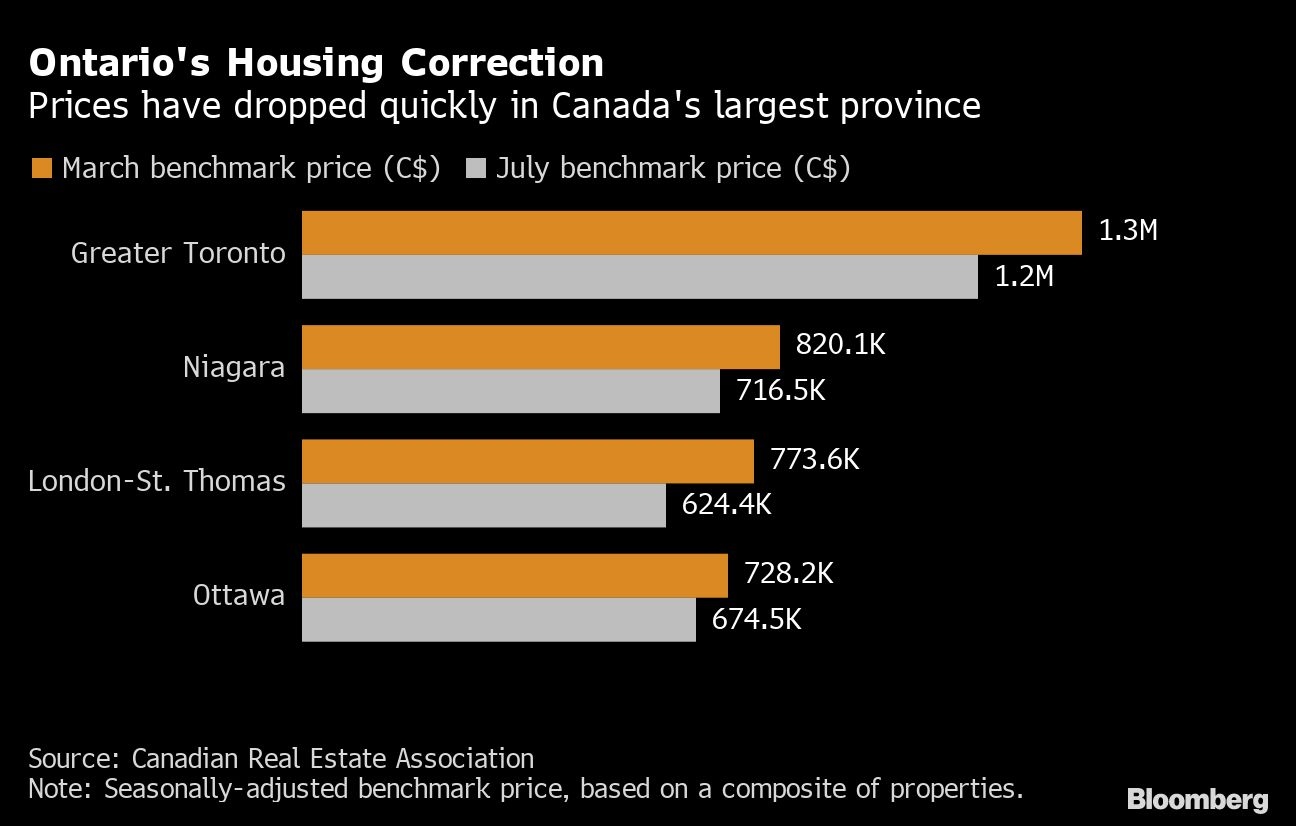

Canadian home prices have already started to retreat, dropping 1.7 per cent in July and bringing the cumulative drop from February’s peak to nearly 6 per cent, according to the Canadian Real Estate Association. Prices have dropped by double-digit percentages in a number of cities.

Canada’s six largest banks begin reporting their results for the quarter ended July 31 on Tuesday, and analysts are expecting them to take larger provisions for credit losses than in the previous quarter as the outlook worsens for the economy.

The variable that most directly affects loan losses is unemployment, and Canada’s labor market remains tight, with the jobless rate at a record low 4.9 per cent. That’s translating into a level of loan arrears that EQB CEO Andrew Moor said is the lowest in his 15 years leading the company.

And while Canada’s alternative lenders specialize in customer segments that the big banks avoid -- such as those who are new to the country, self-employed or have a bruised credit history -- they have strict underwriting guidelines, income-verification procedures and regulations designed to prevent a wave of defaults such as the US saw in the 2008 financial crisis, Gloyn said.

But that doesn’t make them immune to potential stresses. About 64 per cent of Home Capital’s borrowers will need to renew their mortgage within 12 months, and some could face payment increases of as much as CUS$850 (US$655) a month, stressing their ability to pay, Gloyn estimated in a note in July. EQB would likely have “roughly similar outcomes” in its Alt-A segment though the company doesn’t provide the disclosures needed to conduct that analysis, he said.

Home Capital nearly collapsed in 2017 after suffering a run on deposits when regulators alleged the company misled investors over the extent of fraudulent mortgage applications. Warren Buffett’s Berkshire Hathaway Inc. bought an equity stake of nearly 20 per cent and provided an emergency credit line to stabilize the firm.

Home Capital CEO Yousry Bissada, who took the helm after Berkshire’s rescue, said the lender may see its arrears increase and house prices soften. But he said borrowers would likely stop paying other debts before giving up on their homes and that the business is built to be a “fortress” in challenging times.

“We have strengthened our team and our culture, we’ve fortified our balance sheet and funding model,” he said on a conference call with analysts. “This makes us more resilient, and importantly, more nimble.”

Home Capital disclosed this week that it had rejected a takeover bid from an unnamed suitor.

EQB, for its part, is getting more cautious on refinancings, debt-service ratios and loan-to-value ratios, Moor said on the earnings call. Still, those are “tactical moves consistent with our past practice, not wholesale changes in our already-sound approach,” he said.

Canadian home prices may retreat to their levels from last September or October while avoiding “huge corrections” that challenge the Canadian economy, he said later in an interview with BNN Bloomberg Television.

“We’re always looking for the areas we think might be the riskiest and making sure that our loan book is in good shape,” Moor said.

Related