Nov 13, 2023

Oil price news: Oil holds run of weekly drops with focus on demand outlook

, Bloomberg News

Oil watcher Bill O'Grady says Americans falling out of love with driving

VIDEO SIGN OUT

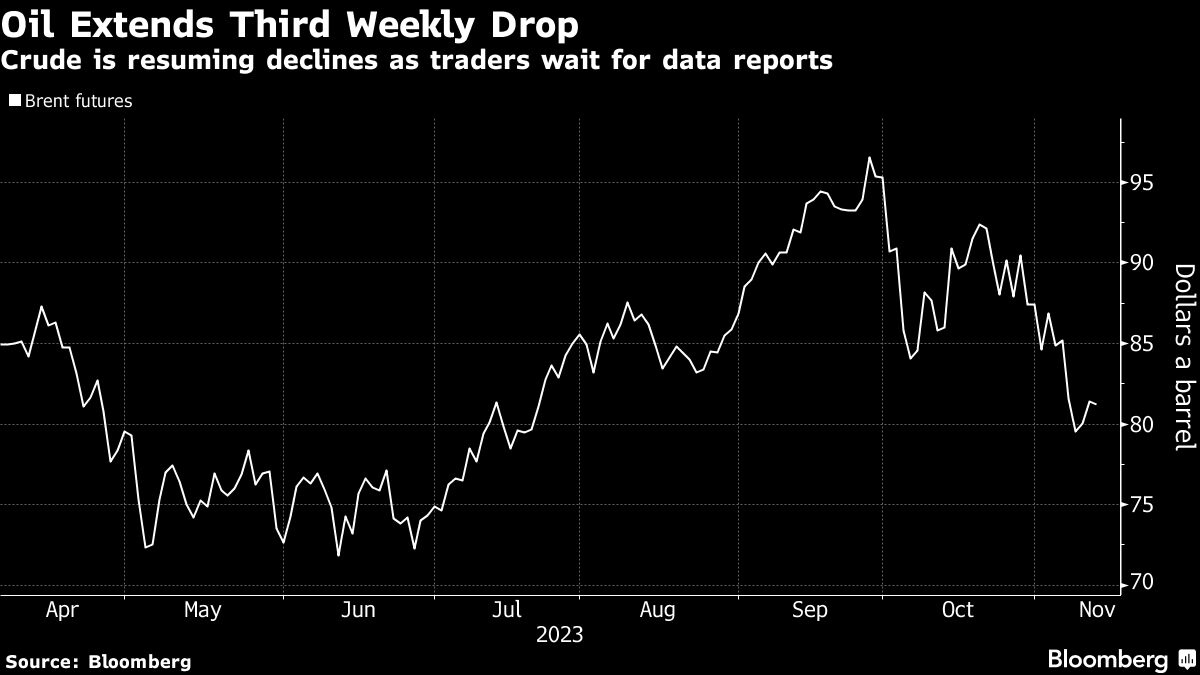

Oil held near US$81 after three weeks of declines as traders wait for industry reports to confirm whether the recent run lower has been overdone.

Brent crude erased an earlier decline to trade little changed, after losing about 12 per cent over the past three weeks. Analysts at Goldman Sachs Group Inc. said renewed demand concerns have driven the selloff, but that consumption has remained robust all year and will likely continue to do so in 2024. The bank also trimmed its price forecast for next year to US$92.

There will be a raft of key figures against which consumption can be measured this week, with OPEC publishing its monthly market report on Monday, followed by the International Energy Agency later in the week and two weeks’ worth of U.S. inventory data.

“Crude oil has started the week back on the defensive, but so far both Brent and WTI hold above key support levels, potentially indicating the worst of the long liquidation phase is behind us,” said Ole Hansen, Saxo Bank A/S’s head of commodity strategy. “Focus this week is on U.S. CPI from a general market risk perspective and oil market reports from the IEA tomorrow and not least OPEC.”

Oil rebounded slightly at the end of last week after Wednesday slipping below US$80 for the first time since July, with bearish consumption signals from China, the U.S. and Europe prevailing. Supply from the Middle East — the source of about a third of the world’s crude — has remained unaffected by the conflict between Israel and Hamas, while shipments from Russia and the U.S. are increasing.

Iraqi Oil Minister Hayyan Abdul Ghani is visiting the Kurdistan region to discuss the resumption of exports via Ceyhan in Turkey. The major pipeline has been halted since March because of a dispute between Turkey and Iraq and was also damaged by an earthquake.

Prices:

- Brent for January settlement was little changed at US$81.46 a barrel at 10:15 a.m. in London.

- WTI for December delivery was little changed at US$77.23 a barrel.