Feb 5, 2024

Bank of Canada measures suggest it's more hawkish than market thinks, Scotiabank says

, Bloomberg News

The Bank of Canada seems to be following U.S. Fed's playbook: economist

VIDEO SIGN OUT

The Bank of Canada’s decision to bring back a cash-management tool that it hasn’t used in years suggests policymakers don’t want to start loosening monetary policy soon, Bank of Nova Scotia economist Derek Holt says.

The central bank said Friday it will soon restart auctions of Canadian government cash balances, something it hasn’t done since August 2020. Some strategists see that as another move to inject liquidity into short-term funding markets — which, in turn, might buy the central bank more time to continue its quantitative tightening program.

The announcement “could indirectly serve as a signal that they are more hawkishly inclined than markets are pricing,” Holt said in a report to investors. “Doubling down on QT while relying upon a complex patchwork of funding tools like repo injections and this latest step could be an implicit signal they are nowhere close to easing — if not inclined to tighten further.”

The Bank of Canada began quantitative tightening in April 2022, ending its purchases of Canadian government bonds and allowing its balance sheet to shrink as existing bond holdings mature without replacement. The process removes liquidity from the system.

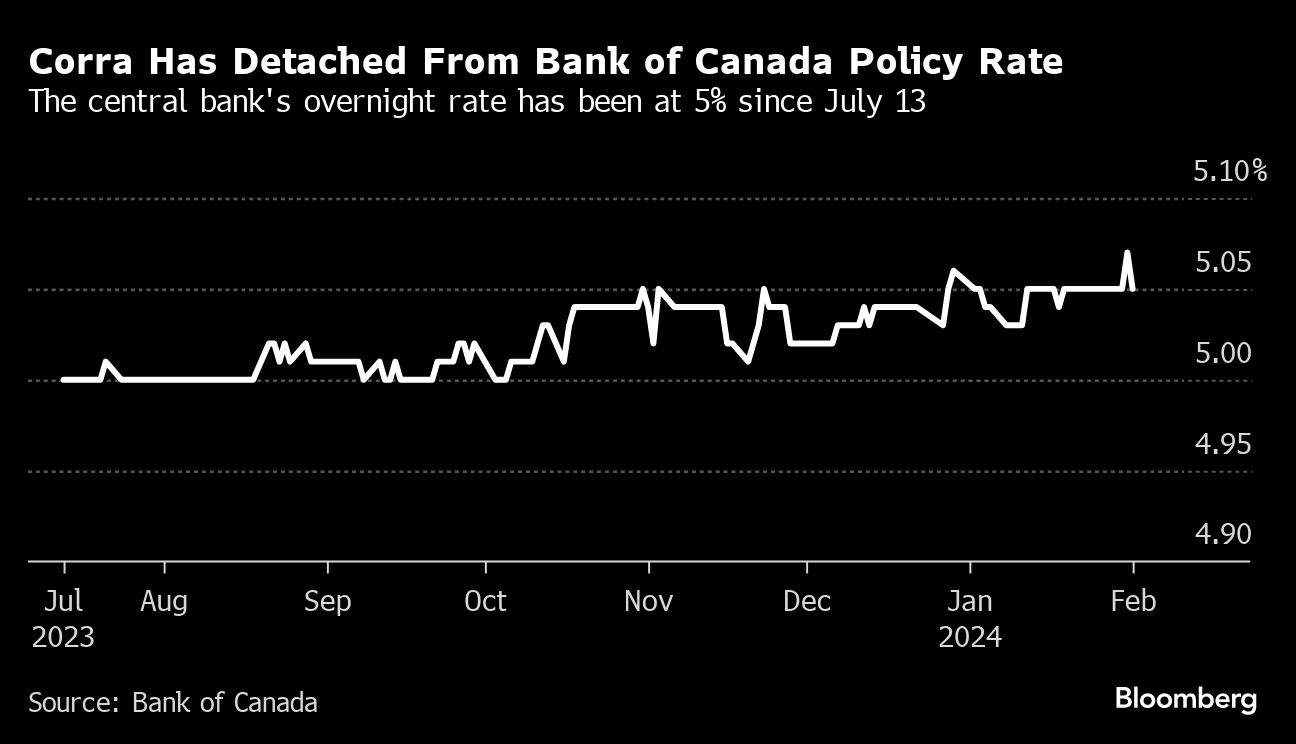

Recently, short-term funding strains are showing up in the Canadian Overnight Repo Rate Average. Corra measures the cost of overnight money using Canadian government treasury bills and bonds as collateral for repurchase transactions. It’s supposed to closely track the Bank of Canada’s benchmark policy rate — currently 5 per cent — but has been settling above that level for months.

That’s led to some debate in the market about whether the central bank will need to end its QT program earlier than anticipated.

Last year, Bank of Canada Governor Tiff Macklem said the central bank expected to continue QT while rates were normalizing. Policymakers have indicated they think they will wind down the program by the end of 2024, or early next year, but haven’t provided a recent update on their plans.

If the reintroduction of the cash-auction program brings Corra down closer to 5 per cent, it means “more run-room for QT,” Taylor Schleich, a rates strategist with National Bank of Canada, said by email. “That’s going to depend on how much the program is used, so it’s hard to say at this point.”

Corra settled at 5.07 per cent on Wednesday, a new high, before falling back to 5.05 per cent on Friday. Traders in overnight swaps see the Bank of Canada starting rate cuts by July.