Sep 6, 2023

Oil edges away from US$90 after OPEC+ leaders extend supply cuts

, Bloomberg News

The weakness in China has been a long time coming: Strategist

VIDEO SIGN OUT

Brent oil retreated from US$90 a barrel as traders digested a decision by OPEC+ leaders Saudi Arabia and Russia to extend supply curbs through the end of the year.

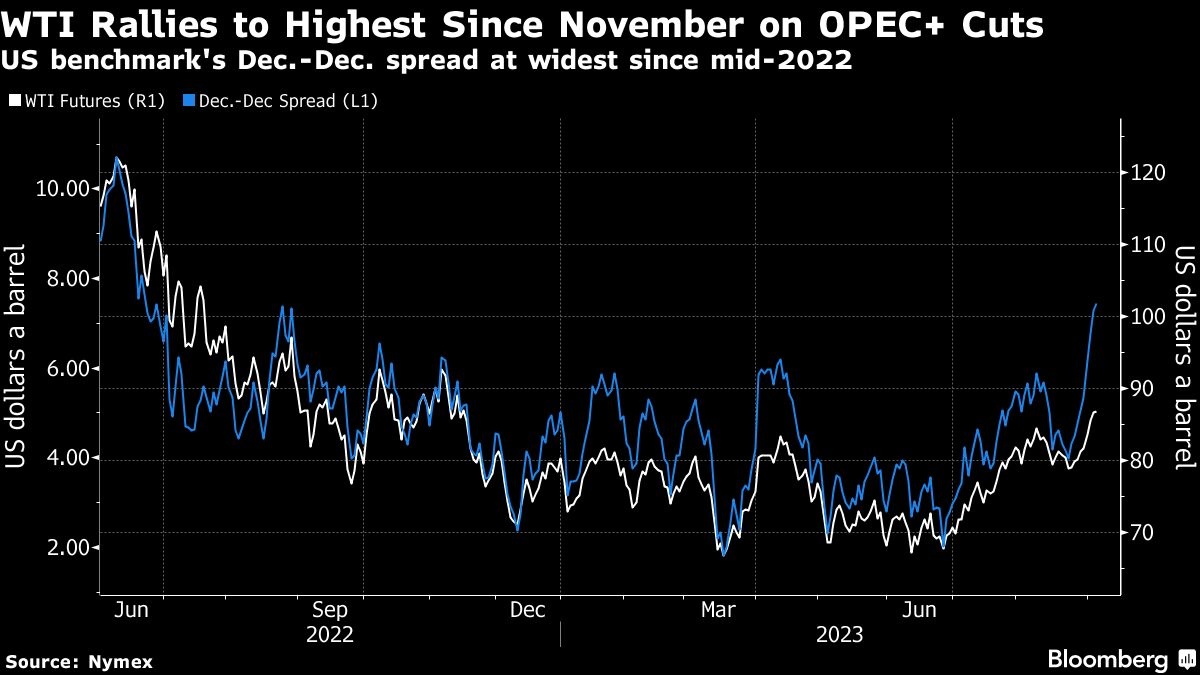

The global benchmark fell 0.8 per cent on Wednesday, having closed at the highest since November a day earlier. Risky assets were generally on the back foot after weak German economic data.

The strategy from Riyadh and Moscow aims to drain inventories further, while driving the market's underlying timespreads deeper into backwardation, a bullish pricing pattern. Still, in the near term, crude is flashing warnings that it is overbought on 14-day Relative Strength Index basis, raising the risk of a pullback.

Oil has rallied sharply this quarter after the Organization of Petroleum Exporting Countries and its allies adopted group-wide supply cuts that were then supplemented by additional, voluntary reductions. The production restraints have been implemented just as the International Energy Agency estimates that global crude consumption is running at a record pace.

“It was absolutely a surprise,” said Nadia Martin Wiggen, a director at commodities-focused hedge fund Svelland Capital. “When we look toward the start of next year after these cuts, we're going to see OECD commercial stock levels at lows we haven't seen except in very big years.”

Goldman Sachs Group Inc. said that the moves by OPEC+ brought bullish risks to its outlook for prices, according to a report. The bank's analysts outlined several scenarios, including one that saw Brent extending gains to above US$100 a barrel, though they stressed that this wasn't a base-case view.

Prices:

- WTI for October delivery fell 0.7 per cent to US$86.05 a barrel at 10:28 a.m. in London.

- Brent for November settlement dipped 0.8 per cent at US$89.33 a barrel.