Jul 4, 2023

Real estate leads European stock gains; oil rises

, Bloomberg News

BNN Bloomberg's mid-morning market update: July 4, 2023

VIDEO SIGN OUT

European real estate shares headed for their biggest three-day advance since March, while oil climbed as traders weighed supply cuts.

Global stock market trading was light on Tuesday, with US exchanges closed for the Independence Day holiday. Europe’s Stoxx 600 edged higher on trading volume that was a third lower than the 30-day average. US futures were little changed, while Canada’s benchmark equity gauge rose.

Real estate topped gains among European industry groups as Swedish property manager Castellum AB jumped as DNB Bank ASA recommended buying the stock because of its attractive valuation. Belgium’s Warehouses de Pauw CVA rose after boosting its earnings outlook.

Deal activity also sparked investor interest on Tuesday. Vienna-based OMV AG surged after Bloomberg News reported the firm and Abu Dhabi are in talks to create a chemicals and plastics company worth more than US$30 billion.

Meanwhile, Casino Guichard-Perrachon SA shares were suspended after surging 16 per cent, as the French retailer received offers from Czech billionaire Daniel Kretinsky and a group led by telecom billionaire Xavier Neil.

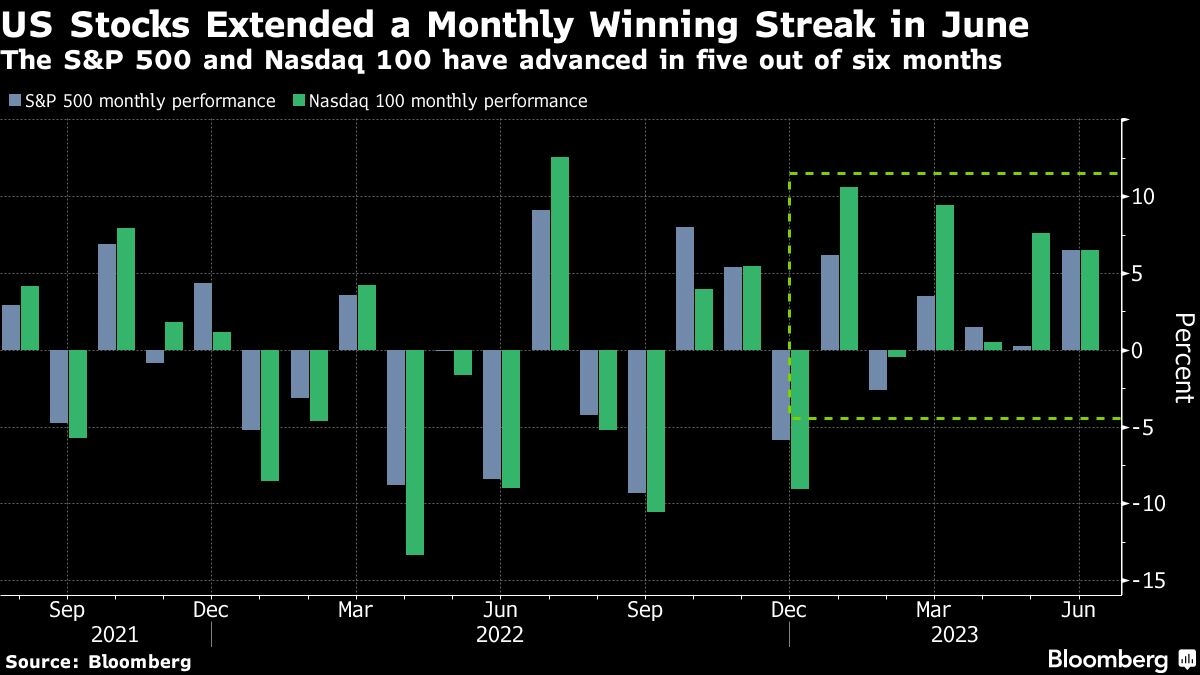

After stocks rallied in the first half of the year, investors are worried that higher rates and a worsening economic backdrop will limit gains from here on. Friday’s nonfarm payrolls report will be closely watched for clues on the trajectory of monetary policy, before focus turns to the earnings season next week.

Meanwhile, strategists are increasingly warning about the risks to US stocks after a steep first-half rally. Citigroup Inc.’s Chris Montagu said positioning looks “very extended” and cited data showing that investors piled into bullish bets on US stock futures toward the end of June.

Among other notes of caution, Goldman Sachs Group Inc. strategists wrote that it’s too early to dismiss the risk of higher interest rates weighing on stocks. On Monday, a key segment of the Treasury yield curve approached its most inverted level in decades, with the two-year note yield exceeding the 10-year rate by as much as 110.8 basis points.

“We remain cautious on equities amid a broadly muted economic backdrop,” said Luca Paolini, chief strategist at Pictet Asset Management. “A gap has opened up between earnings expectations and leading economic indicators. At some point, the gap will have to close. Either the economy will rebound — which we think unlikely — or equities will reprice.”

Elsewhere, Brent crude traded near US$76 a barrel as oil traders considered the effects of output cuts. On Monday, Saudi Arabia said that it will prolong a unilateral 1 million barrel-a-day supply reduction into August, a move traders had widely expected. Russia announced a reduction in exports, while Algeria planned to make more modest curbs.

In Asia, Sri Lankan stocks jumped the most in more than a year as a plan to revamp domestic debt eased concern over financial sector stability. Japan’s Nikkei 225 fell from its highest level since 1990.

Pakistan’s rupee rallied against the dollar on optimism the International Monetary Fund’s bailout will boost demand for the nation’s assets.

Shares of Chinese non-ferrous metals firms climbed after the government imposed restrictions on exports of gallium and germanium in an escalation of the trade war on tech with the US and Europe. The metals are crucial for the semiconductor, telecommunications and electric-vehicles sectors.

Key events this week:

- China Caixin services and composite PMI, Wednesday

- Eurozone S&P Global Eurozone services PMI, PPI, Wednesday

- OPEC International Seminar, speakers including OPEC+ oil ministers, kicks off in Vienna, Wednesday

- FOMC issues minutes on June policy meeting, Wednesday

- New York Fed President John Williams in “fireside chat” at meeting of the Central Bank Research Association at the New York Fed, Wednesday

- US initial jobless claims, trade, ISM services, job openings, Thursday

- Dallas Fed President Lorie Logan speaks on a panel about the policy challenges for central banks at CEBRA meeting, Thursday

- US unemployment rate, nonfarm payrolls, Friday

- ECB’s Christine Lagarde addresses an event in France, Friday

Some of the main moves in markets today:

Stocks

- The MSCI Asia Pacific Index was little changed as of 5:11 p.m. New York time

- S&P 500 futures were little changed

Currencies

- The Bloomberg Dollar Spot Index was little changed

- The euro was little changed at US$1.0882

- The British pound was little changed at US$1.2714

- The Japanese yen was little changed at 144.46 per dollar

- The offshore yuan was little changed at 7.2292 per dollar

- The Mexican peso was little changed at 17.0555

Cryptocurrencies

- Bitcoin was little changed at US$30,801.71

- Ether fell 0.1 per cent to US$1,940.24

Bonds

- The yield on 10-year Treasuries was little changed at 3.85 per cent

- Germany’s 10-year yield advanced two basis points to 2.45 per cent

- Britain’s 10-year yield declined two basis points to 4.42 per cent

Commodities

- Brent crude rose 2.1 per cent to US$76.25 a barrel

- Spot gold rose 0.2 per cent, climbing for the fourth straight day, the longest winning streak since March 13