Aug 23, 2023

Canada bank results seen hit by expenses, strained consumers

, Bloomberg News

Major challenges ahead for Canada's big six banks and the TSX: Portfolio manager

VIDEO SIGN OUT

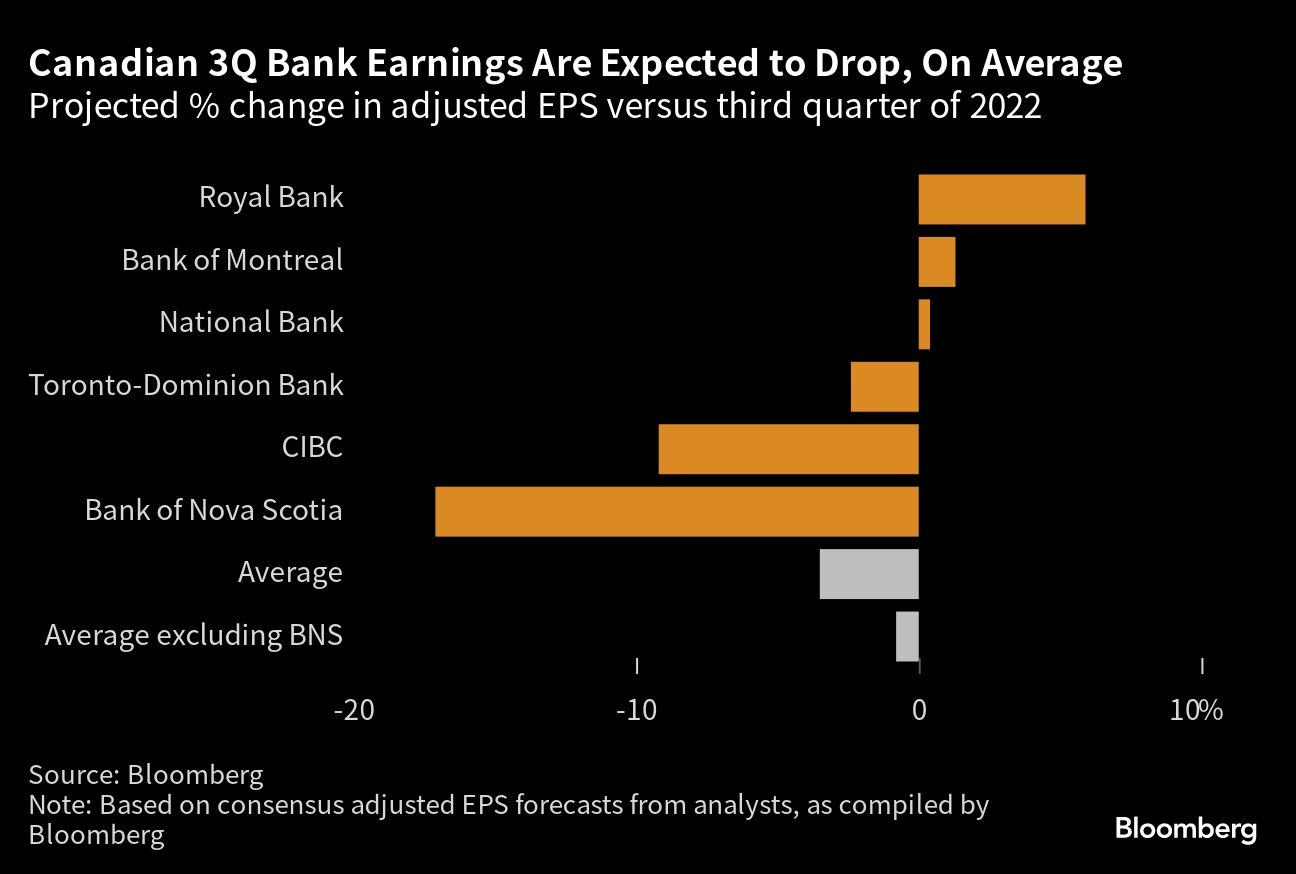

After months of underperforming the broader market, Canada’s Big Six banks are likely to continue struggling as expenses and loan-loss provisions rise and consumer finances deteriorate.

Higher interest rates are expected to hurt lenders’ fiscal third-quarter earnings when they begin to report Thursday. Inflation data on both sides of the border have ratcheted up bets that central banks could raise rates further still, which would further erode spending power and borrowing demand. Analysts expect that higher rates could have banks bracing for elevated funding costs and lagging loan growth.

Another obstacle: The quarterly results won’t get the same revenue lift generated during the pandemic. Given those hurdles, Bank of Nova Scotia analyst Meny Grauman reversed his late July “tactical trade” call in which he said banks had a chance to start closing their performance gap with life insurers and their U.S. peers.

“Events over the last two weeks now suggest that this window of opportunity may have closed even before it really opened,” Grauman wrote in an Aug. 18 note.

Grauman, who holds a bearish view on the banks if inflation doesn’t slow enough to warrant rate cuts next year, also flagged recent credit downgrades on small and midsize U.S. banks as another drag on sentiment.

The S&P/TSX Composite Commercial Banks index bounced back Wednesday from a seven-day slump, the longest losing streak in more than two years, to gain 1.2 per cent as of 2:13 p.m. in Toronto. Still, the gauge has dropped over 4 per cent this year, compared with a 2.7 per cent gain for the broader Canadian benchmark and the composite insurance index’s 7 per cent advance.

At the biggest U.S. banks, better-than-expected second-quarter results raised speculation that Canadian lenders might have had similar success in their most-recent quarter, which ended July 31. But National Bank of Canada analyst Gabriel Dechaine pushed back on these hopes in an Aug. 10 note, pointing to continued pressure from funding costs, among other factors.

The banks have cost issues — non-interest expenses grew 12 per cent across the sector in the first half of the year, Dechaine calculated in a June 6 note. The Big Six could record restructuring charges to the tune of $3 billion (US$2.2 billion) that he expects will be recorded mostly in the fourth quarter. He also pointed to expense growth in the low-teens in the second quarter as a negative surprise he said could emerge again in the third quarter.

Rising expenses come as the banks stand to gain less revenue as capital markets and merger activity continues to slump. Royal Bank of Canada analyst Darko Mihelic lowered his core earnings expectations for Canada’s biggest banks by an average of 6 per cent from last year for that reason. Mihelic’s team expects capital markets revenue on the banks he covers to show a 9 per cent decline from last year.

Not all analysts are downbeat. Market-watchers have set the bar so low that Barclays Plc analyst John Aiken made the case that banks could surpass expectations and bring an upside surprise. He raised his price targets on most of the banks this week.