Apr 9, 2024

U.S.-style oil megadeals viable in Canada, BMO energy banker says

, Bloomberg News

Cenovus Energy's oil streams operations stood out in Q4: analyst

VIDEO SIGN OUT

A U.S.-style megadeal is possible in Canada’s oil patch, though the pressures that pushed Exxon Mobil Corp. and Chevron Corp. to pursue large takeovers aren’t as strong north of the border, says Bank of Montreal’s top energy banker.

Investors would likely support mergers between major Canadian energy producers that increased scale and improved cost efficiencies — and Canadian companies are in a position to do such deals, said Brad Wells, head of energy at BMO Capital Markets.

But the need to add drilling inventory that helped drive Exxon into its $60 billion offer to buy Pioneer Natural Resources Co. in October and Chevron to pursue a $53 billion acquisition of Hess Corp. isn’t a factor in Canada, where oil-sands companies are sitting on decades of supply, he said in an interview.

The overall health of Canadian companies — including balance sheets strengthened by recent gains in oil prices — reduces the impetus to transact and allows them to be opportunistic, making it difficult to predict when such a deal may happen, he said.

“It all comes down to what it looks like: the economics, the strategic rationale, the pro forma business and balance sheet, the price being paid,” Wells said. “All that needs to align for there to be investor support.”

Smaller deals already have been happening in Canada. BMO advised Crescent Point Energy Corp. on its $2.05 billion acquisition of Hammerhead Energy Inc. in December. The bank is also advising Enerplus Corp. on a $3.57 billion takeover offer by US driller Chord Energy Corp., announced in February.

Wells said he’s seeing an uptick in interest from U.S. buyers in the past year, particularly private companies. The banker spoke in advance of the Bank of Montreal and Canadian Association of Petroleum Producers Energy Symposium in Toronto, where executives from major producers including Canadian Natural Resources Ltd., Suncor Energy Inc. and Cenovus Energy Inc. are scheduled to speak Tuesday and Wednesday.

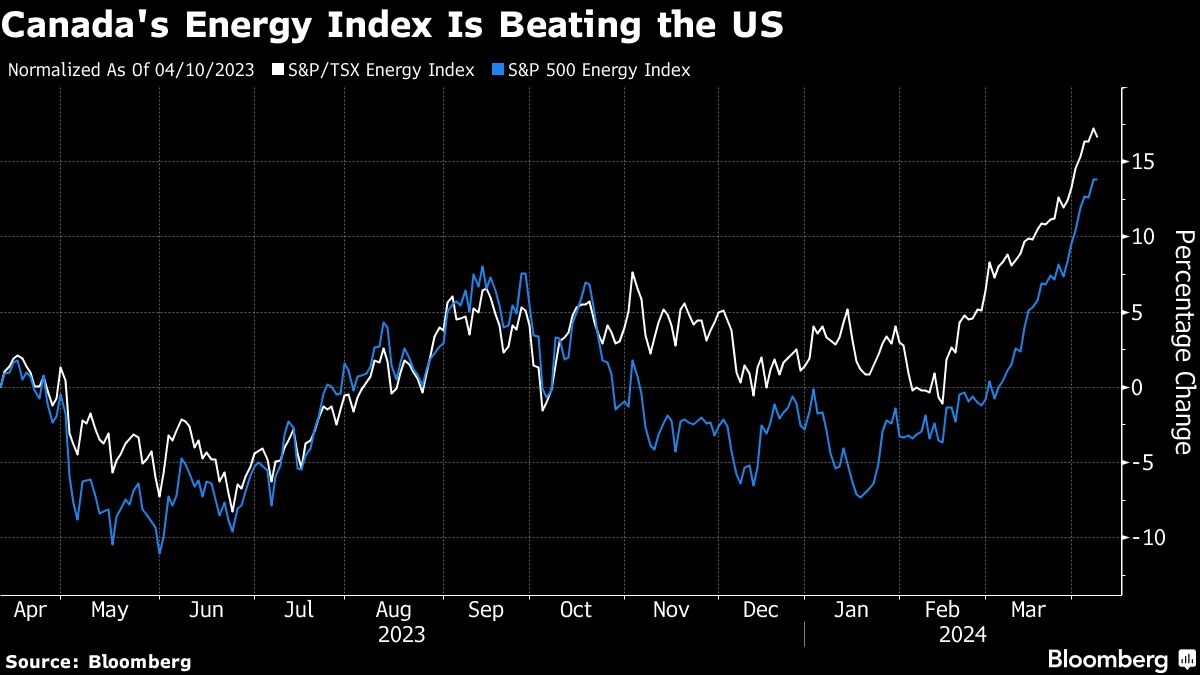

The industry has a lot to celebrate this year. Globally, oil prices are strong, driven by resilient demand, geopolitical concerns and production cuts by OPEC and its allies.

Fears that central banks’ tightening campaigns would push economies into recession have faded, and even the desire for rate cuts to increase consumption are now a marginal factor in the market, taking a back seat to incremental demand from China and India, Wells said.

The price strength has helped Canadian producers pay down debt, and many are approaching leverage levels that will allow them to commit most, if not all, of their free cash flow to shareholder returns through dividends and buybacks, he said.

Looking ahead, the industry may also benefit from Mexico’s decision to curtail some exports of its medium sour crude, forcing U.S. refiners to replace it with Canadian heavy oil, he said.

At the same time, the long-awaited expansion of the Trans Mountain pipeline — which carries crude from Alberta’s oil sands to a Pacific Coast port — is scheduled to begin operation next month, allowing more Canadian crude to flow along the U.S. West Coast and to Asia, he said.

“I think 2024 will be a turning point for the Canadian oil sector,” Wells said. “It will be the first time in at least a decade that there is excess pipeline capacity out of the Western Canadian Sedimentary Basin, which will be a game-changer for the sector.”