Jun 11, 2020

Oil dives the most in six weeks, exposing a fragile recovery

, Bloomberg News

Ways Canada's oil and gas industry could pivot to low carbon

VIDEO SIGN OUT

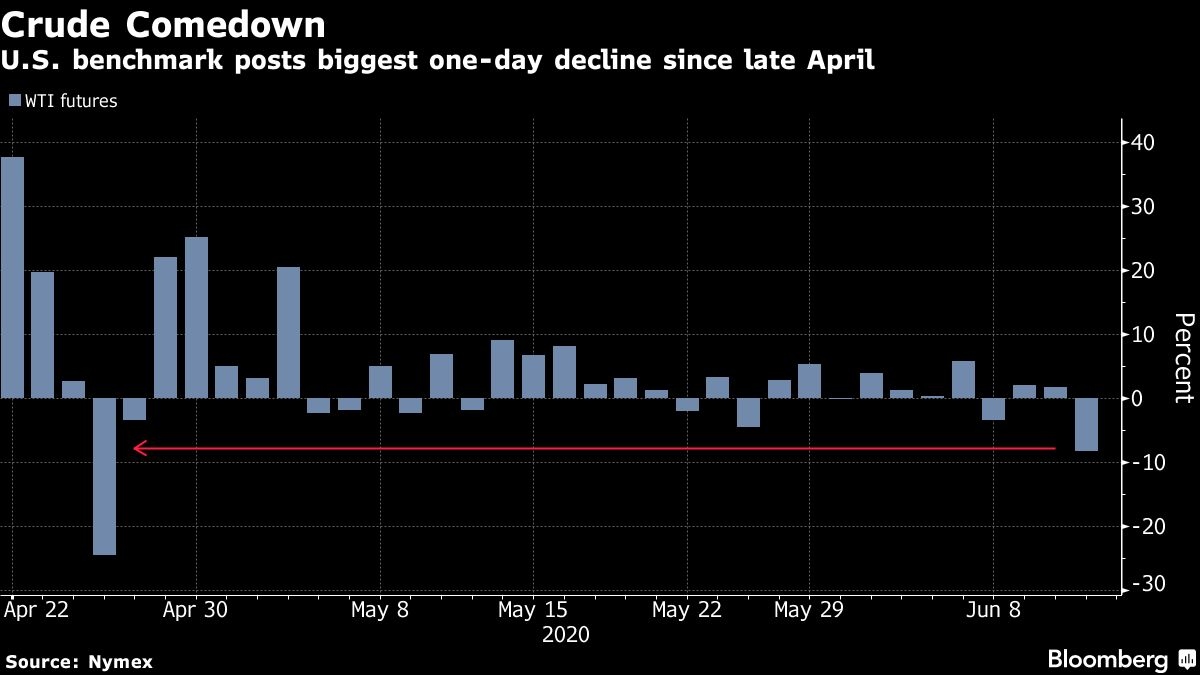

Oil fell the most since late April as economic uneasiness iced U.S. stock markets, threatening to spoil crude’s recovery from a historic drop below zero.

The market is grappling with record high U.S. oil inventories and an uneven demand rebound as signs mount that a second wave of the pandemic could be taking hold in some states. U.S. jobless claims remained high, underscoring longer-term macroeconomic challenges a day after the Federal Reserve provided a grim outlook for the economy. Oil’s recovery has been driven by production cuts and the easing of pandemic-related lockdowns.

“It was very fast, driven by historically unprecedented OPEC+ cuts and central bank and government support on the demand side,” said Bart Melek, head of commodity strategy at Toronto Dominion Bank. “We should not be surprised to see a pullback, following such a violent rally,” he said.

On the supply side, higher prices have pushed some producers to turn on the taps. U.S. crude stockpiles rose last week to 538.1 million barrels, according to the Energy Information Administration. That’s the highest level in data compiled by Bloomberg since 1982.

“The surprisingly bearish stats, particularly on crude, the relatively dour comments by the Fed yesterday and fears of a resurgence of the coronavirus have all added to the price weakness today,” said Thomas Finlon, of Houston-based GF International.

Prices

West Texas Intermediate for July delivery fell US$3.26 to settle at US$36.24 a barrel in New York, the biggest drop since April 27.

Brent crude for August delivery dropped US$3.18 to close at US$38.55 a barrel, the biggest decline since April 21.

Crude’s inability to sustain prices over US$40 a barrel is leaving many companies across the industry in dire straits.

“A couple months ago, the sector was in complete survivor mode, and it still needs to be, quite frankly,” said Jennifer Rowland, an analyst at Edward Jones & Co. “Even at (US)$45, there will be a lot of companies that can’t survive,” she said. “Companies are still going to be bleeding cash at this level.”

In a more positive sign, data showed that oil demand in the U.K. has been steadily recovering in recent weeks. Still, there’s still a massive glut to be cleared globally, including more than 180 million barrels of crude stored at sea, according to Vortexa data.

Other oil-market news

-Chesapeake Energy Corp.’s momentum and volatility may be tied to recent interest among retail investors trading on platforms like Robinhood.

-S&P Global Platts, the organizer of Singapore’s Annual Asia Pacific Petroleum Conference, just announced that it’s going to hold the event virtually because of the coronavirus.

-Trafigura Group reported a 27-per-cent gain in half-year net income as the commodities trading giant benefited from supply and demand disruptions created by the virus pandemic.

--With assistance from Alex Longley, James Thornhill and Saket Sundria.