May 11, 2022

Stock-and-bond rout turns financial clock back to Christmas 2018

, Bloomberg News

S&P 500 could drop to 3500 points; 75bps rate hikes possible for Canada and U.S.: David Rosenberg

VIDEO SIGN OUT

Rising interest rates, plummeting stocks and the surging dollar have tightened reins on the economy to a point where the Federal Reserve has previously cried uncle. No such capitulation should be expected this time.

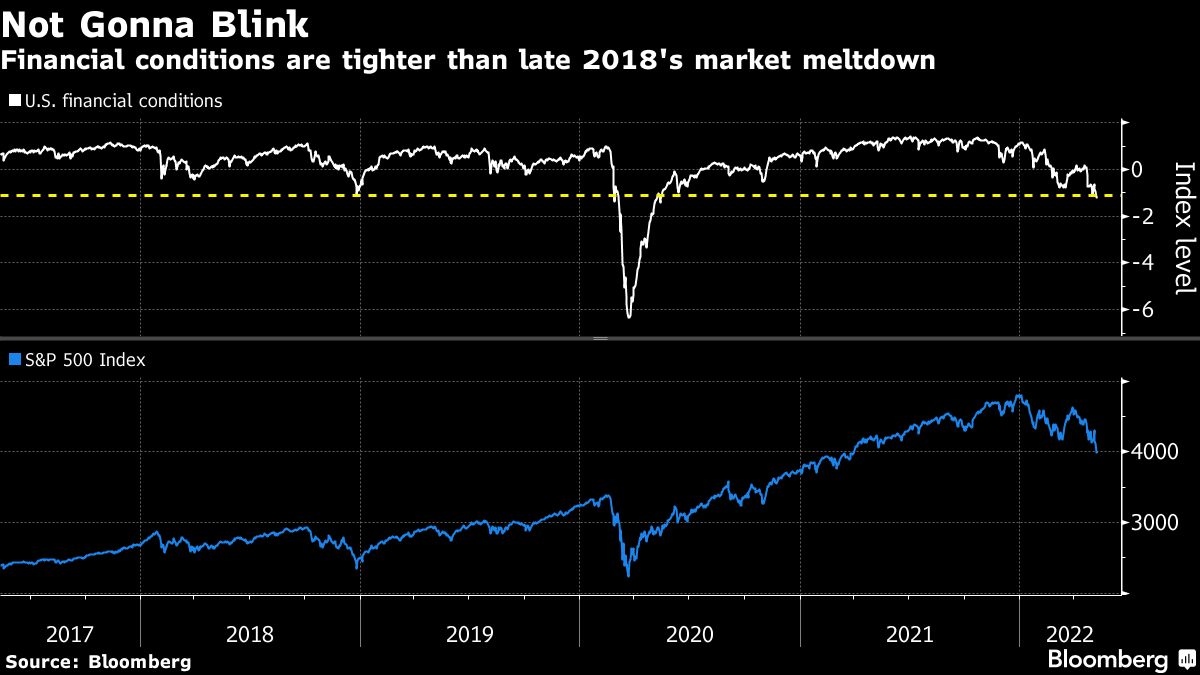

Financial conditions, a multi-input measure of nervousness across equity and fixed-income markets, have constricted to roughly the same levels they reached at the height of the central bank’s last tightening campaign, at Christmas 2018, a Bloomberg measure shows. It was then, with the S&P 500 just points away from a bear market, that Fed Chair Jerome Powell decided enough was enough and stopped hiking rates.

Less than four years later, with inflation raging like no time in 40 years, things have changed dramatically. That was clear on Tuesday, when Cleveland Fed President Loretta Mester said, after the first half-point rate rise in 22 years, policy makers can’t rule out even bigger boosts in the future to bring inflation under control. Fed Governor Christopher Waller came next, describing the labor market as “overstimulated” and reiterating Powell’s view that the economy can stand higher rates.

The message for investors is a grim one. As bad as things have been in markets and for increasing number of corporate debtors, and as tight as they’re threatening to make things for the economy, it would trouble policy makers little if things got worse. If anything, the moves could help them make up for not having started to shift policy sooner.

“The Fed is really happy financial conditions are tight,” said George Pearkes, global macro strategist at Bespoke Investment Group. “They would way rather the market do the moving for them and then not deliver on tightening. That’s being ahead rather than behind the curve, as it were. That appears to be the most likely scenario right now.”

Barring a “complete meltdown” in US stocks or credit, it’s highly unlikely the Fed will ease up on inflation, according to BMO Capital Markets.

A report Wednesday was the latest trigger for volatility. The 0.6 per cent gain in the core measure of consumer prices in April from the previous month -- bigger than all forecasts in Bloomberg’s survey -- wiped out a gain in S&P 500 futures and sent two-year yield soaring as investors boosted bets on further Fed policy tightening.

“Given how much of a political hot-button issue inflation has become, the odds are low that the Fed will take its foot off the brakes before the midterm elections,” BMO strategist Ian Lyngen wrote in a note Tuesday. Republicans have sought to make the surge in living costs a top issue in November’s congressional ballots.

Right now, market turmoil is merely a means to the Fed’s ends. The technology-heavy Nasdaq 100 has plunged more than 24 per cent this year, dragged down by a bond selloff that saw 10-year Treasury yields reach 3.2 per cent on Monday. The credit market is also showing some pressure, with high-yield premiums hitting the highest since November 2020.

The effects of tighter financial conditions can be felt beyond stock prices. Initial public offerings and corporate-credit issuance has slowed as the cost of funding climbs, according to Jefferies LLC.

Still, no Fed official who’s spoken since the May 4 policy meeting has expressed concern about the market volatility or the state of the US economy.

For her part, Treasury Secretary Janet Yellen, came close to endorsing the dollar’s climb toward 2020 crisis-level highs. The greenback is being pushed higher by rising US rates, “and in a way that’s part of how a tighter monetary policy works,” the former Fed chair said last Wednesday. On Tuesday, New York Fed President John Williams that the US unemployment rate could climb from the current 3.6 per cent, it wouldn’t be “in a huge way.”

Citigroup Inc. economists warned against any conclusion that Fed policy makers are currently hitting their peak hawkishness, as strategists from JPMorgan Chase & Co. have suggested. There’s a potential for a ramp-up in the so-called terminal rate -- the endpoint for the policy benchmark for the cycle.

PEAK STILL PENDING

That might not come until September, if core inflation proves sticky and it’s evident the central bank has significantly more work to do, the bank’s team wrote in a Tuesday note. The Fed is expected is deliver two more 50-basis points hikes at its next two meetings, swaps pricing shows.

“Financial conditions have tightened rapidly, causing some to speculate that we are at the moment of ‘peak hawkishness,”’ Citigroup economists led by Andrew Hollenhorst wrote. “That is a possible outcome, but not a likely one given the trajectory of inflation,” they wrote. “We continue to see risks as balanced toward a further hawkish move from the Fed.”