Oct 12, 2023

U.S. stocks, bonds fall as CPI boosts Fed-hike wagers

, Bloomberg News

Get out of equities, we're headed towards a long-recession bear market: Portfolio Manager

VIDEO SIGN OUT

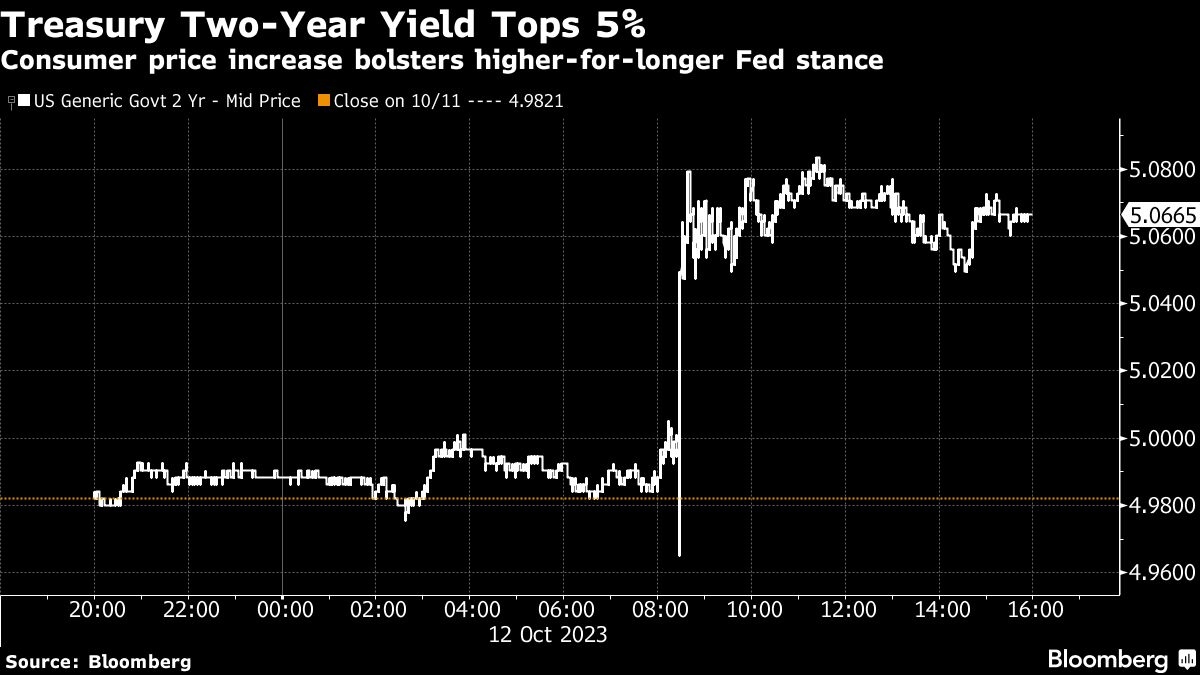

Stocks fell and Treasury yields rose as data bolstered speculation the Federal Reserve is nowhere near declaring victory over inflation — with bets on another hike this year climbing.

The S&P 500 halted a four-day advance. Bank shares underperformed ahead of results from JPMorgan Chase & Co., Citigroup Inc. and Wells Fargo & Co. Friday. Bonds dropped across U.S. the curve, with the 30-year rate surging as much as 19 basis points after an auction of the securities drew weak demand. The dollar gained the most in five weeks. Swap contracts pushed the odds of another quarter-point Fed hike to about 40 per cent — from closer to 30 per cent Wednesday.

The so-called core consumer price index, which excludes food and energy costs, increased 0.3 per cent last month. From a year ago, it rose 4.1 per cent, the lowest since 2021. Economists favor the core gauge as a better indicator of underlying inflation than the overall CPI. That measure climbed 0.4 per cent, boosted by energy costs. Forecasters had called for a 0.3 per cent monthly advance in both the overall and core measures.

“As for how this will impact interest rates, at this point, ‘higher-for-longer’ may be more important than ‘how high?’ said Richard Flynn, managing director at Charles Schwab UK. “Whether or not the Fed opts for hikes, it’s unlikely we’ll see rates drop below where they are for as long as the inflation dragon proves difficult to slay.”

While swap contracts continue to anticipate a Fed pivot to rate cuts next year, that outcome was assigned somewhat lower odds.

“Bottom line: the Fed can likely pause in November, though it’s a close call, and it remains too soon to consider cuts,” said Don Rissmiller at Strategas.

Yet some analysts and traders don’t think the report was surprising enough to move the needle, especially after a raft of Fed officials speaking this week said the rout in bond markets may suspend the need to tighten further for now.

Fed Governor Christopher Waller noted Wednesday the US central bank can watch and see what happens before taking further action with interest rates as financial markets tighten. Vice Chair Philip Jefferson on Monday said he would “remain cognizant of the tightening in financial conditions through higher bond yields.” And Dallas Fed President Lorie Logan indicated that if risk premiums in the bond market are on the rise, that “could do some of the work of cooling the economy for us, leaving less need for additional monetary policy tightening.”

“We don’t expect any more hikes,” said Matt Bush, U.S. economist at Guggenheim Investments. “I don’t think they’re going to see a great need to come out and hike at the Nov. 1 meeting. And beyond that, we’re going to see signs of a slower economy throughout the fourth quarter, a weaker labor market and that will take more pressure off them to hike again.”

To Tiffany Wilding at Pacific Investment Management Co., the CPI is likely to create some anxiety for Fed policymakers.

“We’ve been skeptical that the Fed would actually deliver the hike projected in the second half of 2023 by the majority of Fed officials, but at this point we are leaning toward them getting it in despite the recent tightening in financial conditions,” she noted. “It’s a very close call.”

More on CPI and Fed Outlook:

- Jason Pride, chief of investment strategy and Research at Glenmede:

- “There’s very little in today’s CPI report that suggests it’s mission accomplished for the Fed getting the inflation genie back in the bottle. Heading into year end, the Fed may still choose to raise rates once more, though it may be attentive to already tightening financial conditions due to the rise in long-term rates over the last few months. Another rate hike should remain on the table for now.”

- James Rossiter, head of global macro strategy at TD Securities:

- “This number is strong enough to keep the market on its toes with respect to another Fed hike. We don’t think it’ll happen, but the small upside surprise here challenges that view just a tiny bit.”

- Giuseppe Sette, president at Toggle AI:

- “A mixed report leaves the Fed hanging. We could get one more hike, or none at all, but the key point is different: even if CPI was to stabilize at this level and not fall more, Fed rates are already appropriate. The hiking cycle is done for good.”

- Mike Loewengart, head of model portfolio construction at Morgan Stanley Global Investment Office:

- “Today’s slightly-hotter-than-expected CPI and tame weekly jobless claims didn’t do anything to move the needle on inflation or the interest rate outlook. The odds may favor the Fed leaving rates unchanged at its November meeting, but rates are still likely to remain high for the foreseeable future.”

- Chris Zaccarelli, chief investment officer at Independent Advisor Alliance:

- “The bond market is sending a message that it is still worried about inflation and that the Fed will make good on its promise to keep rates higher for longer. We believe it’s a coinflip as to whether or not the Fed raises rates on Nov. 1.”

- Will Compernolle, macro strategist at FHN Financial:

- “The worrying aspects of the September CPI are probably not enough to cause the Fed to hike 25bp at its next meeting, but the next week of Fed commentary could prime market expectations for a future hike. Rising price pressures in proxies for underlying inflation — the inflation when noisier aspects are zeroed out — should temper any confidence that the Fed has reached its terminal rate.”

- Krishna Guha, vice chairman of Evercore:

- “The September CPI report is not a good one for the Fed, but will keep the U.S. central bank in wait-and-see mode. With yields much higher than they were a couple of months ago – and we think likely to step back up again when the Israel crisis and geopolitical risk-off ultimately abates – and wider financial conditions much tighter on net we continue to think the Fed is done here.”

- “In our baseline, the implication of this bumpier data will instead be to reinforce the Fed’s high-for-longer priors on rates – up until the point at which the drag from higher yields becomes more apparent, which even if we are right will take some time to materialize.”

- “The September CPI report is not a good one for the Fed, but will keep the U.S. central bank in wait-and-see mode. With yields much higher than they were a couple of months ago – and we think likely to step back up again when the Israel crisis and geopolitical risk-off ultimately abates – and wider financial conditions much tighter on net we continue to think the Fed is done here.”

Corporate Highlights

- Delta Air Lines Inc. slumped after cutting the high end of its outlook for 2023 profit on rising fuel prices and larger-than-expected aircraft maintenance costs.

- Walgreens Boots Alliance Inc. prepared for the arrival of its new chief executive officer with a US$1 billion cost-cutting program while it issued 2024 profit guidance shy of Wall Street estimates.

- Ford Motor Co. became the latest strike target for the United Auto Workers after members walked out of its largest plant, a highly profitable pickup factory in Kentucky.

- Target Corp. climbed following an upgrade to buy at Bank of America Corp., which sees an improved risk profile for the retailer based on recent pullback in the stock.

- Domino’s Pizza Inc. reported revenue for the third quarter that missed the average analyst estimate.

- Beyond Meat Inc. dropped after Mizuho Securities cut the recommendation to underperform, pointing to macroeconomic pressures for consumption and a “lack of disruptive innovation” in the area.

- Infosys Ltd. narrowed its sales forecast for the fiscal year, a sign that corporations are continuing to curtail spending on software and information technology projects.

Key events this week:

- China CPI, PPI, trade, Friday

- Eurozone industrial production, Friday

- U.S. University of Michigan consumer sentiment, Friday

- Citigroup, JPMorgan, Wells Fargo, BlackRock results as the quarterly earnings season kicks off, Friday

- G20 finance ministers and central bankers meet as part of IMF gathering, Friday

- ECB President Christine Lagarde, IMF Managing Director Kristalina Georgieva speak on IMF panel, Friday

- Fed’s Patrick Harker speaks, Friday

Some of the main moves in markets:

Stocks

- The S&P 500 fell 0.6 per cent as of 4 p.m. New York time

- The Nasdaq 100 fell 0.4 per cent

- The Dow Jones Industrial Average fell 0.5 per cent

- The MSCI World index fell 0.5 per cent

- Currencies

- The Bloomberg Dollar Spot Index rose 0.7 per cent

- The euro fell 0.8 per cent to US$1.0530

- The British pound fell 1.1 per cent to US$1.2175

- The Japanese yen fell 0.4 per cent to 149.81 per dollar

- Cryptocurrencies

- Bitcoin was little changed at US$26,702.63

- Ether fell 2.1 per cent to US$1,530.49

- Bonds

- The yield on 10-year Treasuries advanced 15 basis points to 4.71 per cent

- Germany’s 10-year yield advanced seven basis points to 2.79 per cent

- Britain’s 10-year yield advanced nine basis points to 4.42 per cent

Commodities

- West Texas Intermediate crude was little changed

- Gold futures fell 0.3 per cent to US$1,881.30 an ounce